Table of Contents

- Understanding the Risks of cashing out retirement to pay off debt

- How cashing out retirement to pay off debt Impacts Your Future Savings

- Evaluating Alternatives Before Cashing Out Retirement to Pay Off Debt

- Tax Implications and Penalties of Early Withdrawal

- Strategies to Minimize Tax Burden When cashing out retirement to pay off debt

- Long‑Term Financial Planning After Cashing Out Retirement

- Key Steps to Rebuild Savings After cashing out retirement to pay off debt

- Psychological and Lifestyle Considerations

- Case Study: A Real‑World Illustration

- When Cashing Out Retirement to Pay Off Debt May Be Justifiable

Many individuals face the uncomfortable crossroads where mounting debt collides with the looming need to preserve retirement savings. The decision to tap into those hard‑earned funds can feel like an immediate solution, yet it often carries long‑term consequences that merit careful scrutiny. This article walks through the practical realities of cashing out retirement to pay off debt, highlighting the financial mechanics, tax implications, and alternative pathways that may offer a more balanced outcome.

Imagine a scenario: a homeowner in their early sixties confronts a sizable credit‑card balance while also approaching the age of retirement. The allure of a lump‑sum withdrawal from a 401(k) or an IRA appears as a quick fix, promising to eliminate monthly interest charges and restore a sense of control. However, this narrative is not unique, and understanding the broader context is essential before committing to such a move.

Through a factual, story‑like approach, we will explore the steps involved, the hidden costs, and the strategic considerations that can help you decide whether cashing out retirement to pay off debt is truly the most prudent choice.

Understanding the Risks of cashing out retirement to pay off debt

When you withdraw money from a qualified retirement account before reaching age 59½, the IRS typically imposes a 10% early‑withdrawal penalty in addition to ordinary income tax on the distribution. This double‑tax burden can quickly erode the net amount available to settle debts. For example, a $30,000 withdrawal could result in roughly $9,000 in combined taxes and penalties, leaving only $21,000 to address the liability.

Beyond immediate tax costs, cashing out retirement to pay off debt reduces the principal that would otherwise compound over decades. Even a modest annual return of 5% can generate significant growth over a 30‑year horizon. By diminishing that base, you sacrifice future purchasing power and may jeopardize the ability to maintain your desired lifestyle in retirement.

How cashing out retirement to pay off debt Impacts Your Future Savings

The concept of opportunity cost is central to this discussion. Every dollar removed from a retirement portfolio foregoes potential investment gains. If the debt you aim to eliminate carries an interest rate lower than the expected return on your retirement assets, the net financial effect could be negative. Conversely, high‑interest debts such as credit‑card balances (often exceeding 20% APR) may justify a short‑term sacrifice, but only after a thorough analysis of all variables.

Another factor to consider is the effect on required minimum distributions (RMDs) once you reach age 72. Smaller account balances lead to lower RMDs, which might seem beneficial, yet it also means you have less flexibility to manage taxable income in later years. The interplay between early withdrawals, tax brackets, and future RMDs creates a complex financial tapestry that deserves professional guidance.

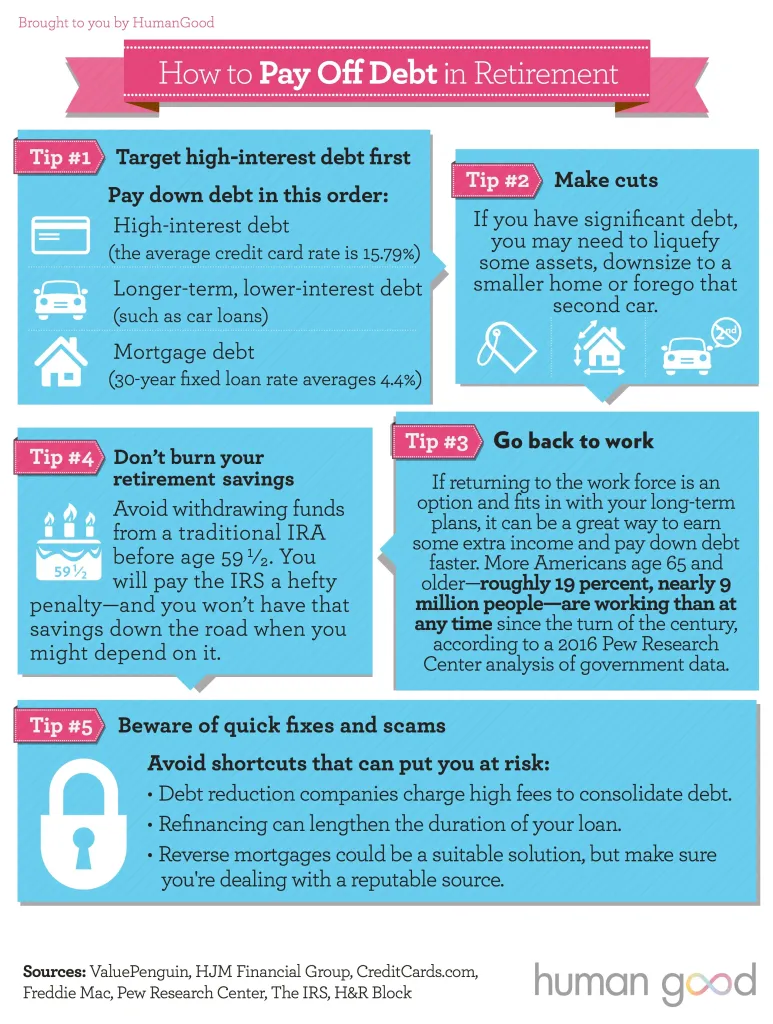

Evaluating Alternatives Before Cashing Out Retirement to Pay Off Debt

Before you decide to tap your retirement nest egg, explore the following alternatives that could provide relief without compromising long‑term security:

- Debt consolidation loans: Securing a lower‑interest personal loan to pay off higher‑rate credit‑card debt can reduce monthly payments while preserving retirement assets.

- Balance transfer credit cards: A 0% introductory APR period can give you a window to pay down principal without accruing additional interest.

- Home equity lines of credit (HELOC): If you own equity, borrowing against it may offer favorable rates, though it does place your home at risk if payments lapse.

- Budget restructuring: A disciplined cash‑flow analysis often reveals discretionary spending that can be redirected toward debt reduction.

- Seeking professional advice: Financial planners can model scenarios to compare the true cost of cashing out retirement versus other strategies.

For small business owners who also grapple with retirement planning, the article retirement options for small business owners – a detailed guide offers insight into how to balance business cash flow with personal financial obligations.

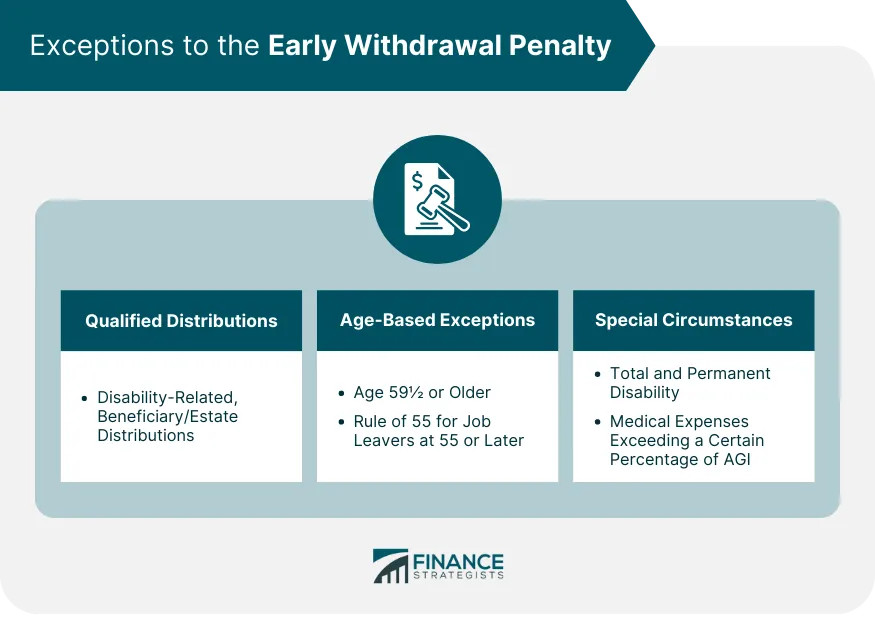

Tax Implications and Penalties of Early Withdrawal

The IRS treats most retirement account withdrawals as taxable income. When you execute a cashing out retirement to pay off debt transaction, the amount withdrawn is added to your ordinary income for the year, potentially pushing you into a higher tax bracket. Additionally, the 10% early‑withdrawal penalty applies unless you qualify for an exception, such as substantial medical expenses, a qualified domestic relations order, or certain qualified education costs.

State taxes may also apply, depending on where you reside. Some states conform to federal rules, while others have distinct tax treatments for retirement distributions. It is crucial to calculate both federal and state liabilities before proceeding.

Strategies to Minimize Tax Burden When cashing out retirement to pay off debt

If you determine that an early withdrawal is the most viable option, consider these tactics to mitigate tax impact:

- Spread withdrawals over multiple years: Taking smaller distributions can keep you within a lower tax bracket each year.

- Roth conversions: Converting a portion of a traditional IRA to a Roth IRA may allow you to pay taxes at the current rate and avoid future RMDs.

- Utilize deductions: Bunching charitable contributions or medical expenses into the year of withdrawal can offset increased taxable income.

- Coordinate with other income sources: Aligning withdrawals with years of lower earned income (e.g., after a career transition) can reduce overall tax liability.

Long‑Term Financial Planning After Cashing Out Retirement

Should you proceed with cashing out retirement to pay off debt, revisiting your retirement plan becomes essential. Rebuilding the withdrawn balance will likely require higher contribution rates, delayed retirement, or a shift to more aggressive investment allocations. Creating a realistic catch‑up strategy can help restore the trajectory toward your retirement goals.

Technology tools can simplify this process. For advisors and individuals alike, platforms such as retirement income planning software for advisors – a complete guide provide scenario analysis, projection modeling, and tax impact calculators to visualize the path forward.

Key Steps to Rebuild Savings After cashing out retirement to pay off debt

- Increase contribution percentages: Aim for at least 15% of gross income, adjusting upward as debt‑free status is achieved.

- Take advantage of catch‑up contributions: Individuals 50 or older can contribute an additional $7,500 (2024 limit) to 401(k)s and $1,000 to IRAs.

- Reassess asset allocation: A diversified portfolio aligned with risk tolerance can accelerate growth while managing volatility.

- Monitor progress regularly: Quarterly reviews help ensure that contributions, investment returns, and any lingering debt are on track.

Psychological and Lifestyle Considerations

Debt carries an emotional weight that can affect decision‑making. The relief of eliminating monthly payments may provide short‑term peace of mind, yet the knowledge of a reduced retirement cushion can generate anxiety later. Balancing immediate comfort with future security involves honest self‑assessment and, often, candid conversations with family members or financial counselors.

Moreover, lifestyle adjustments—such as downsizing a home, relocating to a lower‑cost area, or modifying discretionary spending—can free up cash to address debt without eroding retirement assets. These changes, while sometimes difficult, can preserve long‑term financial health.

Case Study: A Real‑World Illustration

John, a 58‑year‑old engineer, held $120,000 in a 401(k) and $35,000 in credit‑card debt at 20% APR. Facing a potential foreclosure due to missed mortgage payments, he contemplated cashing out retirement to pay off the credit‑card balances. After consulting a financial planner, John learned that a personal loan at 8% interest would cover his debt with a lower overall cost than the combined taxes and penalties of an early withdrawal.

John opted for the loan, used the funds to clear his credit‑card balances, and kept his retirement intact. He then increased his 401(k) contributions by 4% and set a target to rebuild the $30,000 he had earmarked for the loan repayment. Within three years, John not only eliminated the loan but also restored his retirement balance to its original level, all while preserving his credit score and avoiding unnecessary tax penalties.

When Cashing Out Retirement to Pay Off Debt May Be Justifiable

While the general guidance leans toward preserving retirement assets, certain circumstances may make early withdrawal the lesser of two evils:

- Medical emergencies: Unforeseen health expenses that exceed insurance coverage.

- Preventing foreclosure or repossession: When the loss of a primary residence would cause a more severe financial crisis.

- High‑interest, unsecured debt: Credit‑card balances exceeding 15% APR where other refinancing options are unavailable.

- Qualified disaster relief: Certain disaster‑related withdrawals may be penalty‑free.

Even in these scenarios, a thorough cost‑benefit analysis is indispensable. Engaging a certified financial planner or a chartered retirement planning counselor can ensure that you fully comprehend the trade‑offs.

In summary, the decision to cash out retirement to pay off debt is fraught with tax, opportunity, and emotional implications. By exploring alternatives, understanding tax consequences, and implementing disciplined post‑withdrawal strategies, you can safeguard both your present financial stability and future retirement aspirations.