Table of Contents

- t rowe price retirement 2035 fund: Core Investment Strategy

- t rowe price retirement 2035 fund: Risk Management Techniques

- Performance Overview and Historical Returns

- Fees, Expenses, and Cost Comparison

- Suitability for Different Investor Profiles

- Tax Considerations and Distribution Rules

- How to Invest in the t rowe price retirement 2035 fund

- Comparative Analysis with Peer Funds

- Vanguard Target Retirement 2035 Trust II

- State Street Target Retirement 2030 Fund

- Key Takeaways and Practical Steps

The search for a reliable target‑date retirement fund often leads investors to compare a handful of well‑known managers. Among those, the t rowe price retirement 2035 fund stands out as a product designed for investors who plan to retire around the year 2035. This article walks through the fund’s purpose, investment approach, risk profile, and how it fits within a broader retirement plan.

Target‑date funds, by definition, adjust their asset allocation over time. Early years feature a higher proportion of equities to capture growth, while later years shift toward bonds and cash equivalents to preserve capital. Understanding the specific glide path of a fund helps investors gauge whether it aligns with their personal risk tolerance and retirement timeline.

For those who are already considering a target‑date solution, it is useful to see how the t rowe price retirement 2035 fund compares with similar offerings, such as the Vanguard Target Retirement 2035 Trust II – In‑Depth Analysis or the JP Morgan Guide to Retirement 2025 – A Comprehensive Overview. By looking at the underlying methodology, investors can decide which manager’s philosophy best matches their expectations.

t rowe price retirement 2035 fund: Core Investment Strategy

The t rowe price retirement 2035 fund follows a diversified, actively managed strategy. Its portfolio is built around a mix of domestic and international equities, fixed‑income securities, and a modest allocation to real assets. The fund’s managers aim to balance growth potential with downside protection, adjusting exposure as the target date approaches.

Key elements of the strategy include:

- Equity Allocation: Early in the glide path, roughly 70‑80% of assets are placed in equities. This includes large‑cap U.S. stocks, mid‑ and small‑cap exposures, and a portion of international equities.

- Fixed‑Income Allocation: Bonds start at about 20‑30% of the portfolio, gradually rising to 50‑60% as the fund nears 2035. The fixed‑income mix features government, corporate, and high‑yield bonds.

- Real Assets and Alternatives: A small percentage, typically under 5%, is allocated to real estate investment trusts (REITs) and other real assets to provide inflation protection.

t rowe price retirement 2035 fund: Risk Management Techniques

Risk management is integral to the t rowe price retirement 2035 fund’s approach. The fund employs several techniques to mitigate volatility:

- Dynamic rebalancing that responds to market movements rather than strictly following a calendar schedule.

- Use of low‑correlation assets, such as international bonds, to smooth returns during periods of domestic market stress.

- Regular stress‑testing of the portfolio to ensure the glide path remains viable under various economic scenarios.

These measures help maintain a steady progression toward a more conservative allocation as the retirement date draws near.

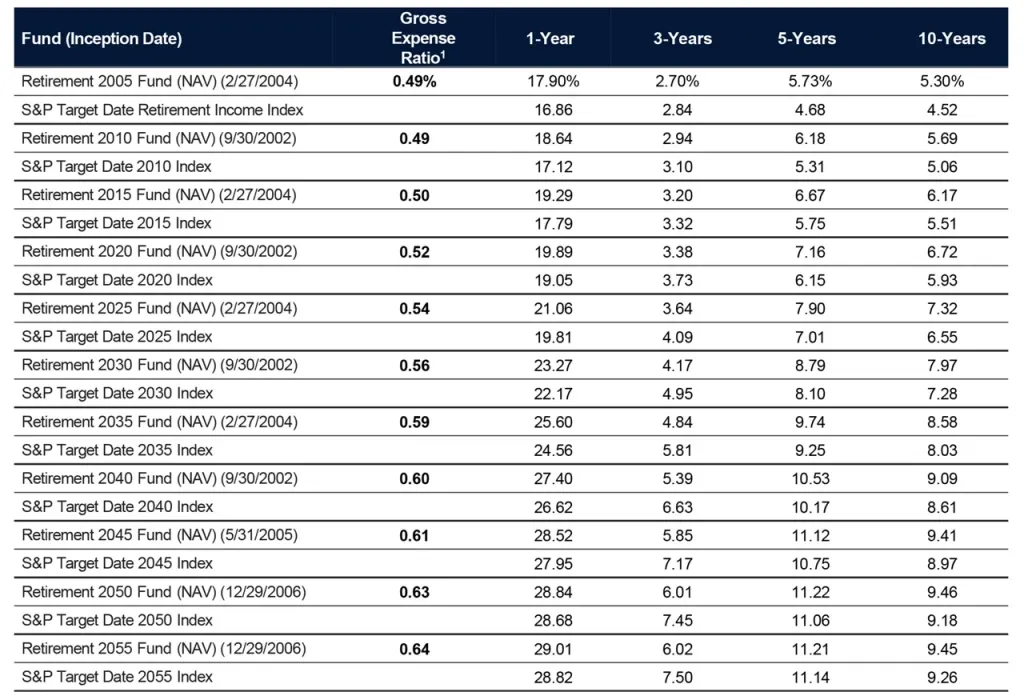

Performance Overview and Historical Returns

While past performance is not a guarantee of future results, it provides a useful benchmark. Since its inception, the t rowe price retirement 2035 fund has delivered annualized returns that are generally in line with peer groups. Over a 10‑year horizon, the fund has posted an average return of approximately 7.2%, outpacing many comparable target‑date offerings.

The fund’s performance is often evaluated against a benchmark blend of the MSCI World Index for equities and the Bloomberg Barclays U.S. Aggregate Bond Index for fixed income. In years of strong equity markets, the fund’s active management has contributed modest alpha, while during bond market downturns, the diversified approach has helped limit losses.

Fees, Expenses, and Cost Comparison

Cost is a crucial factor for long‑term investors. The t rowe price retirement 2035 fund carries an expense ratio of 0.68%, which includes management fees, administrative costs, and other operational expenses. While this is higher than some index‑based target‑date funds, it remains competitive among actively managed options.

Investors should also be aware of potential additional costs, such as transaction fees within the underlying holdings and any distribution fees that may apply if the fund is held in certain account types. Comparing the expense ratio with alternatives—like the Vanguard offering, which typically runs lower due to its index‑focused approach—helps investors decide if the active management premium is justified.

Suitability for Different Investor Profiles

The t rowe price retirement 2035 fund is best suited for investors who:

- Plan to retire around the year 2035, giving the fund roughly a decade of time to transition toward a more conservative allocation.

- Prefer an actively managed glide path that can adapt to market conditions rather than a static, rule‑based approach.

- Seek a diversified portfolio that includes both domestic and international exposure, along with a modest real‑asset component.

For small business owners exploring retirement solutions for their employees, the fund can be part of a broader plan. The Retirement Plans for Small Business Owners: A Comprehensive Guide discusses how target‑date funds like this one can be integrated into 401(k) or SIMPLE IRA structures.

Tax Considerations and Distribution Rules

Because the t rowe price retirement 2035 fund is typically held within tax‑advantaged accounts such as IRAs or employer‑sponsored plans, investors benefit from tax deferral on capital gains and dividends. However, when distributions begin, the tax treatment depends on the account type:

- Traditional IRA or 401(k): Distributions are taxed as ordinary income.

- Roth IRA: Qualified withdrawals are tax‑free, provided the five‑year rule and age requirements are met.

It is essential for investors to coordinate their withdrawal strategy with their overall tax plan to minimize unexpected liabilities.

How to Invest in the t rowe price retirement 2035 fund

Investors can purchase shares of the t rowe price retirement 2035 fund through several channels:

- Directly from T. Rowe Price’s online platform, where investors can set up automatic contributions.

- Through brokerage accounts that offer a wide range of mutual funds, such as Fidelity, Charles Schwab, or Vanguard.

- As part of an employer‑sponsored retirement plan, where the fund may be listed among the available target‑date options.

When opening an account, it is advisable to review the fund’s prospectus, which details the investment objectives, risks, and fees. Additionally, investors should confirm that the fund’s share class aligns with their account type to avoid unnecessary costs.

Comparative Analysis with Peer Funds

To put the t rowe price retirement 2035 fund into perspective, consider how it stacks up against two prominent peers:

Vanguard Target Retirement 2035 Trust II

Vanguard’s version relies heavily on index tracking, resulting in a lower expense ratio (around 0.15%). The glide path is more static, with less flexibility to respond to market shifts. Investors who prioritize low cost and are comfortable with a set allocation may favor Vanguard.

State Street Target Retirement 2030 Fund

The State Street fund targets a slightly earlier retirement date and maintains a higher bond allocation earlier in the glide path. Its expense ratio sits near 0.40%, offering a middle ground between active and passive strategies. This fund may appeal to investors who want a more conservative stance sooner.

By comparing these options, investors can determine whether the active management and diversified approach of the t rowe price retirement 2035 fund align with their personal risk appetite and cost expectations.

Key Takeaways and Practical Steps

Choosing a target‑date fund is a significant decision in a retirement plan. The t rowe price retirement 2035 fund provides an actively managed solution with a clear glide path, diversified asset mix, and moderate fees. For investors aiming to retire near 2035, it offers a blend of growth potential and risk mitigation that can adapt to changing market conditions.

To make an informed choice, follow these practical steps:

- Assess your retirement timeline and confirm that 2035 aligns with your expected retirement year.

- Evaluate your risk tolerance and decide whether an active glide path suits your comfort level.

- Compare expense ratios and historical performance with peer funds, such as Vanguard and State Street.

- Review the fund’s prospectus for detailed information on fees, allocation shifts, and distribution rules.

- Consider how the fund fits into your overall retirement strategy, including other investment accounts and tax considerations.

By taking a systematic approach, investors can position themselves for a smoother transition into retirement, leveraging the strengths of the t rowe price retirement 2035 fund while staying mindful of costs and risk.

Ultimately, the success of any retirement portfolio depends on disciplined saving, regular review, and the flexibility to adjust as life circumstances evolve. The t rowe price retirement 2035 fund is a tool that, when used wisely, can help investors stay on track toward their retirement goals.