Table of Contents

- Health Insurance for Retired Postal Employees: Core Programs and Options

- How Health Insurance for Retired Postal Employees Interacts with Medicare

- Federal Employees Health Benefits (FEHB) and Its Role for Retirees

- Postal Service Retiree Health Benefits (RHB) Explained

- Eligibility Criteria and Enrollment Timelines

- Cost Considerations and Financial Planning

- Practical Tips for Maximizing Benefits

- Common Challenges and How to Overcome Them

- Future Outlook: Policy Changes and Their Potential Impact

- Steps to Enroll and Maintain Coverage

When a postal worker hangs up the uniform after decades of service, the transition to retirement brings a mix of relief and new responsibilities. One of the most pressing concerns is securing reliable health coverage that respects years of dedication while fitting a fixed income. The journey through health insurance for retired postal employees is shaped by federal programs, union agreements, and personal choices that together form a safety net for the later years.

Understanding the landscape starts with recognizing that former postal workers are not treated the same as typical private‑sector retirees. Their benefits are woven into the fabric of the United States Postal Service (USPS) and the Federal Employees Health Benefits (FEHB) program. This unique arrangement offers options that can be both generous and complex. By walking through the key components—eligibility, plan types, enrollment timelines, and cost‑management strategies—retirees can make informed decisions that protect their health and financial well‑being.

In the following sections, we will unpack each element of health insurance for retired postal employees, provide actionable tips, and point you toward resources that simplify the process. Whether you are approaching retirement or already enjoying your first years of leisure, the information here is designed to guide you step by step.

Health Insurance for Retired Postal Employees: Core Programs and Options

The foundation of health insurance for retired postal employees rests on three pillars: Medicare, the Federal Employees Health Benefits (FEHB) program, and the Postal Service’s retiree health plan (often referred to as the Retiree Health Benefit (RHB) or the Postal Service Retiree Health Plan). Each program serves a distinct purpose and together they create a layered approach to coverage.

How Health Insurance for Retired Postal Employees Interacts with Medicare

Medicare automatically becomes available to most retirees at age 65. Enrollment is optional, but delaying can result in penalties. For former postal workers, Medicare Part A (hospital insurance) is usually premium‑free because they have paid Medicare taxes throughout their careers. Part B (medical insurance) carries a monthly premium that is based on income, and it is essential for covering services not included in Part A.

When a retiree also participates in the FEHB program, the two plans work side by side. FEHB often serves as a supplemental plan, covering copayments, deductibles, and services that Medicare does not. Understanding this coordination is crucial because it determines out‑of‑pocket costs and influences the choice of an FEHB plan that best matches the retiree’s health needs.

Federal Employees Health Benefits (FEHB) and Its Role for Retirees

FEHB is a voluntary, employer‑sponsored health insurance program that offers more than 30 plan options ranging from fee‑for‑service to health maintenance organizations (HMOs). Retired postal employees who were enrolled in FEHB at the time of retirement can continue their coverage without interruption, provided they meet certain criteria such as maintaining continuous enrollment for a minimum number of years.

Because FEHB plans differ in premium structure, provider networks, and prescription drug coverage, retirees should review each option carefully. Some plans have higher premiums but lower out‑of‑pocket expenses, which can be advantageous for individuals with chronic conditions. Others may offer broader national networks, suitable for retirees who travel frequently.

Postal Service Retiree Health Benefits (RHB) Explained

The Postal Service provides a retiree health benefit that functions as a supplemental insurance layer. It is typically offered to employees who retire after at least 20 years of service and have met the eligibility requirements for the USPS Retiree Health Plan. This benefit helps cover costs that neither Medicare nor FEHB fully address, such as certain specialist visits, vision, and dental services.

Eligibility for the RHB is not automatic; retirees must apply during the designated enrollment window and may be required to contribute a monthly premium based on their chosen level of coverage. The premium rates are generally lower than comparable private plans because of the collective bargaining power of the postal union.

Eligibility Criteria and Enrollment Timelines

Meeting the eligibility requirements for each program is the first step toward securing health insurance for retired postal employees. Below is a concise overview of the key thresholds:

- Medicare: Age 65 or younger with certain disabilities; automatic enrollment for most retirees at 65.

- FEHB Continuation: Must have been continuously enrolled for at least 5 years, or at least 2 years if the retiree is a former member of the Federal Employees’ Group Life Insurance (FEGLI) program.

- RHB: Minimum 20 years of service with the USPS and enrollment during the open season, typically occurring a few months before the retirement date.

Missing an enrollment window can lead to a lapse in coverage or the need to wait for the next open season, which could result in higher premiums. Therefore, retirees should mark their calendars and keep documentation of service years, current FEHB status, and any existing health plans.

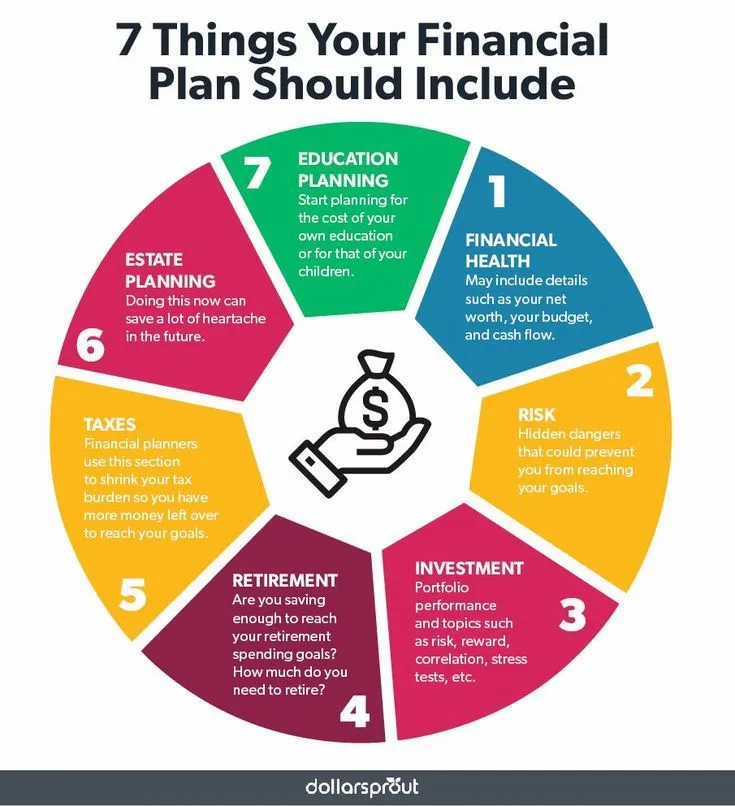

Cost Considerations and Financial Planning

Budgeting for health insurance is a critical component of retirement planning. The combined costs of Medicare premiums, FEHB contributions, and any RHB premiums can vary widely based on the chosen plans and the retiree’s income level.

For example, a retiree who selects a high‑deductible FEHB plan might pay a lower monthly premium but could face larger out‑of‑pocket expenses when seeking care. Conversely, a low‑deductible plan with higher premiums could provide more predictable costs throughout the year. Adding the RHB premium—often a modest amount relative to private insurance—can further reduce overall expenses by covering services not otherwise included.

Many retirees find it helpful to use a retirement budgeting worksheet or consult a financial advisor. Tools such as the Definitive Guide to Retirement Income can help project future healthcare costs and align them with other income sources like Social Security or a 401(k).

Practical Tips for Maximizing Benefits

To make the most of health insurance for retired postal employees, consider the following actionable steps:

- Review Plan Summaries Annually: Insurance plans can change their networks, copay structures, and covered services each year. Stay informed to avoid unexpected bills.

- Leverage Preventive Services: Medicare and most FEHB plans cover annual physicals, vaccinations, and screenings at no cost. Using these services can catch health issues early and reduce long‑term expenses.

- Combine Coverage Wisely: Evaluate how Medicare, FEHB, and RHB work together. For instance, a Medicare Advantage plan might replace Part B and provide additional benefits, but it may not be compatible with certain FEHB options.

- Use Prescription Drug Plans (PDPs): If your FEHB plan does not include drug coverage, consider a separate Medicare Part D plan. Compare formulary lists to ensure your medications are covered.

- Stay Within Network Boundaries: Out‑of‑network visits often result in higher cost‑sharing. Confirm that your preferred doctors and hospitals are part of the plan’s network before scheduling appointments.

Common Challenges and How to Overcome Them

Even with robust options, retirees may encounter obstacles such as coordination of benefits, claim denials, or changes in plan eligibility due to shifts in employment status of a spouse. Here are strategies to address these issues:

- Coordinate Benefits Early: Submit all necessary documentation to Medicare, FEHB, and the RHB simultaneously. This reduces processing delays.

- Maintain Accurate Records: Keep copies of enrollment forms, premium receipts, and Explanation of Benefits (EOB) statements. They are essential for resolving disputes.

- Seek Assistance from the Union: The American Postal Workers Union (APWU) offers member services that can help navigate enrollment, answer coverage questions, and advocate on your behalf.

- Utilize Online Portals: Most programs provide web portals where you can track claims, update personal information, and view plan changes in real time.

Future Outlook: Policy Changes and Their Potential Impact

The landscape of health insurance for retired postal employees is not static. Legislative proposals that affect Medicare reimbursement rates, FEHB premium caps, or the continuation of the RHB could alter the benefits retirees currently enjoy. Staying engaged with policy updates—through newsletters from the USPS, the APWU, or government health agencies—helps retirees anticipate changes and adjust their coverage accordingly.

For example, a proposed amendment to expand Medicare Part B coverage for telehealth services could reduce the need for supplemental FEHB coverage for virtual visits. Conversely, any reduction in federal funding for the FEHB program might result in higher premiums, prompting retirees to reassess their plan choices.

Steps to Enroll and Maintain Coverage

Below is a concise checklist that outlines the enrollment process for health insurance for retired postal employees:

- Confirm eligibility for Medicare, FEHB continuation, and the Postal Service Retiree Health Plan.

- Gather required documentation: service records, current health plan statements, and Social Security number.

- Enroll in Medicare during the Initial Enrollment Period (three months before turning 65, the month of, and three months after).

- Select an FEHB plan that aligns with your health needs and budget. Use the FEHB plan comparison tool available on the Office of Personnel Management (OPM) website.

- Apply for the RHB during the designated open enrollment window. Pay the applicable premium to activate coverage.

- Set up automatic premium payments to avoid lapses in coverage.

- Periodically review your coverage during the annual open enrollment season to ensure it still meets your needs.

Following these steps reduces the risk of coverage gaps and ensures that retirees can focus on their health rather than administrative hurdles.

For those who manage small business investments or have additional retirement accounts, integrating health insurance decisions with overall financial strategy can enhance stability. The Retirement Planning for Small Business Owners – A Complete Guide offers insights on aligning health benefits with broader retirement assets.

In conclusion, health insurance for retired postal employees is a multifaceted system that combines federal programs, union-negotiated benefits, and individual choices. By understanding eligibility, evaluating plan options, and staying proactive with enrollment and cost management, retirees can secure comprehensive coverage that honors their years of service while supporting a healthy, financially secure retirement.