Table of Contents

- e&o Insurance for Real Estate Brokers: Core Coverage Explained

- Why e&o Insurance for Real Estate Brokers Is a Non‑Negotiable Necessity

- Key Factors That Influence Premiums for e&o Insurance for Real Estate Brokers

- How to Choose the Right e&o Insurance for Real Estate Brokers

- Common Claims Faced by Real Estate Brokers and How e&o Insurance Helps

- Real‑World Example: A Litigation Scenario Resolved by e&o Coverage

- Integrating e&o Insurance into a Comprehensive Risk Management Strategy

- Further Reading: A Comprehensive Guide Tailored for Brokers

In the fast‑moving world of property transactions, a real‑estate broker’s day is filled with negotiations, paperwork, and client interactions. While the excitement of closing deals can be rewarding, the profession also carries a unique set of liabilities. A single error, missed disclosure, or misunderstood contract term can expose a broker to costly lawsuits. This is where errors and omissions insurance—commonly known as e&o insurance—steps in to protect the broker’s livelihood.

Understanding e&o insurance for real estate brokers is not merely about complying with state regulations; it is about safeguarding the reputation and financial stability of a business that thrives on trust. The right coverage can mean the difference between weathering a claim and facing a financial crisis. Below, we explore the core components of e&o insurance, the factors that influence premiums, and practical steps brokers can take to secure optimal protection.

e&o Insurance for Real Estate Brokers: Core Coverage Explained

At its essence, e&o insurance for real estate brokers provides protection against claims of professional negligence, mistakes, or failure to perform professional duties. The policy typically covers legal defense costs, settlements, and judgments, up to the policy limit. Below are the primary coverages you can expect:

- Professional Liability: Protects against claims arising from inaccurate advice, misrepresentation of property facts, or failure to disclose material information.

- Legal Defense Fees: Covers the cost of hiring attorneys, expert witnesses, and court expenses, even if the claim is unfounded.

- Personal Injury: Extends coverage to claims of defamation, libel, or slander that occur in the course of business.

- Regulatory Defense: Some policies include protection when a broker is investigated by real‑estate licensing boards or other regulatory agencies.

It is essential to read the policy wording carefully. Not every e&o policy is identical; some may exclude certain types of transactions, such as commercial leasing, or limit coverage for claims related to property management services.

Why e&o Insurance for Real Estate Brokers Is a Non‑Negotiable Necessity

Real‑estate brokers operate in an environment where the stakes are high and the margin for error is thin. A single misstep—like overlooking a zoning restriction or providing inaccurate square‑footage data—can trigger a lawsuit that quickly escalates beyond the broker’s personal assets. Moreover, many states require brokers to maintain a minimum level of e&o coverage as a condition of licensure. Even in jurisdictions where it is not mandatory, clients increasingly expect brokers to demonstrate that they carry professional liability protection.

Consider the case of a broker who failed to disclose a pending lien on a property. The buyer later discovered the lien during closing, resulting in a $150,000 loss. The buyer sued the broker for negligence. Without e&o insurance for real estate brokers, the broker would have had to cover legal fees and any settlement out of pocket, potentially jeopardizing the entire business. With a solid policy in place, the insurer handled the defense and paid the settlement, allowing the broker to continue operating.

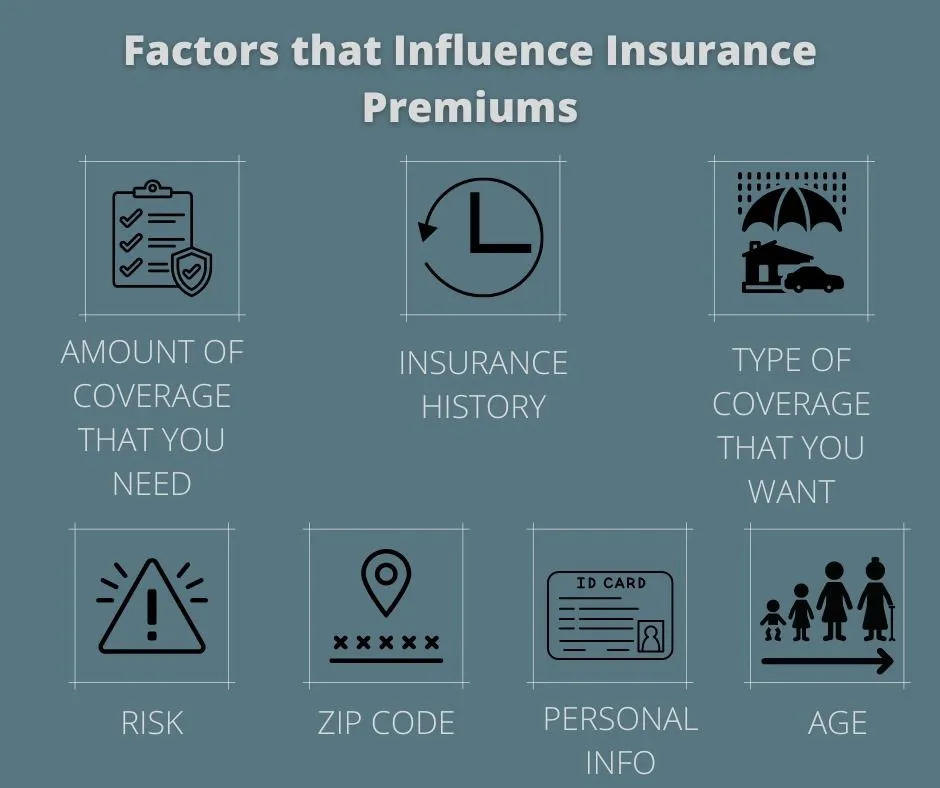

Key Factors That Influence Premiums for e&o Insurance for Real Estate Brokers

Insurance carriers assess risk using a variety of criteria. Understanding these factors helps brokers make informed decisions and potentially lower their premiums:

- Experience Level: Brokers with a longer track record and fewer past claims typically enjoy lower rates.

- Transaction Volume: Higher annual sales volume can increase exposure, leading to higher premiums.

- Geographic Location: Markets with higher litigation rates or more complex property laws may attract higher costs.

- Type of Services Offered: Adding services such as property management or commercial brokerage can broaden coverage needs and affect pricing.

- Claims History: A clean claims record signals lower risk, while recent or multiple claims can raise rates.

- Policy Limits and Deductibles: Choosing higher limits and lower deductibles provides stronger protection but raises the premium.

Brokerages often benefit from grouping policies under a single umbrella, especially when multiple agents share the same office. This can result in economies of scale and a more streamlined claims process.

How to Choose the Right e&o Insurance for Real Estate Brokers

Selecting the appropriate policy involves more than just comparing price tags. Follow these steps to ensure comprehensive protection:

- Assess Your Exposure: Calculate the maximum potential loss from a single claim, considering both legal costs and possible settlements.

- Review Policy Exclusions: Verify that the policy does not exclude the types of transactions you regularly handle.

- Compare Multiple Quotes: Engage with several carriers to understand differences in coverage, limits, and service quality.

- Check Financial Strength: Choose insurers with strong ratings from agencies like A.M. Best or Standard & Poor’s.

- Seek Professional Advice: Consulting an insurance broker who specializes in real‑estate coverage can uncover hidden risks and tailor the policy to your needs.

For a deeper dive into the nuances of professional liability, the article Errors and Omissions Insurance for Real Estate – What Every Professional Should Know provides a thorough overview of claim scenarios and policy options.

Common Claims Faced by Real Estate Brokers and How e&o Insurance Helps

While each brokerage is unique, certain claim types recur across the industry. Understanding these scenarios illustrates why e&o insurance for real estate brokers is indispensable.

- Failure to Disclose: Omitting material facts about a property’s condition, legal encumbrances, or neighborhood zoning can lead to buyer lawsuits.

- Misrepresentation of Property Value: Overstating market value or square footage may result in claims of negligent advice.

- Breach of Fiduciary Duty: Allegations that a broker prioritized personal gain over the client’s best interest.

- Contract Errors: Mistakes in drafting or interpreting purchase agreements can trigger disputes.

- Advertising Violations: Using inaccurate or misleading marketing materials may expose brokers to regulatory penalties and civil claims.

When any of these events occur, the e&o insurance for real estate brokers steps in to fund the defense, negotiate settlements, and, if necessary, cover court‑ordered judgments. The coverage often operates on a “claims‑made” basis, meaning the policy must be active both when the alleged error occurs and when the claim is filed.

Real‑World Example: A Litigation Scenario Resolved by e&o Coverage

Imagine a broker who represented a seller in a residential transaction. The broker inadvertently omitted a known foundation issue from the disclosure packet. After closing, the buyer discovered the defect, resulting in $80,000 in repair costs. The buyer sued for negligence. Because the broker had e&o insurance for real estate brokers, the insurer covered the $15,000 legal defense, negotiated a $70,000 settlement, and the broker incurred only a modest deductible. Without the policy, the broker would have faced a potentially devastating financial blow.

Integrating e&o Insurance into a Comprehensive Risk Management Strategy

Insurance alone does not eliminate risk; it mitigates financial impact. Effective risk management combines insurance with proactive measures:

- Standardized Documentation: Use checklists and standardized forms to ensure all required disclosures are captured.

- Continuing Education: Stay current on local regulations, market trends, and best practices through regular training.

- Client Communication Protocols: Document all client interactions, especially advice related to property condition or market value.

- Technology Tools: Leverage transaction management software to reduce human error and maintain audit trails.

- Quality Assurance Reviews: Implement peer reviews of contracts and disclosures before submission.

When these controls are in place, the likelihood of a claim diminishes, which can positively influence future premium calculations. The synergy between sound business practices and e&o insurance for real estate brokers creates a resilient operation capable of handling unforeseen challenges.

Further Reading: A Comprehensive Guide Tailored for Brokers

For those seeking an all‑inclusive resource, the guide Real Estate Broker E&O Insurance: A Comprehensive Guide outlines policy structures, case studies, and step‑by‑step instructions for filing a claim.

In addition, the article e&o Insurance for Real Estate Agents – Essential Coverage Explained breaks down coverage limits and deductible choices in plain language, helping agents make informed decisions without legal jargon.

Ultimately, e&o insurance for real estate brokers is more than a regulatory checkbox; it is a strategic investment in the long‑term health of a brokerage. By understanding the scope of coverage, evaluating risk factors, and integrating preventive practices, brokers can protect both their clients and their own professional futures.

As the real‑estate landscape evolves with new technologies, tighter regulations, and shifting market dynamics, the importance of robust professional liability protection only grows. Brokers who proactively secure comprehensive e&o coverage position themselves to navigate complexities with confidence, ensuring that a single mistake does not jeopardize years of hard‑earned success.