Table of Contents

- what is a chartered retirement planning counselor: Definition and Core Purpose

- what is a chartered retirement planning counselor: Required Education and Certification

- Key Services Delivered by a Chartered Retirement Planning Counselor

- what is a chartered retirement planning counselor: The Role in Risk Management

- How a Chartered Retirement Planning Counselor Differs from Other Advisors

- what is a chartered retirement planning counselor: Choosing the Right Professional

- Integrating a Chartered Retirement Planning Counselor into Your Financial Team

- what is a chartered retirement planning counselor: Real‑World Example

- Future Trends Shaping the Role of Chartered Retirement Planning Counselors

Planning for retirement can feel like navigating a maze without a map. Many individuals turn to professionals who claim expertise, but not all titles carry the same weight. Among the most respected designations is the chartered retirement planning counselor, a credential that signals rigorous training, ethical standards, and a deep focus on the unique challenges retirees face.

Understanding what is a chartered retirement planning counselor requires looking beyond a simple label. It involves examining the educational pathway, the regulatory framework, and the practical services delivered to clients. This article walks you through those elements, illustrating how a chartered retirement planning counselor differs from other financial advisors and why their specialized knowledge can be a pivotal asset in your retirement strategy.

what is a chartered retirement planning counselor: Definition and Core Purpose

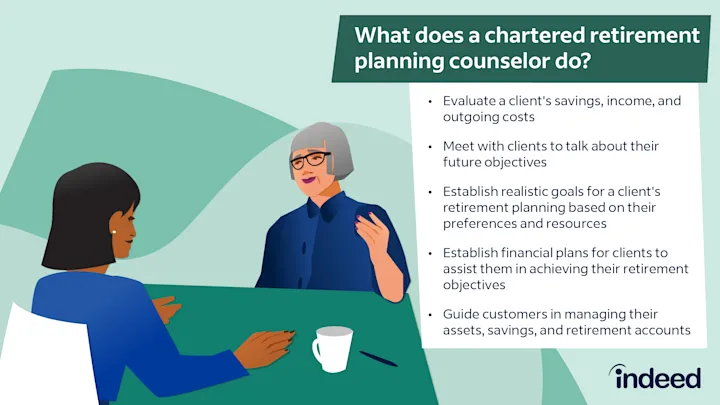

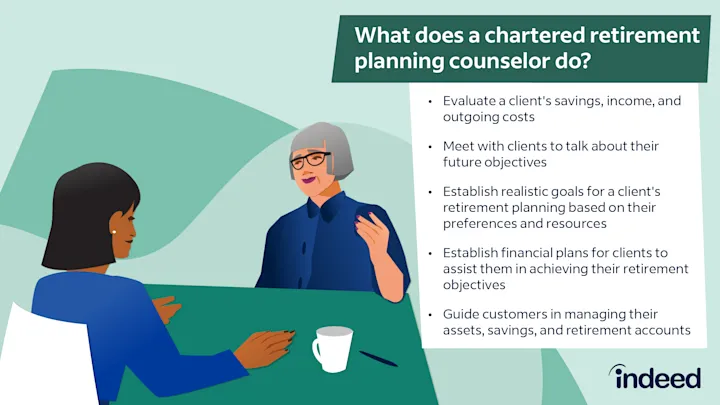

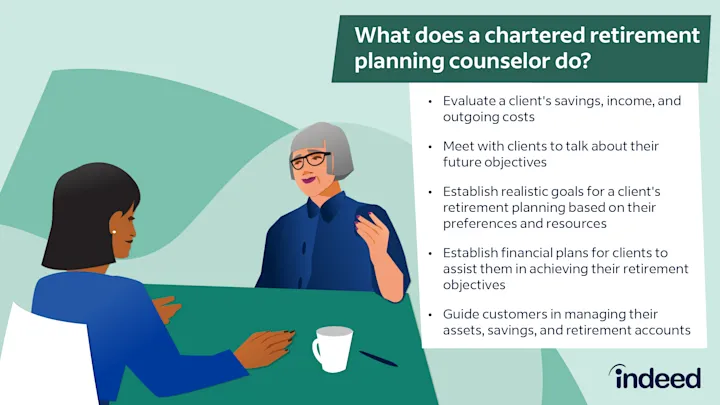

A chartered retirement planning counselor (CRPC) is a professional who has earned a chartered designation specifically oriented toward retirement planning. The title is typically granted by a recognized professional body—such as the Chartered Institute of Retirement Planning (CIRP) or a similar national authority—that sets strict educational, examination, and ethical requirements. The core purpose of a CRPC is to help individuals and families develop, implement, and monitor retirement plans that align with long‑term financial goals, risk tolerance, and lifestyle aspirations.

Unlike generic financial planners, a chartered retirement planning counselor focuses exclusively on the retirement phase of the financial life cycle. This specialization means they are well‑versed in topics such as pension scheme design, annuity selection, tax‑efficient withdrawal strategies, healthcare cost projections, and legacy planning. Their advice is grounded in both fiduciary responsibility and a chartered code of conduct that emphasizes client‑first decision making.

what is a chartered retirement planning counselor: Required Education and Certification

- Academic Foundations – Candidates usually hold a bachelor’s degree in finance, economics, accounting, or a related field. Some programs may also accept degrees in business administration or law, provided the applicant completes prerequisite courses in retirement economics.

- Professional Coursework – A series of chartered modules covers topics such as actuarial mathematics, retirement income modeling, regulatory compliance (including IRS rules), and ethical considerations. The curriculum often mirrors the depth found in actuarial exams.

- Examination Process – To earn the chartered status, candidates must pass a comprehensive exam that tests both theoretical knowledge and practical application. The exam may include case studies that simulate real‑world retirement planning scenarios.

- Continuing Professional Development (CPD) – After certification, a CRPC must complete a set number of CPD hours each year. This ensures they stay current with evolving tax laws, product innovations, and demographic trends that affect retirees.

Key Services Delivered by a Chartered Retirement Planning Counselor

The services offered by a chartered retirement planning counselor are designed to address the full spectrum of retirement needs. Below are the most common areas of focus:

- Retirement Goal Setting – Establishing realistic retirement income targets based on desired lifestyle, anticipated longevity, and inflation expectations.

- Pension and Social Security Optimization – Analyzing employer-sponsored pension plans, government benefits, and the timing of Social Security claims to maximize lifetime benefits.

- Investment Allocation – Crafting asset‑allocation strategies that balance growth potential with risk reduction, often incorporating target‑date funds such as the State Street Target Retirement 2030 Fund – In‑Depth Overview as a convenient option for diversified exposure.

- Tax‑Efficient Withdrawal Strategies – Planning the sequence of withdrawals from taxable, tax‑deferred, and tax‑free accounts to minimize tax liabilities, a concern highlighted in articles like Can the IRS Take Your Retirement Money? A Detailed Look.

- Healthcare and Long‑Term Care Planning – Estimating future medical expenses and recommending insurance products that protect against catastrophic costs.

- Estate and Legacy Planning – Coordinating wills, trusts, and beneficiary designations to ensure assets are transferred according to the client’s wishes while reducing estate taxes.

what is a chartered retirement planning counselor: The Role in Risk Management

One of the most critical functions of a chartered retirement planning counselor is to assess and mitigate financial risks that could derail a retirement plan. These risks include market volatility, longevity risk (outliving savings), inflation, and unexpected health expenses. By employing actuarial models and scenario analysis, the counselor can propose solutions such as guaranteed income products, diversified portfolios, and contingency reserves. Their chartered training ensures they can translate complex risk calculations into actionable recommendations that clients can understand and trust.

How a Chartered Retirement Planning Counselor Differs from Other Advisors

While many financial professionals claim expertise in retirement, the chartered designation sets a higher benchmark. Below are the distinguishing factors:

- Specialization vs. Generalization – General financial planners may offer retirement advice as part of a broader service suite. In contrast, a chartered retirement planning counselor’s entire curriculum revolves around retirement issues, providing deeper insight.

- Regulatory Oversight – The chartered body typically enforces a fiduciary standard and a code of ethics that can be more stringent than the standards governing non‑chartered advisors.

- Quantitative Rigor – The actuarial components of chartered training equip counselors with advanced mathematical tools for forecasting cash flows, a skill less common among generic advisors.

- Continuing Education – Mandatory CPD ensures that chartered counselors remain abreast of policy changes, product innovations, and demographic shifts that affect retirement planning.

For example, a client interested in a diversified, low‑maintenance approach might be guided toward a target‑date fund, but the chartered counselor would also evaluate the fund’s glide path, expense ratios, and alignment with the client’s risk profile. This level of scrutiny often goes beyond the surface‑level recommendation many non‑chartered advisors provide.

what is a chartered retirement planning counselor: Choosing the Right Professional

When selecting a chartered retirement planning counselor, consider the following criteria:

- Credentials Verification – Confirm that the counselor holds a valid charter from a reputable governing body.

- Experience with Similar Clients – Look for case studies or testimonials that demonstrate success with clients who share your financial situation.

- Fee Structure Transparency – Chartered counselors often work on a fee‑only basis, which can reduce conflicts of interest compared to commission‑based models.

- Communication Style – Effective counselors explain complex concepts in plain language, enabling you to make informed decisions without feeling overwhelmed.

Integrating a Chartered Retirement Planning Counselor into Your Financial Team

Retirement planning rarely occurs in isolation. Most individuals already have relationships with accountants, estate attorneys, and sometimes employer‑provided financial coaches. A chartered retirement planning counselor can act as the central hub, coordinating inputs from these various professionals to ensure a cohesive strategy.

For instance, the counselor might work with an accountant to align tax‑efficient withdrawal plans with the client’s broader tax filing strategy. Simultaneously, they could collaborate with an estate attorney to synchronize beneficiary designations across retirement accounts, life insurance policies, and trust structures. This integrated approach reduces the risk of contradictory advice and optimizes the overall financial picture.

what is a chartered retirement planning counselor: Real‑World Example

Consider Jane, a 58‑year‑old executive who plans to retire at 65. She has a defined‑benefit pension, a 401(k) with a substantial balance, and a taxable brokerage account. Jane also wishes to leave a legacy for her grandchildren. By engaging a chartered retirement planning counselor, Jane receives a detailed retirement income projection that includes:

- Projected pension payouts adjusted for cost‑of‑living increases.

- A recommended sequence of withdrawals that first taps taxable accounts, then tax‑deferred accounts, and finally tax‑free accounts to minimize tax exposure.

- An allocation of a portion of her 401(k) into a target‑date fund similar to the Vanguard Target Retirement 2025 Trust Select – Comprehensive Overview, providing a glide path that aligns with her retirement timeline.

- A legacy plan that incorporates a revocable living trust, ensuring assets pass to her grandchildren with reduced probate costs.

The outcome is a clear, actionable roadmap that balances income needs, risk management, tax efficiency, and legacy goals—all hallmarks of what a chartered retirement planning counselor delivers.

Future Trends Shaping the Role of Chartered Retirement Planning Counselors

As populations age and financial products evolve, the responsibilities of chartered retirement planning counselors will expand. Emerging trends include:

- Digital Planning Platforms – Advanced software can model thousands of retirement scenarios instantly. Counselors who master these tools will provide faster, more precise advice.

- Sustainable Investing – Growing interest in ESG (environmental, social, governance) criteria means retirees increasingly seek portfolios that reflect personal values while delivering returns.

- Longevity Insurance – Products that hedge against outliving assets are gaining popularity, and chartered counselors will play a key role in evaluating their suitability.

- Regulatory Shifts – Potential changes to required minimum distributions (RMDs) or tax treatment of retirement accounts will demand ongoing expertise from chartered professionals.

Staying ahead of these developments will reinforce why the chartered designation remains a trusted benchmark for retirement expertise.

In summary, understanding what is a chartered retirement planning counselor reveals a professional equipped with specialized education, rigorous certification, and a client‑centric ethic designed to navigate the complexities of retirement. Whether you are approaching retirement, already retired, or simply planning ahead, partnering with a chartered counselor can provide the strategic clarity and confidence needed to achieve a secure, fulfilling retirement journey.