Table of Contents

- Understanding errors and omissions insurance for real estate

- Key components of errors and omissions insurance for real estate

- Why errors and omissions insurance for real estate is essential for agents and brokers

- How to choose the right errors and omissions insurance for real estate

- Assess your risk profile

- Compare carriers and endorsements

- Review claims history

- Check for continuity provisions

- Seek professional advice

- Common claim scenarios and how errors and omissions insurance for real estate responds

- Misrepresentation of property condition

- Errors in contract drafting

- Failure to disclose zoning restrictions

- Cost considerations: premium factors for errors and omissions insurance for real estate

- Regulatory landscape and compliance

- Integrating errors and omissions insurance for real estate with broader risk management

- Steps to file a claim under errors and omissions insurance for real estate

- Future trends: how errors and omissions insurance for real estate is evolving

- Impact of digital transactions

- Rise of niche markets

- Data‑driven underwriting

In the fast‑moving world of property transactions, a single oversight can turn a profitable deal into a costly lawsuit. Real estate professionals—agents, brokers, and even developers—regularly navigate complex contracts, zoning regulations, and disclosure requirements. When a mistake occurs, the financial impact can be severe, threatening both personal assets and business continuity.

To protect against these risks, many in the industry turn to a specialized form of liability coverage known as errors and omissions insurance for real estate. This policy, often abbreviated as E&O, is designed to shield professionals from claims arising out of alleged negligence, errors, or incomplete work. Understanding how this coverage works, what it includes, and how to select the right policy is crucial for anyone who earns a living through property transactions.

The following guide breaks down the core concepts of errors and omissions insurance for real estate, outlines common scenarios that trigger claims, and offers practical steps to ensure adequate protection. Whether you are a solo agent, part of a large brokerage, or a real estate developer, the information presented here will help you make informed decisions about your professional liability strategy.

Understanding errors and omissions insurance for real estate

Errors and omissions insurance for real estate is a type of professional liability insurance that covers claims made by clients who allege that the insured failed to perform their professional duties adequately. Unlike general liability insurance, which addresses bodily injury and property damage, E&O focuses on financial losses that result from mistakes, misrepresentations, or failure to disclose material facts.

Typical situations that trigger coverage include:

- Incorrect advice about property values or market trends.

- Failure to disclose known defects or zoning restrictions.

- Errors in drafting or reviewing purchase agreements.

- Misrepresentation of a property’s condition or legal status.

When a client files a claim, the insurer typically covers legal defense costs, settlements, or judgments up to the policy limits, provided the claim falls within the scope of the policy. This financial safety net allows real estate professionals to focus on serving clients without the constant fear of crippling legal expenses.

Key components of errors and omissions insurance for real estate

Not all E&O policies are created equal. The following elements are essential to evaluate when comparing coverage options:

- Policy limits: The maximum amount the insurer will pay for a single claim and in aggregate over the policy period. Limits can range from $250,000 to several million dollars, depending on the size and risk profile of the business.

- Deductibles: The out‑of‑pocket amount the insured must pay before the insurer responds. Higher deductibles lower premiums but increase exposure.

- Territorial coverage: Some policies cover claims arising only within the United States, while others extend to international transactions.

- Claims-made versus occurrence: Most real estate E&O policies are claims‑made, meaning they cover claims reported during the policy period, regardless of when the error occurred. Continuity of coverage is critical when switching insurers.

- Exclusions: Common exclusions include fraudulent acts, intentional misconduct, and claims arising from services not listed in the policy.

Understanding these components helps agents align coverage with their specific risk exposure. For example, a broker who frequently handles high‑value commercial deals may need higher limits and broader territorial coverage than a residential agent focusing on single‑family homes.

Why errors and omissions insurance for real estate is essential for agents and brokers

Real estate transactions involve large sums of money, complex legal documents, and numerous parties. Even a minor oversight—such as a missed deadline or an inaccurate square‑footage statement—can lead to a lawsuit that threatens the professional’s reputation and financial stability. Errors and omissions insurance for real estate provides a safety net that:

- Protects personal assets from being seized to satisfy judgments.

- Covers the cost of hiring experienced legal counsel.

- Offers peace of mind, allowing agents to focus on client relationships rather than legal anxieties.

- Often fulfills licensing board or brokerage requirements, ensuring compliance with industry standards.

Many state real estate commissions mandate that agents maintain a minimum level of professional liability coverage. Even in states where it is not required, brokers frequently insist on it as part of their risk‑management policies. Without this protection, a single claim could jeopardize an entire career.

How to choose the right errors and omissions insurance for real estate

Selecting a policy involves more than just comparing price tags. Below are practical steps to help you find a plan that matches your needs:

Assess your risk profile

Start by evaluating the types of transactions you handle, the average deal size, and any specialty areas (e.g., luxury homes, commercial leases, or property development). Higher‑risk activities generally warrant higher policy limits and lower deductibles.

Compare carriers and endorsements

Not all insurers specialize in real estate. Look for carriers with a proven track record in underwriting professional liability for property professionals. Review policy endorsements that add coverage for specific services, such as property management or consulting.

Review claims history

Examine the insurer’s claims handling reputation. A policy that promises quick, transparent defense can be more valuable than one with lower premiums but a sluggish claims process.

Check for continuity provisions

Because most policies are claims‑made, it’s essential to secure a “tail” endorsement if you plan to retire or switch carriers. This endorsement extends coverage for claims reported after the policy ends, covering errors that occurred while the policy was active.

Seek professional advice

Consulting with a broker who understands real estate risks can streamline the selection process. They can tailor coverage, negotiate limits, and ensure that all relevant endorsements are included.

For a deeper dive into policy specifics, see our comprehensive guide to errors and omissions insurance for real estate. The article outlines common pitfalls and provides a checklist for evaluating quotes.

Common claim scenarios and how errors and omissions insurance for real estate responds

Real‑world claims illustrate why coverage matters. Below are three typical examples and the role of E&O insurance in each case.

Misrepresentation of property condition

An agent fails to disclose a known water intrusion issue. The buyer later discovers extensive damage and sues for repair costs. Errors and omissions insurance for real estate covers the legal defense, and, if the claim is settled, the policy pays the settlement up to the policy limit.

Errors in contract drafting

A broker drafts a purchase agreement with a typo that changes the closing date, causing the buyer to lose a financing deadline. The buyer files a claim for consequential losses. The E&O policy steps in to cover attorney fees and any awarded damages, protecting the broker’s personal assets.

Failure to disclose zoning restrictions

A developer sells land without informing the purchaser of a pending zoning change that limits future construction. The buyer sues for loss of anticipated development value. Errors and omissions insurance for real estate provides defense costs and, if the claim succeeds, covers the settlement amount.

These scenarios highlight the breadth of protection offered by errors and omissions insurance for real estate. While no policy can prevent every lawsuit, having the right coverage dramatically reduces financial exposure.

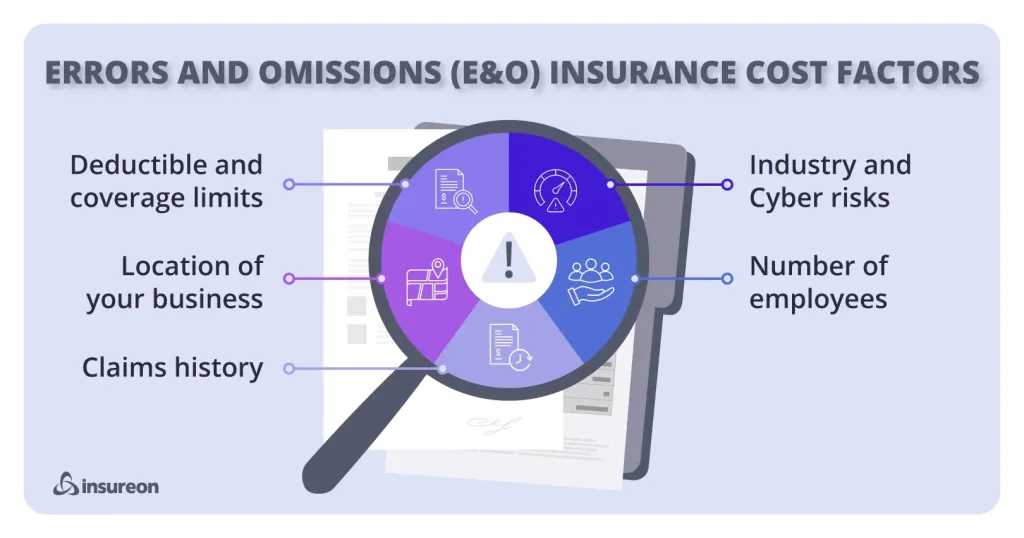

Cost considerations: premium factors for errors and omissions insurance for real estate

Premiums are influenced by several variables. Understanding these can help you budget effectively.

- Experience level: New agents often face higher rates because they lack a claims history.

- Revenue and transaction volume: Higher sales volumes increase exposure, leading to higher premiums.

- Claims history: A clean record can result in discounts, while past claims raise rates.

- Geographic location: Regions with higher litigation rates or property values may see increased costs.

- Policy structure: Choosing a higher deductible or lower limit can lower the premium, but it also adjusts the risk you retain.

On average, residential agents might pay between $500 and $1,500 annually for a basic $1 million limit, while commercial brokers often see premiums ranging from $2,000 to $5,000 or more. It’s essential to balance affordability with adequate protection.

Regulatory landscape and compliance

State real estate commissions regulate licensing and may require agents to maintain a minimum level of professional liability coverage. For instance, California mandates a $100,000 per claim limit for agents, while Texas requires at least $250,000 per claim. Failure to meet these requirements can result in fines, license suspension, or denial of brokerage affiliation.

Beyond state mandates, many brokerage firms impose stricter internal standards. Some require agents to carry higher limits or specific endorsements, such as cyber liability coverage for electronic data breaches. Staying informed about both statutory and brokerage requirements is a key part of risk management.

If you manage a team of agents, consider reviewing the real estate broker E&O insurance comprehensive guide to understand how broker‑level policies differ from individual coverage and how to structure a program that protects the entire firm.

Integrating errors and omissions insurance for real estate with broader risk management

While E&O insurance is a cornerstone of professional protection, it works best as part of a holistic risk‑management strategy. Additional layers may include:

- General liability insurance: Covers bodily injury and property damage occurring on the premises.

- Cyber liability insurance: Addresses data breaches, client privacy violations, and online fraud.

- Workers’ compensation: Required if you have employees, covering on‑the‑job injuries.

- Professional training and compliance programs: Ongoing education reduces the likelihood of errors that could trigger claims.

By combining these elements, you create a robust defense against both predictable and unforeseen liabilities.

Steps to file a claim under errors and omissions insurance for real estate

When a claim arises, following a structured process can streamline resolution:

- Notify the insurer promptly: Most policies require immediate notice of a potential claim.

- Gather documentation: Collect all relevant contracts, emails, disclosures, and notes.

- Cooperate with the adjuster: Provide requested information and avoid direct communication with the claimant without legal counsel.

- Engage legal counsel: Many insurers have a panel of attorneys experienced in real estate defense.

- Track expenses: Keep records of all defense costs, as they may affect the deductible or policy limits.

Timely and organized claim handling not only protects your coverage but also demonstrates professionalism to clients and regulators.

Future trends: how errors and omissions insurance for real estate is evolving

The real estate industry is undergoing rapid transformation due to technology, data analytics, and changing consumer expectations. These shifts influence the nature of professional liability and the design of insurance products.

Impact of digital transactions

Electronic signatures, virtual tours, and AI‑driven valuation tools reduce paperwork but introduce new risks, such as cyber‑theft and algorithmic errors. Insurers are responding by offering hybrid policies that bundle E&O with cyber liability, ensuring coverage for both traditional mistakes and tech‑related incidents.

Rise of niche markets

Specialized sectors—like short‑term rentals, co‑living spaces, and sustainable “green” developments—present unique contractual complexities. Tailored endorsements are emerging to address the specific liabilities of these niches.

Data‑driven underwriting

Insurers are leveraging big data to assess risk more accurately, offering dynamic pricing based on an agent’s transaction history, client reviews, and compliance records. This approach promises more equitable premiums but also requires professionals to maintain detailed performance metrics.

Staying abreast of these trends ensures that your errors and omissions insurance for real estate remains relevant and effective in a changing landscape.

In summary, errors and omissions insurance for real estate is a vital safeguard that protects professionals from the financial fallout of mistakes, omissions, or misrepresentations. By understanding coverage components, evaluating risk, and integrating insurance with broader risk‑management practices, agents and brokers can maintain confidence in their daily operations. Regularly reviewing policy terms, staying compliant with state regulations, and anticipating industry trends will keep your protection robust for years to come.