Table of Contents

- What Is Errors and Omissions Insurance Real Estate Broker Coverage?

- Key Risks Covered by Errors and Omissions Insurance Real Estate Broker Policies

- How Errors and Omissions Insurance Real Estate Broker Policies Are Structured

- Policy Limits

- Deductibles

- Exclusions

- Claims‑Made vs. Occurrence

- Choosing the Right Errors and Omissions Insurance Real Estate Broker Policy

- Cost Factors Influencing Premiums for Errors and Omissions Insurance Real Estate Broker

- Real‑World Examples of Errors and Omissions Insurance in Action

- Case Study 1: Undisclosed Flood Zone

- Case Study 2: Missed Contract Deadline

- Maintaining Coverage: Best Practices for Ongoing Protection

- Regular Policy Reviews

- Continuing Education

- Documentation and Record Keeping

- Risk Management Programs

- Future Trends Impacting Errors and Omissions Insurance Real Estate Broker Coverage

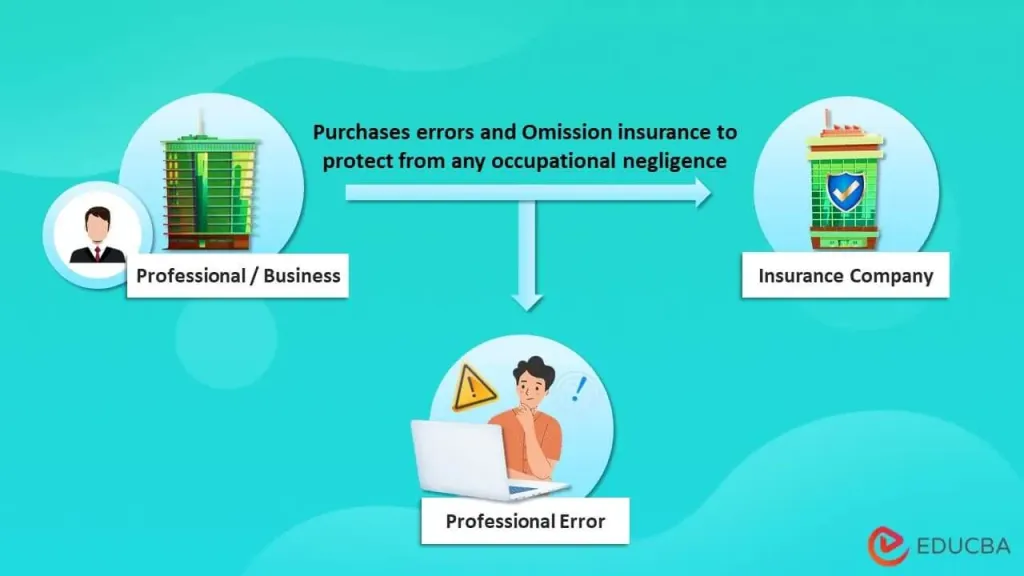

In the fast‑moving world of property transactions, real estate brokers constantly juggle negotiations, disclosures, and complex paperwork. Each step carries the potential for a misstep that could lead to costly lawsuits. To protect themselves, many brokers turn to a specialized form of liability coverage known as errors and omissions insurance. This type of policy is designed specifically for professionals who provide advice or services that, if performed incorrectly, could cause financial loss to a client.

Unlike general commercial liability insurance, which covers bodily injury or property damage, errors and omissions insurance focuses on mistakes, oversights, or negligence in the execution of professional duties. For a real estate broker, that could mean a missed deadline on a contract, a failure to disclose a known defect, or an inaccurate valuation that leads a buyer to overpay. The financial repercussions of such errors can be severe, ranging from settlement payments to legal fees that threaten the broker’s livelihood.

Understanding the nuances of errors and omissions insurance real estate broker coverage is therefore not a luxury—it’s a core component of running a sustainable brokerage. The following sections walk through the key concepts, typical policy features, and practical steps brokers should take to secure the right protection.

What Is Errors and Omissions Insurance Real Estate Broker Coverage?

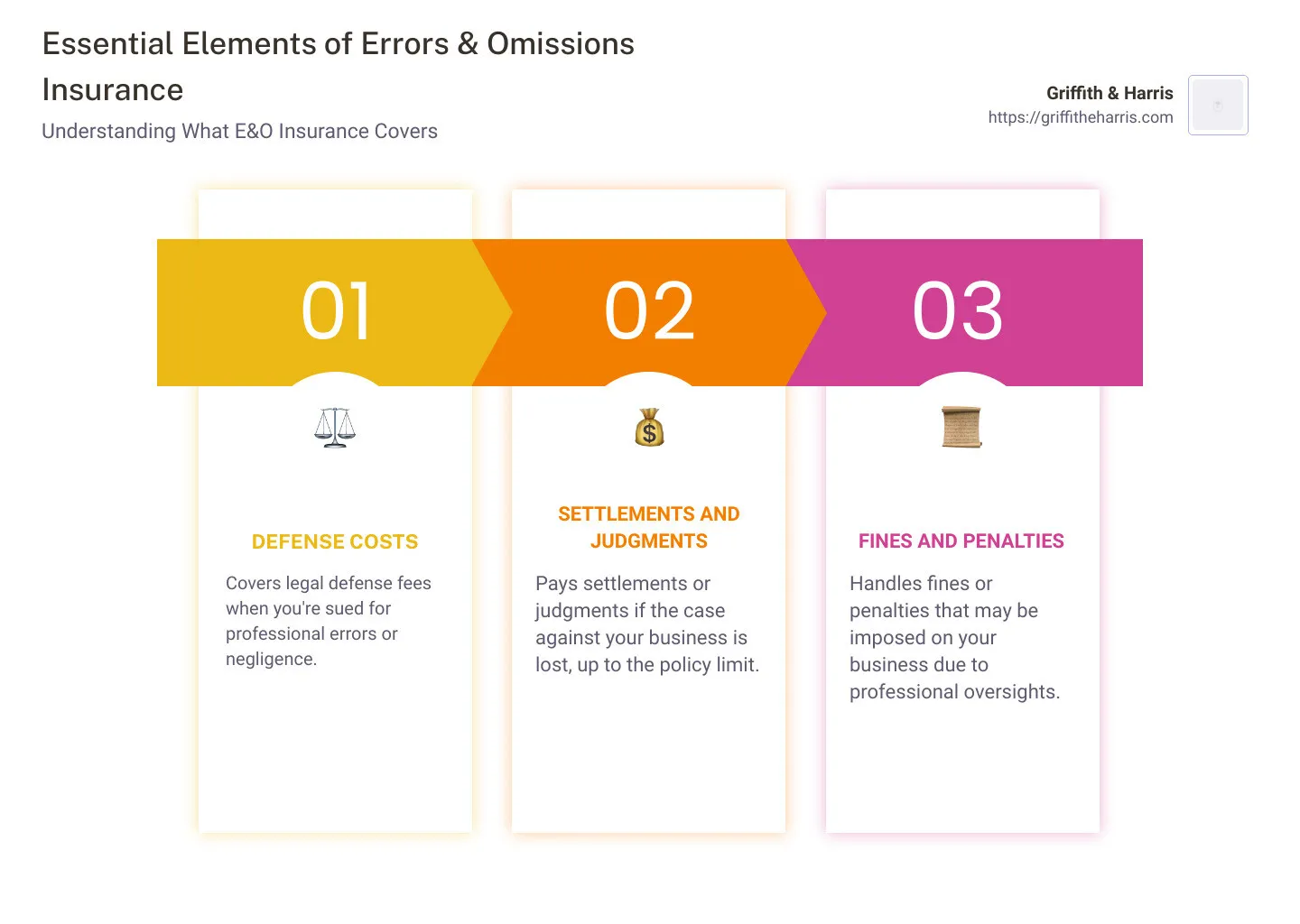

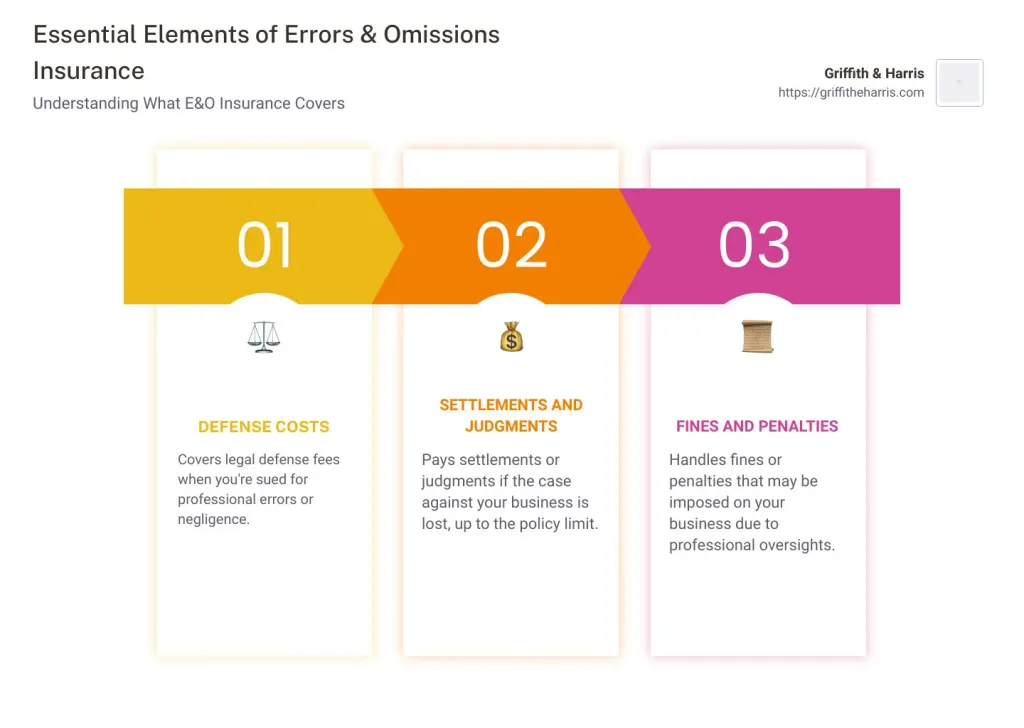

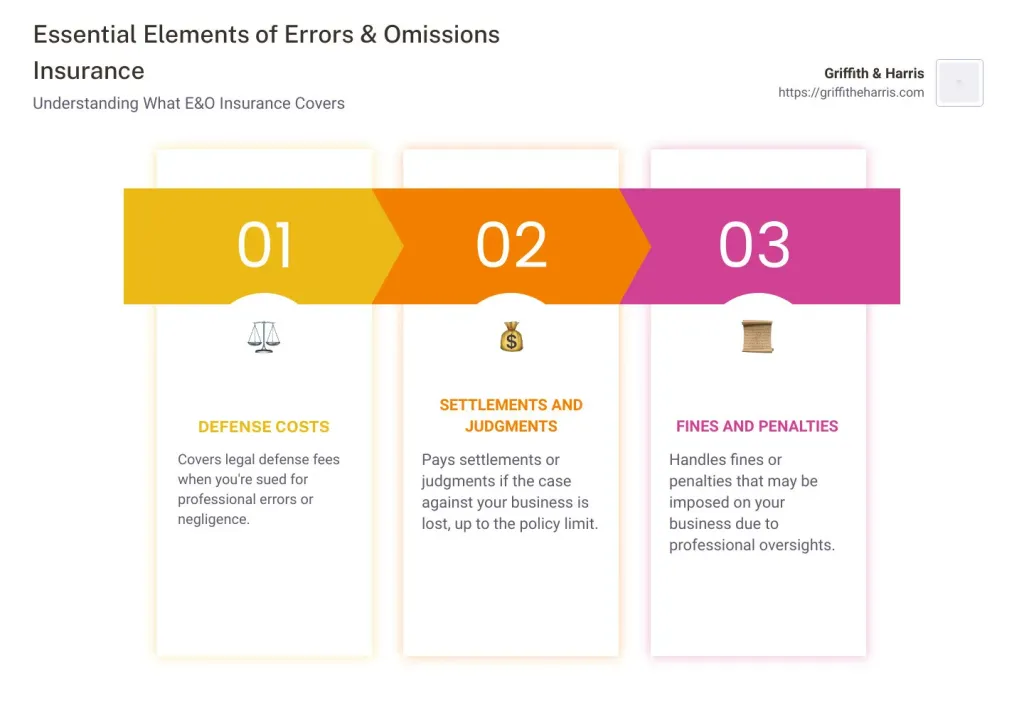

Errors and omissions insurance real estate broker policies are a form of professional liability insurance. They protect brokers against claims alleging inadequate work or negligent acts that cause financial loss to a client. The coverage typically includes:

- Legal Defense Costs: Fees for attorneys, court expenses, and settlement negotiations.

- Settlements and Judgments: Payments required to resolve a claim if the broker is found liable.

- Claims Made Basis: Most policies operate on a “claims‑made” trigger, meaning the claim must be reported while the policy is active.

Because the real estate industry is heavily regulated, many state licensing boards require brokers to maintain a minimum level of errors and omissions insurance. Even when not mandated, the peace of mind that comes from having a safety net is invaluable.

Key Risks Covered by Errors and Omissions Insurance Real Estate Broker Policies

Real estate brokers face a variety of exposure points. Below are the most common scenarios that trigger a claim:

- Misrepresentation of Property Facts: Providing inaccurate information about zoning, square footage, or structural condition.

- Failure to Disclose Known Defects: Overlooking material facts that a buyer would reasonably expect to be disclosed.

- Improper Handling of Funds: Errors in escrow accounting or trust fund management.

- Negligent Advice: Recommending a property that does not meet a client’s stated criteria, resulting in financial loss.

- Contractual Mistakes: Missing critical deadlines or failing to include essential clauses.

Each of these situations can lead to a lawsuit where the plaintiff seeks compensation for the alleged loss. Errors and omissions insurance real estate broker coverage steps in to absorb the financial impact, allowing the broker to focus on business continuity rather than legal battles.

How Errors and Omissions Insurance Real Estate Broker Policies Are Structured

When evaluating a policy, brokers should pay attention to the following components:

Policy Limits

Limits define the maximum amount an insurer will pay for a single claim and for the aggregate of all claims during the policy period. Typical limits for a broker range from $250,000 to $2 million, depending on the size of the brokerage and the volume of transactions.

Deductibles

The deductible is the amount the broker must pay out of pocket before the insurer steps in. Higher deductibles lower the premium but increase the broker’s exposure in a claim scenario.

Exclusions

Every policy contains exclusions—situations not covered. Common exclusions for errors and omissions insurance real estate broker policies include intentional wrongdoing, fraudulent acts, and claims arising from activities outside the scope of the broker’s license.

Claims‑Made vs. Occurrence

Most E&O policies for brokers are claims‑made, meaning coverage is triggered when a claim is made while the policy is active, regardless of when the alleged error occurred. Some insurers offer “extended reporting periods” (tail coverage) that protect against claims filed after the policy ends.

Choosing the Right Errors and Omissions Insurance Real Estate Broker Policy

Selecting an appropriate policy involves more than just comparing premium costs. Brokers should conduct a thorough risk assessment and consider the following steps:

- Assess Transaction Volume: Higher transaction counts increase exposure, warranting higher limits.

- Evaluate Service Scope: Brokers who also provide property management, consulting, or appraisal services may need broader coverage.

- Review State Requirements: Some jurisdictions impose minimum coverage amounts that must be met.

- Compare Insurers: Look for carriers with strong financial ratings and experience handling real estate claims.

- Consult a Specialist: Insurance brokers who specialize in real estate can tailor policies to fit unique needs.

For a detailed walkthrough of the selection process, see Real Estate Broker E&O Insurance: A Comprehensive Guide, which outlines the critical questions every broker should ask.

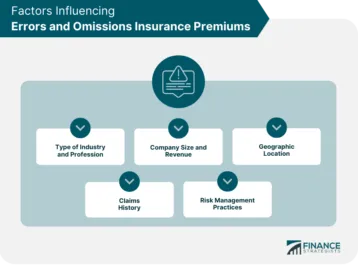

Cost Factors Influencing Premiums for Errors and Omissions Insurance Real Estate Broker

Premiums are calculated based on a blend of objective and subjective factors. Understanding these drivers helps brokers manage costs without sacrificing protection.

- Claims History: Brokers with prior claims may face higher rates.

- Years in Business: Established firms often receive discounts due to proven track records.

- Location: Markets with higher litigation rates or property values can increase premiums.

- Revenue and Transaction Size: Larger deals imply greater potential loss, affecting pricing.

- Risk Management Practices: Demonstrated use of compliance checklists, continuing education, and internal audits can lead to premium reductions.

Investing in robust risk mitigation—such as standardized disclosure forms and regular training—can lower the perceived risk for insurers, ultimately resulting in more favorable premium rates.

Real‑World Examples of Errors and Omissions Insurance in Action

To illustrate the practical benefits, consider these anonymized case studies:

Case Study 1: Undisclosed Flood Zone

A broker failed to disclose that a property was located within a high‑risk flood zone. After a severe storm caused damage, the buyer sued for the cost of additional insurance and repairs. The broker’s errors and omissions insurance real estate broker policy covered the $150,000 settlement and legal fees, preserving the brokerage’s cash flow.

Case Study 2: Missed Contract Deadline

In a multi‑unit commercial sale, the broker overlooked a deadline for a financing contingency. The buyer lost the financing opportunity and sued for lost profit. The insurer paid the $85,000 judgment, and the broker was able to maintain client relationships by demonstrating responsibility.

These scenarios highlight how errors and omissions insurance real estate broker coverage can act as a financial lifeline when unexpected disputes arise.

Maintaining Coverage: Best Practices for Ongoing Protection

Obtaining a policy is only the first step. Continuous compliance ensures the coverage remains effective throughout the broker’s career.

Regular Policy Reviews

Review the policy at least annually, especially after significant business changes such as mergers, expansion into new services, or entering different states.

Continuing Education

Many professional associations require continuing education. Completing courses on legal updates and ethical standards not only reduces risk but may also qualify brokers for premium discounts.

Documentation and Record Keeping

Maintain organized records of all communications, disclosures, and contracts. Accurate documentation is a critical defense tool if a claim arises.

Risk Management Programs

Implement systematic checks, such as double‑review of disclosures and standardized client intake forms. These procedures can catch errors before they become claims.

For a broader perspective on how brokers can integrate risk management with their insurance strategy, refer to e&o Insurance for Real Estate Brokers – Essential Coverage Guide.

Future Trends Impacting Errors and Omissions Insurance Real Estate Broker Coverage

The real estate landscape is evolving, and several emerging trends may influence the scope and cost of errors and omissions insurance for brokers.

- Technology Integration: The rise of AI‑driven valuation tools introduces new liability concerns. Insurers are beginning to consider technology‑related errors when underwriting policies.

- Virtual Transactions: Remote closings and digital signatures have become standard. While convenient, they raise questions about data security and the adequacy of electronic disclosures.

- Regulatory Changes: Some states are tightening disclosure requirements, potentially expanding the range of claims that fall under errors and omissions coverage.

- Environmental Risks: Increasing awareness of climate‑related hazards may lead to more claims involving undisclosed environmental issues, prompting insurers to adjust policy language.

Staying informed about these developments allows brokers to anticipate shifts in coverage needs and collaborate proactively with insurers.

In summary, errors and omissions insurance real estate broker coverage serves as a critical safeguard against the financial fallout of professional mistakes. By understanding policy structures, evaluating risk exposure, and maintaining diligent risk management practices, brokers can protect their businesses while continuing to serve clients with confidence. The investment in a well‑tailored E&O policy not only meets regulatory obligations but also reinforces the broker’s reputation as a responsible and trustworthy professional in a competitive market.