Table of Contents

- Retirement Planning for Small Business Owners: Key Considerations

- Understanding the Unique Challenges of Retirement Planning for Small Business Owners

- Choosing the Right Retirement Plan for Small Business Owners

- Funding Strategies and Contribution Limits

- Tax Advantages and Implications

- Integrating Retirement Planning with Business Succession

- Utilizing Professional Guidance and Tools

- Common Mistakes to Avoid in Retirement Planning for Small Business Owners

Running a small business often means juggling multiple responsibilities—cash flow, staffing, marketing, and long‑term growth. Amid these daily demands, thinking about retirement can feel like a distant concern. Yet, the earlier an entrepreneur starts to address retirement planning for small business owners, the more options become available and the less pressure there is to make rushed decisions later.

Unlike employees of large corporations, small business owners typically lack a built‑in retirement plan and must create one from scratch. This reality brings both challenges and opportunities. While the absence of an employer‑sponsored plan means there are no automatic payroll deductions, it also opens the door to flexible, tax‑advantaged solutions that can be tailored to the specific cash‑flow patterns of a growing business.

In this article we walk through the essential steps, common pitfalls, and practical tools that can help any entrepreneur craft a solid retirement strategy. Whether you are just starting out or approaching the exit phase, the guidance here is designed to fit the unique financial landscape of a small business.

Retirement Planning for Small Business Owners: Key Considerations

Understanding the Unique Challenges of Retirement Planning for Small Business Owners

Small business owners wear many hats, which often leads to inconsistent personal savings. Income can fluctuate seasonally, and profit is frequently reinvested back into the business. These dynamics make it harder to predict how much can be set aside each year for retirement. Additionally, many entrepreneurs blend personal and business finances, complicating the separation needed for clear retirement accounting.

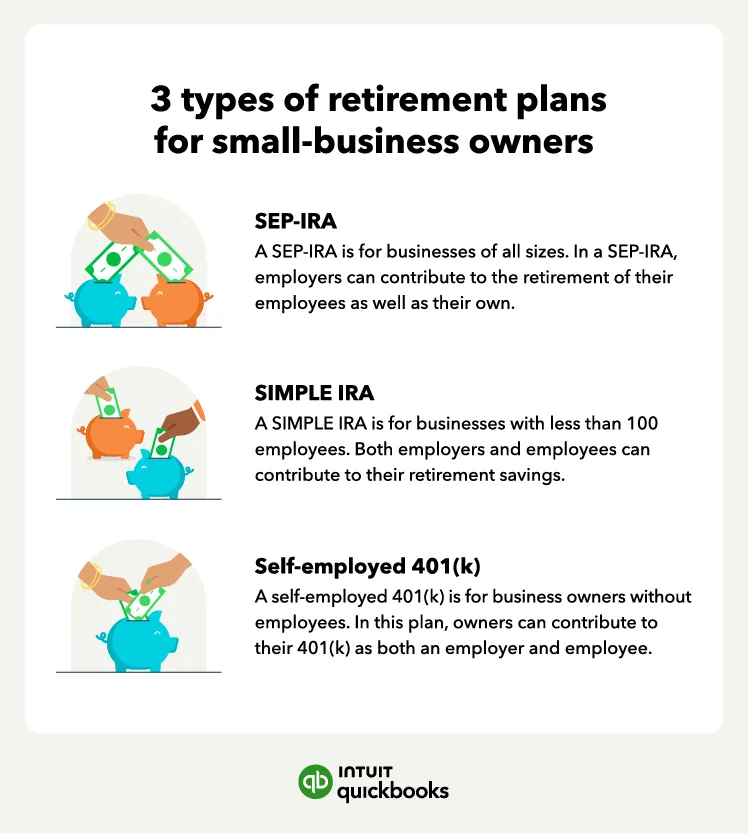

Another hurdle is the limited access to group retirement plans that large employers enjoy. Without a 401(k) match or a defined benefit plan, owners must rely on individual retirement accounts (IRAs) or small‑business‑specific plans such as a Solo 401(k), SEP‑IRA, or SIMPLE IRA. Each of these options carries distinct contribution limits, eligibility rules, and tax implications.

Choosing the Right Retirement Plan for Small Business Owners

When selecting a vehicle for retirement planning for small business owners, consider the following factors:

- Business size and structure: Sole proprietors, partnerships, and S‑corporations each have different options for contribution limits.

- Cash‑flow predictability: Plans that allow flexible contributions, such as a SEP‑IRA, work well for businesses with variable earnings.

- Future hiring plans: If you anticipate adding employees, a Solo 401(k) may be upgraded to a traditional 401(k) to include staff.

- Administrative simplicity: Some plans require annual filings (e.g., Form 5500 for a 401(k) with assets over $250,000), while others are largely paper‑free.

For a deeper dive into the specific options available, see the article Retirement Options for Small Business Owners – A Detailed Guide. It outlines the pros and cons of each plan type, helping you match a solution to your business’s financial rhythm.

Funding Strategies and Contribution Limits

One of the most powerful aspects of retirement planning for small business owners is the ability to contribute significantly more than an employee can through a traditional IRA. For example, a Solo 401(k) allows employee‑deferral contributions up to $22,500 (or $30,000 if age 50 or older) plus an employer contribution of up to 25% of compensation, with a combined limit of $66,000 for 2023.

SEP‑IRAs, on the other hand, let you contribute up to 25% of compensation, capping at $66,000 as well. The key is to calculate a sustainable contribution rate that does not jeopardize operational cash needs. Some owners adopt a “percentage of profit” rule—setting aside 10% of net profit each quarter—to maintain consistency.

Tax Advantages and Implications

Retirement planning for small business owners offers several tax benefits:

- Contributions reduce taxable income for the year they are made, lowering the current tax bill.

- Growth within the account is tax‑deferred (or tax‑free for Roth variants), compounding wealth faster.

- When structured correctly, contributions can be deducted as business expenses, improving the bottom line.

It’s also important to understand the impact of required minimum distributions (RMDs) after age 73. Planning ahead can mitigate the tax shock that RMDs sometimes cause, especially if the retirement account has grown substantially.

Integrating Retirement Planning with Business Succession

For many entrepreneurs, retirement and business succession go hand in hand. A well‑designed retirement plan can serve as a funding source for buying out a partner or selling the company. For instance, a cash‑value life insurance policy within a retirement plan can be leveraged to provide liquidity during a buy‑sell agreement.

Conversely, a clear succession plan can free up personal assets for retirement saving. When you know the exit strategy—whether through a sale, transfer to family, or employee ownership—you can better allocate retirement contributions without fearing that cash will be needed for an unexpected transition.

Utilizing Professional Guidance and Tools

Given the complexity of retirement planning for small business owners, many turn to financial advisors who specialize in small‑business retirement solutions. These professionals can run scenario analyses, compare plan costs, and ensure compliance with IRS regulations.

Technology also plays a role. Tools such as retirement income planning software help advisors and owners visualize future cash flows, tax impacts, and withdrawal strategies. Learn more about these platforms in Retirement Income Planning Software for Advisors – A Complete Guide.

Common Mistakes to Avoid in Retirement Planning for Small Business Owners

Even with the right plan in place, small business owners can stumble into costly errors:

- Procrastination: Delaying contributions reduces compounding power. Even modest early contributions can grow dramatically over time.

- Mixing personal and business expenses: Failing to separate these can trigger audit risks and muddle retirement account calculations.

- Ignoring contribution limits: Over‑contributing can result in penalties; under‑contributing may leave tax benefits on the table.

- Relying on a single retirement vehicle: Diversifying across a Solo 401(k) and a Roth IRA, for example, can provide flexibility in retirement withdrawals.

Some owners consider cashing out retirement savings to address immediate debt. While it may seem tempting, the long‑term cost—including taxes and lost growth—often outweighs short‑term relief. A balanced approach is discussed in Cashing Out Retirement to Pay Off Debt: A Comprehensive Guide.

Another strategic tip is to align retirement contributions with key business milestones. When the company hits a revenue target or after a successful product launch, allocate a percentage of the surplus to the retirement account. This method creates a habit of saving tied to business performance, reinforcing both financial health and personal security.

Finally, keep an eye on legislative changes. Tax laws affecting retirement contributions, deduction limits, and RMDs evolve periodically. Staying informed—or working with an advisor who monitors these shifts—ensures that your retirement planning for small business owners remains optimal.

In summary, retirement planning for small business owners is a multi‑faceted process that blends tax strategy, cash‑flow management, and long‑term vision. By selecting the appropriate retirement vehicle, contributing consistently, leveraging professional advice, and integrating the plan with broader business goals, entrepreneurs can build a robust financial safety net. The journey may require disciplined effort and occasional course corrections, but the payoff—a secure, dignified retirement while preserving the legacy of the business—makes the investment of time and resources worthwhile.