Table of Contents

- Retirement Options for Small Business Owners: Overview of Core Plans

- Retirement Options for Small Business Owners – Solo 401(k) Plans

- Retirement Options for Small Business Owners – SIMPLE IRA

- Retirement Options for Small Business Owners – SEP IRA

- Retirement Options for Small Business Owners – Defined Benefit Plans

- Choosing the Right Plan: Factors to Consider

- Implementation Steps for Small Business Retirement Plans

- 1. Assess Business Structure and Eligibility

- 2. Consult a Financial Advisor or CPA

- 3. Select a Plan Provider

- 4. Draft and File Plan Documents

- 5. Communicate with Employees

- 6. Monitor and Adjust Annually

- Tax Advantages and Strategic Benefits

- Integrating Retirement Planning with Business Succession

- Common Mistakes to Avoid

- Underfunding the Plan

- Neglecting Employee Education

- Overlooking Compliance Deadlines

- Choosing the Wrong Investment Options

- Future Trends in Small Business Retirement Planning

Running a small business demands juggling many responsibilities—from daily operations to strategic growth. Amidst the hustle, planning for a secure retirement often falls to the bottom of the to‑do list. Yet, the financial independence that comes after years of hard work hinges on making informed decisions today. Understanding the range of retirement options for small business owners is essential for building a safety net that aligns with both personal goals and business realities.

This article walks you through the most viable retirement vehicles, highlights key tax advantages, and offers practical steps to implement a plan that fits your unique situation. Whether you operate a solo consultancy, a family‑run shop, or a growing startup, the choices outlined here can help you transition smoothly from active entrepreneurship to a comfortable retirement.

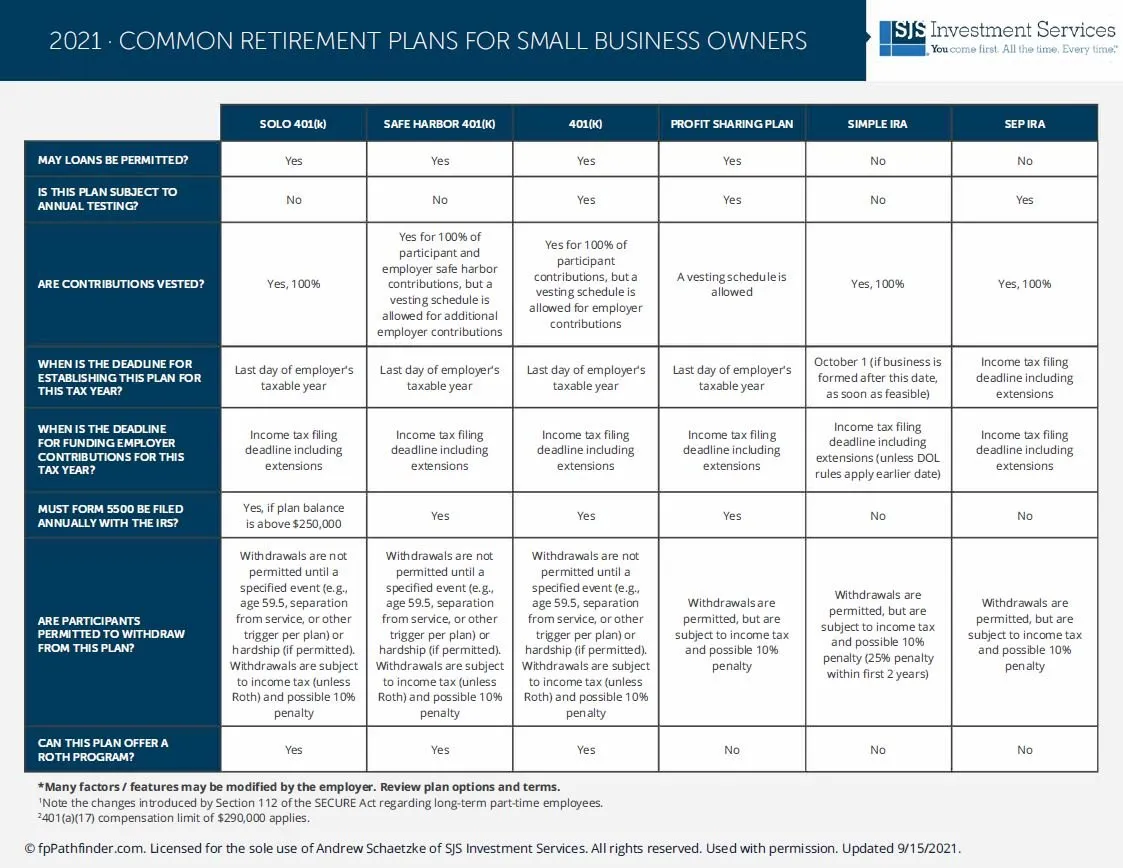

Retirement Options for Small Business Owners: Overview of Core Plans

Small business owners have access to a variety of retirement plans, each with distinct contribution limits, eligibility rules, and administrative requirements. Selecting the right vehicle depends on factors such as business size, cash flow, employee count, and long‑term financial objectives.

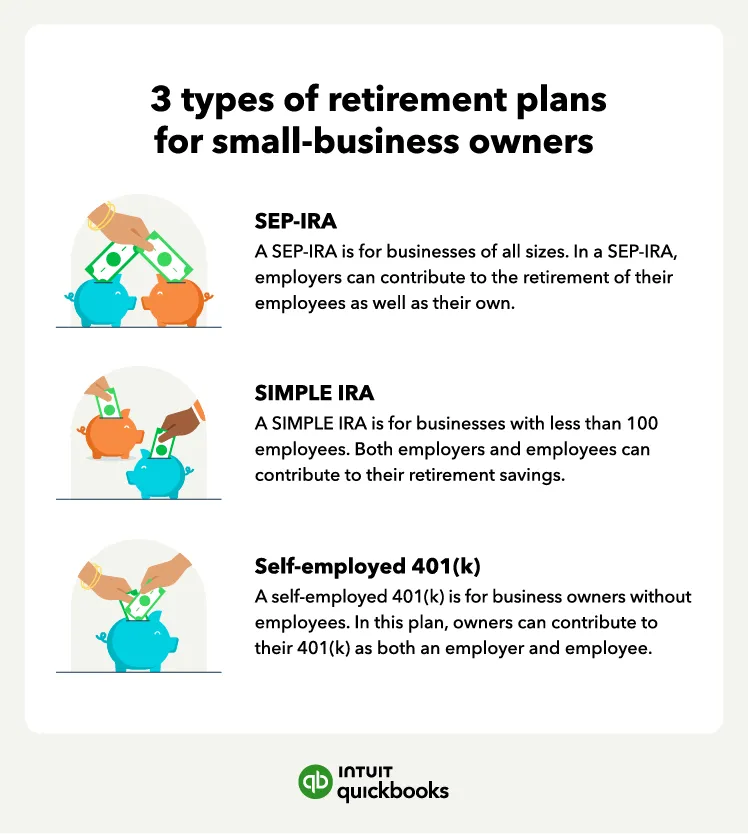

Retirement Options for Small Business Owners – Solo 401(k) Plans

A Solo 401(k) is designed for self‑employed individuals or business owners with no full‑time employees (apart from a spouse). It combines employee deferral contributions with employer profit‑sharing, allowing high contribution limits—up to $66,000 for 2023, with an additional $7,500 catch‑up contribution if you’re 50 or older. The plan offers flexible investment choices and can be set up quickly through most financial institutions.

Retirement Options for Small Business Owners – SIMPLE IRA

The Savings Incentive Match Plan for Employees (SIMPLE) IRA is suitable for businesses with 100 or fewer employees. Employers must either match employee contributions dollar‑for‑dollar up to 3% of compensation or make a fixed 2% nonelective contribution. Employees can defer up to $15,500 in 2023, plus a $3,500 catch‑up contribution for those 50+. Simplicity in administration makes it attractive for owners who lack the resources for more complex plans.

Retirement Options for Small Business Owners – SEP IRA

The Simplified Employee Pension (SEP) IRA allows employers to contribute up to 25% of an employee’s compensation or $66,000 (whichever is less) for 2023. Contributions are discretionary, giving owners the ability to vary funding based on yearly profitability. SEP IRAs are easy to set up, require minimal paperwork, and can be a powerful tool for owners who want to maximize retirement savings when cash flow permits.

Retirement Options for Small Business Owners – Defined Benefit Plans

For owners seeking a predictable retirement income, defined benefit (pension) plans offer a fixed payout based on salary history and years of service. While administration is more complex and actuarial calculations are required, these plans enable substantially higher contribution limits—sometimes exceeding $200,000 annually—making them ideal for high‑earning owners who wish to accelerate retirement savings.

Choosing the Right Plan: Factors to Consider

When evaluating retirement options for small business owners, weigh the following considerations:

- Cash Flow Stability: Plans with discretionary contributions, like SEP IRAs, align with variable earnings.

- Employee Participation: If you have a team, a SIMPLE IRA or a traditional 401(k) may enhance employee recruitment and retention.

- Administrative Burden: Solo 401(k)s and SIMPLE IRAs generally require less paperwork than defined benefit plans.

- Tax Implications: Employer contributions are tax‑deductible, reducing taxable income while building retirement assets.

- Long‑Term Goals: Consider whether you aim for modest growth or accelerated accumulation, which influences plan selection.

Implementation Steps for Small Business Retirement Plans

Transitioning from concept to execution involves several key steps. Below is a practical roadmap for owners ready to adopt a retirement plan.

1. Assess Business Structure and Eligibility

Determine whether your business qualifies as a sole proprietorship, partnership, S‑corp, or LLC. Eligibility for certain plans—like Solo 401(k)s—depends on having no full‑time employees. Reviewing the comprehensive guide to retirement plans for small business owners can clarify nuances.

2. Consult a Financial Advisor or CPA

Engaging a professional ensures compliance with IRS regulations and helps tailor the plan to your financial situation. For owners interested in technology‑driven solutions, exploring retirement income planning software for advisors can streamline calculations and projections.

3. Select a Plan Provider

Choose a reputable financial institution or third‑party administrator (TPA). A TPA can handle compliance testing, filing Form 5500, and participant communication. The complete guide to third‑party administrators for retirement plans offers insights on evaluating providers.

4. Draft and File Plan Documents

Prepare the plan adoption agreement, summary plan description, and trust agreement (if applicable). These documents must be filed with the IRS and, in some cases, the Department of Labor.

5. Communicate with Employees

Transparent communication fosters employee buy‑in. Explain contribution options, vesting schedules, and investment choices. Providing educational webinars or printed guides can increase participation rates.

6. Monitor and Adjust Annually

Review contributions, investment performance, and regulatory changes each year. Adjust employer contributions or plan features as needed to stay aligned with business goals.

Tax Advantages and Strategic Benefits

Retirement options for small business owners are not merely savings vehicles; they also serve as strategic tax tools.

- Deductible Contributions: Employer contributions reduce taxable income, providing immediate tax relief.

- Tax‑Deferred Growth: Investments grow tax‑free until withdrawal, enhancing compounding effects.

- Roth Options: Some plans, like Roth 401(k)s, allow after‑tax contributions, enabling tax‑free withdrawals in retirement.

- Employer Tax Credits: The SECURE Act offers a credit of up to $5,000 for the first three years of a new retirement plan.

These benefits can improve cash flow during profitable years while building a robust retirement nest egg.

Integrating Retirement Planning with Business Succession

For many owners, retirement planning intertwines with succession strategies. A well‑structured retirement plan can facilitate a smooth ownership transition by:

- Providing liquidity to fund buy‑outs.

- Offering a tax‑efficient way to distribute equity to family members.

- Ensuring that key employees remain motivated during the handover period.

Coordinating retirement savings with succession planning helps protect both personal and business assets, reducing the risk of financial disruption.

Common Mistakes to Avoid

Even seasoned entrepreneurs can stumble when setting up retirement options for small business owners. Below are pitfalls to watch out for:

Underfunding the Plan

Contributing less than the maximum allowable amount may limit tax benefits and slow wealth accumulation. Regularly revisit contribution levels to align with cash flow.

Neglecting Employee Education

Failing to inform staff about plan features can result in low participation, undermining the plan’s effectiveness as a recruitment and retention tool.

Overlooking Compliance Deadlines

Missing filing deadlines for Form 5500 or failing to perform required nondiscrimination tests can lead to penalties. Partnering with a qualified TPA mitigates this risk.

Choosing the Wrong Investment Options

Offering overly aggressive or overly conservative investment choices may not match employee risk tolerance. Provide a balanced menu and educational resources.

Future Trends in Small Business Retirement Planning

Technology continues to reshape how small business owners approach retirement. Emerging trends include:

- Robo‑Advisors: Automated investment platforms tailor portfolios based on risk profiles, reducing management fees.

- Digital Enrollment: Cloud‑based portals simplify employee onboarding and contribution adjustments.

- ESG Investing: Growing demand for environmental, social, and governance (ESG) funds allows owners to align investments with personal values.

- Hybrid Plans: Combining features of 401(k)s and cash‑balance pensions offers flexibility and predictable outcomes.

Staying informed about these developments can give small business owners a competitive edge and enhance the overall retirement experience.

In summary, the landscape of retirement options for small business owners is rich with possibilities. From Solo 401(k)s and SIMPLE IRAs to sophisticated defined benefit plans, each vehicle offers unique benefits that can be matched to an owner’s financial situation, employee structure, and long‑term goals. By conducting a thorough assessment, seeking professional counsel, and committing to regular plan maintenance, owners can secure a financially stable retirement while simultaneously strengthening their business’s appeal to current and future employees.