Table of Contents

- the definitive guide to retirement income

- the definitive guide to retirement income: Key Strategies

- Understanding the Pillars of Retirement Income

- Social Security and Government Benefits

- Employer Pensions and Defined Benefit Plans

- Personal Savings, Investments, and Withdrawal Strategies

- Annuities as Income Guarantees

- Tax Considerations for Retirement Income

- Managing Risk in Retirement

- Market Volatility and Sequence of Returns Risk

- Inflation Protection

- Health Care and Long‑Term Care Costs

- Tools and Resources for Building Your Plan

- Actionable Checklist for Your Retirement Income Plan

Reaching retirement is a milestone that brings both relief and new challenges. After decades of work, the focus shifts from earning a paycheck to preserving and drawing down the wealth that has been accumulated. The transition is not simply about having money; it is about creating a reliable, predictable stream of income that can sustain a desired lifestyle for the rest of one’s life.

In this article we walk through the essential components of a retirement income plan, explain how each piece fits together, and offer practical steps anyone can follow. Whether you are approaching retirement, already retired, or helping a client navigate these waters, the content serves as a comprehensive reference. By the end, you will have a clear picture of how to construct a resilient income framework that balances growth, safety, and flexibility.

the definitive guide to retirement income

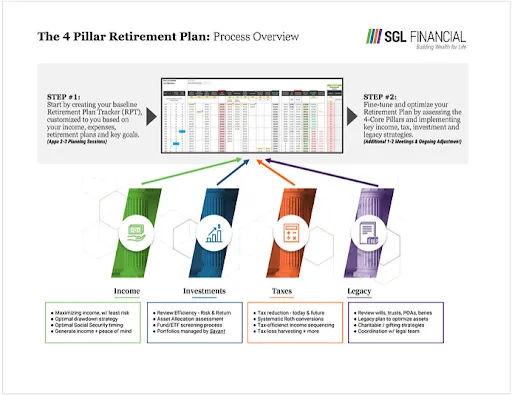

At its core, the definitive guide to retirement income emphasizes diversification. Just as investors diversify assets to reduce risk, retirees must diversify income sources to protect against market volatility, unexpected health expenses, and policy changes. A well‑balanced plan typically draws from four main pillars: government benefits, employer‑provided pensions, personal savings and investments, and annuity products. Each pillar has its own timing, tax treatment, and risk profile, and the optimal mix depends on individual goals, risk tolerance, and life expectancy.

the definitive guide to retirement income: Key Strategies

Below are the strategic considerations that shape a robust retirement income plan.

- Start Early and Review Often – The power of compound growth makes early savings essential, but regular reviews ensure the plan adapts to life changes.

- Match Income Timing to Expenses – Align cash flow with when you need money, using short‑term assets for near‑term costs and longer‑term investments for later years.

- Manage Tax Efficiency – Different income streams are taxed in distinct ways; planning can reduce the overall tax burden.

- Protect Against Longevity Risk – Ensure the plan can last longer than the average life expectancy.

Understanding the Pillars of Retirement Income

Each pillar contributes a unique function in the overall income architecture.

Social Security and Government Benefits

Social Security remains a cornerstone for many retirees, offering a base level of income that adjusts with inflation. Deciding when to claim—age 62, full retirement age, or delayed up to age 70—has a profound impact on monthly benefits. Delaying benefits increases the monthly amount by approximately 8% per year, which can be especially valuable for those with longer life expectancies.

Employer Pensions and Defined Benefit Plans

Although less common than in previous generations, defined benefit (DB) plans provide a guaranteed payout based on salary history and years of service. Understanding the payout formula, survivor benefits, and any cost‑of‑living adjustments is critical. In cases where the employer offers a cash‑balance or hybrid plan, the retirement income strategy may need to incorporate both defined benefit and defined contribution elements.

Personal Savings, Investments, and Withdrawal Strategies

Personal savings, typically held in 401(k), IRA, or Roth accounts, represent the most flexible pillar. The classic “4% rule”—withdrawing 4% of the portfolio’s initial value adjusted for inflation—offers a simple benchmark for sustainable withdrawals. However, modern research suggests a dynamic approach, adjusting withdrawals based on market performance and personal circumstances, can improve longevity outcomes.

Annuities as Income Guarantees

Annuities transform a lump‑sum investment into a stream of payments that can be lifetime or period‑certain. Fixed annuities provide predictable income, while variable and indexed annuities offer growth potential linked to market performance. When used judiciously, annuities can address longevity risk, but fees and surrender charges require careful scrutiny.

Tax Considerations for Retirement Income

Tax efficiency can make a significant difference in the net income available for living expenses. Below are common tax scenarios and strategies to manage them.

- Tax‑Deferred Accounts – Traditional 401(k) and IRA withdrawals are taxed as ordinary income. Planning the timing of withdrawals can keep you in a lower tax bracket.

- Tax‑Free Accounts – Roth accounts grow tax‑free, and qualified withdrawals are not taxed. Allocating a portion of income from Roth sources can provide flexibility in high‑tax years.

- Qualified Charitable Distributions (QCDs) – For retirees over 70½, directing up to $100,000 of IRA withdrawals to charity satisfies required minimum distributions (RMDs) without increasing taxable income.

- State Taxes – Some states tax retirement income differently. Relocating to a tax‑friendly jurisdiction can improve after‑tax cash flow.

Managing Risk in Retirement

Risk management is as important as income generation. The primary risks include market volatility, inflation, health expenses, and longevity.

Market Volatility and Sequence of Returns Risk

Early retirement years are especially vulnerable to “sequence of returns risk,” where poor market performance coincides with high withdrawal rates, depleting the portfolio faster. Strategies to mitigate this risk include maintaining a cash reserve for the first 5–7 years of retirement, using a bucket approach, or employing a “guardrails” method that adjusts equity exposure based on portfolio performance.

Inflation Protection

Inflation erodes purchasing power, making it essential to include assets that can outpace price increases. Treasury Inflation‑Protected Securities (TIPS), real estate, and equities historically provide inflation hedges. Some annuities also offer inflation riders for an additional cost.

Health Care and Long‑Term Care Costs

Health expenses often rise sharply in later years. Medicare covers many services but does not cover everything. A dedicated health savings account (HSA) or a supplemental insurance policy can help bridge gaps. Planning for long‑term care, either through insurance or a dedicated savings line, prevents unplanned asset depletion.

Tools and Resources for Building Your Plan

Technology has simplified retirement planning. Several software platforms enable advisors and individuals to model cash flow, tax implications, and longevity scenarios. For a deeper dive into such technology, see the article Retirement Income Planning Software for Advisors – A Complete Guide, which outlines key features and best practices.

Investment funds designed specifically for retirees also deserve attention. The Vanguard Target Retirement 2025 Fund Fact Sheet – In‑Depth Review provides a diversified, automatically rebalancing portfolio that becomes more conservative as the target date approaches.

Small business owners face unique challenges when structuring retirement income. The article Retirement Planning for Small Business Owners – A Complete Guide discusses options such as SEP‑IRAs, Solo 401(k)s, and cash‑balance pensions, highlighting how these vehicles fit into the broader income plan.

Actionable Checklist for Your Retirement Income Plan

Use the following step‑by‑step checklist to translate theory into practice.

- Assess Current Financial Situation – List all assets, liabilities, expected expenses, and existing income sources.

- Determine Desired Retirement Lifestyle – Estimate annual spending, accounting for travel, hobbies, and health care.

- Calculate Required Retirement Income – Subtract expected Social Security and pension benefits from total spending needs.

- Choose an Income Mix – Allocate percentages to each pillar (e.g., 30% Social Security, 20% pension, 30% withdrawals, 20% annuity).

- Implement Tax‑Efficient Withdrawal Strategies – Prioritize Roth withdrawals in high‑tax years, manage RMDs, consider QCDs.

- Establish an Emergency Cash Bucket – Keep 1–2 years of expenses in a liquid account to avoid forced sales.

- Monitor and Rebalance Annually – Adjust asset allocation, withdrawal rates, and annuity payouts based on performance and life changes.

- Review Estate and Legacy Plans – Ensure beneficiary designations, wills, and trusts align with income goals.

By systematically following this checklist, retirees can maintain confidence that their income streams are aligned with both short‑term cash needs and long‑term sustainability.

In summary, the definitive guide to retirement income underscores the importance of a diversified, tax‑aware, and risk‑managed approach. No single solution fits everyone; instead, a personalized blend of government benefits, employer pensions, personal investments, and annuity products creates a resilient financial foundation. Regular reviews, the use of modern planning tools, and an awareness of evolving tax and health landscapes ensure that retirees can enjoy their golden years without the constant worry of outliving their resources.