Table of Contents

- Overview of t rowe price retirement 2025 fund

- Investment Strategy and Asset Allocation

- t rowe price retirement 2025 fund – Fees and Expenses

- Performance Track Record and Risk Profile

- How the Fund Fits Into a Retirement Plan

- t rowe price retirement 2025 fund vs Similar Funds

- Practical Tips for Managing Your Investment in t rowe price retirement 2025 fund

When investors look beyond the immediate horizon and begin to plan for a retirement that will likely start around 2025, many turn to target‑date funds as a convenient, “set‑and‑forget” solution. Among the most discussed options is the t rowe price retirement 2025 fund. This fund, managed by a long‑standing asset‑management firm, promises a glide‑path that automatically shifts from growth‑focused equities to more conservative bonds as the target year approaches. Understanding how the fund operates, its historical performance, and the role it can play in a broader retirement strategy is essential for anyone considering it as a core holding.

Target‑date funds have grown in popularity because they simplify the asset‑allocation decision for investors who may not have the time or expertise to rebalance portfolios manually. However, the convenience comes with trade‑offs: investors must trust the fund manager’s assumptions about market cycles, risk tolerance, and the appropriate timing of the shift toward safety. The t rowe price retirement 2025 fund embodies these trade‑offs, offering a specific set of decisions made by T. Rowe Price’s investment team.

In the sections that follow, we will dissect the fund’s strategy, examine its performance record, compare its expense structure with peers, and discuss how it can be integrated into a comprehensive retirement plan. The goal is to provide a factual, narrative‑driven overview that equips readers with the knowledge needed to decide whether this fund aligns with their retirement goals.

Overview of t rowe price retirement 2025 fund

The t rowe price retirement 2025 fund is classified as a target‑date mutual fund. Its primary objective is to deliver a total return—capital appreciation plus income—that meets or exceeds the needs of investors planning to retire near the year 2025. The fund’s glide‑path, a predefined schedule of asset‑allocation changes, is designed to become progressively more conservative as the target date draws near.

At inception, the fund’s portfolio is heavily weighted toward U.S. and international equities, reflecting the higher risk tolerance of younger investors who have a longer time horizon to absorb market volatility. Over the subsequent years, the allocation gradually tilts toward fixed‑income securities, including government and corporate bonds, and eventually incorporates cash equivalents and short‑term instruments as 2025 approaches.

Key attributes of the fund include:

- Managed by T. Rowe Price, a firm with more than eight decades of investment experience.

- Designed for investors who anticipate needing retirement income beginning in 2025.

- Automatic rebalancing that follows a glide‑path aligned with the fund’s target date.

- Diversified exposure across asset classes, sectors, and geographies.

Investment Strategy and Asset Allocation

The fund’s investment strategy hinges on a disciplined, forward‑looking asset‑allocation model. Early in the fund’s life cycle, roughly 80‑90% of assets are allocated to equities, split between U.S. large‑cap, mid‑cap, small‑cap, and international stocks. This equity‑heavy stance aims to capture growth opportunities while the investor’s retirement horizon is still distant.

As the fund approaches its 2025 target, the allocation gradually shifts. By the time the fund reaches its “retirement” phase—typically a few years before 2025—the equity component is reduced to around 40‑50%, with the remainder placed in a mix of intermediate‑term bonds, short‑term bonds, and cash equivalents. This transition is intended to lower volatility and preserve capital as investors prepare to draw down their savings.

The glide‑path is not static; T. Rowe Price reviews its assumptions periodically and may adjust the schedule to reflect evolving market conditions or demographic insights. The fund also employs active management within each asset class, allowing portfolio managers to select securities they believe will outperform their benchmarks.

t rowe price retirement 2025 fund – Fees and Expenses

Expense ratios are a critical consideration for any mutual fund, especially for long‑term investors. The t rowe price retirement 2025 fund carries an expense ratio that sits near the middle of the industry range for target‑date funds. While exact figures can vary slightly from year to year, investors typically see an annual expense of around 0.65% to 0.75% of assets under management.

These fees cover management, administration, and operational costs. Because the fund is actively managed, its expenses are higher than those of passively managed index funds but lower than many specialty funds that employ more intensive research resources. Investors should weigh the fee structure against the potential benefits of professional oversight and the fund’s historical risk‑adjusted returns.

Performance Track Record and Risk Profile

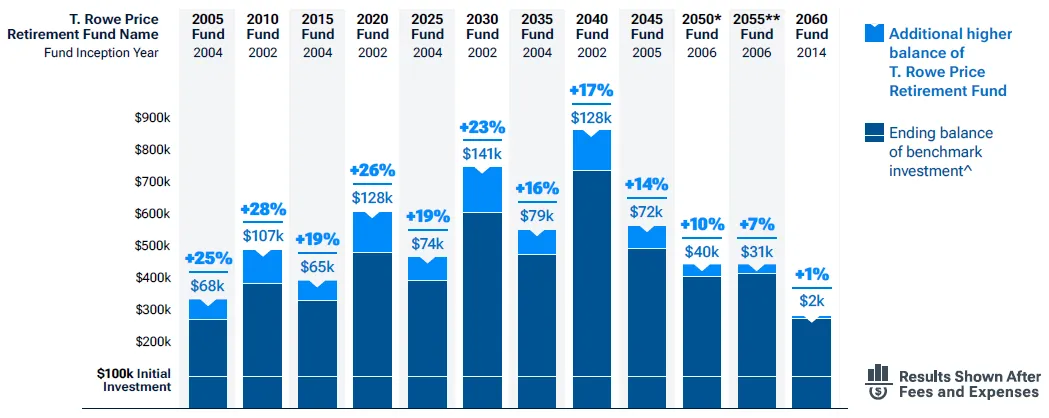

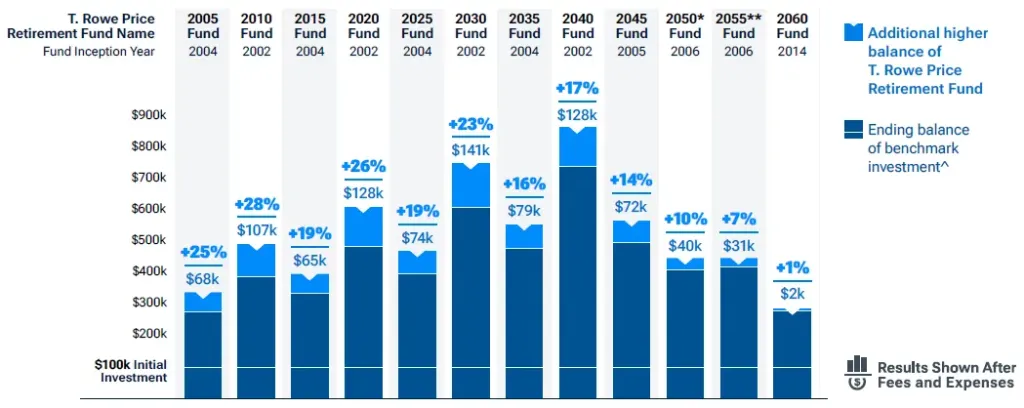

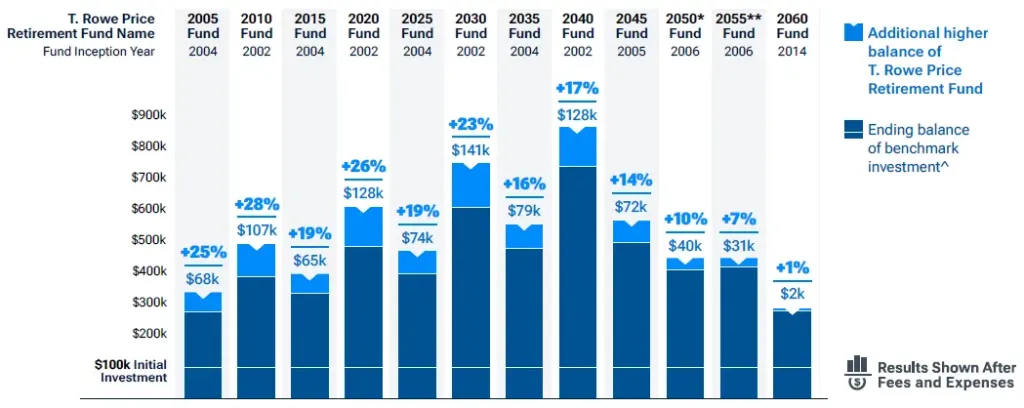

Historical performance offers a window into how the fund has navigated various market cycles. Since its launch, the t rowe price retirement 2025 fund has delivered an average annual return that closely tracks the blended performance of its underlying equity and bond holdings. During bullish periods, the equity portion has driven higher returns, while during market downturns, the bond allocation has helped cushion losses.

When comparing the fund’s risk profile to a pure equity index, volatility (as measured by standard deviation) is noticeably lower, reflecting the moderating influence of the fixed‑income component. This risk mitigation aligns with the fund’s purpose: to provide a smoother investment experience for investors who are nearing retirement and cannot afford large swings in portfolio value.

Investors seeking a more detailed benchmark can refer to the Vanguard Target Retirement 2025 Fund Fact Sheet – In‑Depth Review, which offers a comparable glide‑path for a direct peer comparison.

How the Fund Fits Into a Retirement Plan

Incorporating the t rowe price retirement 2025 fund into a broader retirement strategy requires an understanding of the investor’s overall financial picture. For individuals whose retirement timeline aligns closely with 2025, the fund can serve as a core holding, providing diversified exposure and an automatic rebalancing mechanism.

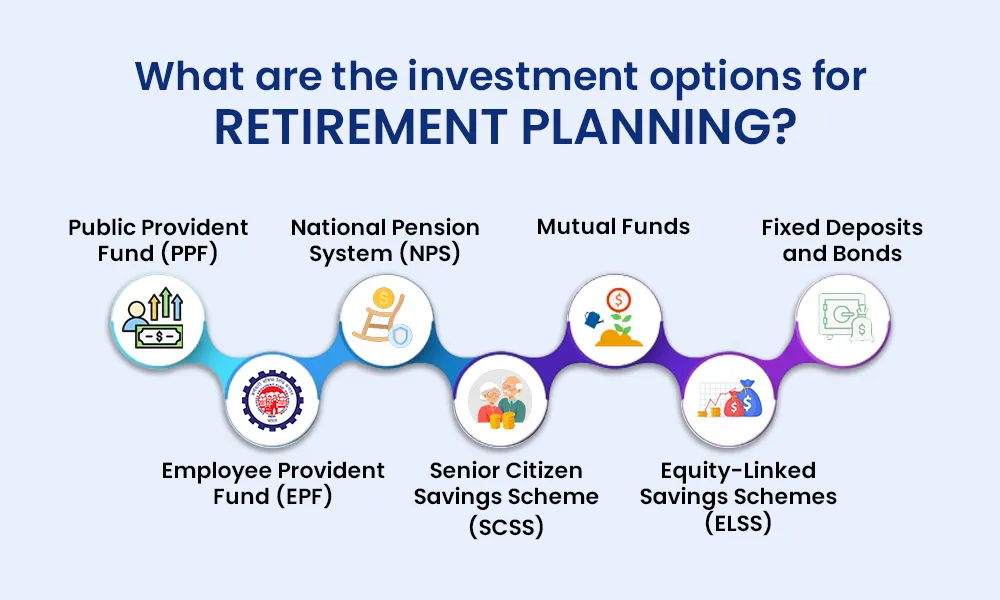

However, many retirees benefit from a layered approach: combining a target‑date fund with other vehicles such as individual stocks, bond ladders, or annuities to tailor income streams and manage longevity risk. Consulting a qualified professional can help identify the optimal mix. The How to Find a Retirement Advisor – A Step‑by‑Step Guide offers practical steps for locating an advisor who can assess personal circumstances and suggest appropriate allocations.

Another consideration is the tax treatment of the fund. Held within a tax‑advantaged account—such as a 401(k) or traditional IRA—the fund’s capital gains and dividends are tax‑deferred, which can enhance compound growth. In a taxable brokerage account, investors should be mindful of the fund’s turnover rate, as higher turnover can generate taxable events.

t rowe price retirement 2025 fund vs Similar Funds

When evaluating alternatives, the t rowe price retirement 2025 fund often gets compared to other 2025 target‑date offerings, such as the Vanguard Target Retirement 2025 Fund. While both share a similar glide‑path, differences emerge in management style, expense ratios, and underlying holdings. For instance, Vanguard’s approach leans more heavily on index tracking, resulting in lower fees, whereas T. Rowe Price applies an active strategy that may capture incremental alpha but at a higher cost.

For a broader historical perspective, readers may also explore the t Rowe Price Retirement 2020 TRRBX – Comprehensive Overview, which provides insights into how the firm’s earlier target‑date products performed during different market environments.

Practical Tips for Managing Your Investment in t rowe price retirement 2025 fund

- Regularly Review Your Asset Allocation: Even though the fund rebalances automatically, it’s wise to assess whether the glide‑path still matches your risk tolerance as you approach retirement.

- Consider Supplemental Savings: Relying solely on a target‑date fund may not be sufficient for all retirement goals. Evaluate whether additional savings or alternative investments are needed.

- Monitor Expense Ratios: Keep an eye on fee changes. A modest increase can erode returns over a long horizon.

- Plan for Withdrawal Strategies: As the fund moves into its retirement phase, think about how you will draw income—whether through systematic withdrawals, annuitization, or a combination.

For those interested in a holistic view of retirement income, the The Definitive Guide to Retirement Income – A Complete Roadmap offers a comprehensive framework that can be combined with the insights provided here.

In sum, the t rowe price retirement 2025 fund presents a solid option for investors targeting a retirement window around 2025. Its active management, disciplined glide‑path, and reputable oversight make it a competitive choice among target‑date funds. Nevertheless, prospective investors should weigh the fund’s expense structure, compare it against passive alternatives, and ensure it fits within a diversified retirement plan that accounts for tax considerations, income needs, and personal risk tolerance. By approaching the decision with a clear understanding of the fund’s mechanics and performance history, investors can make a more informed choice that aligns with their long‑term financial objectives.