Table of Contents

- t Rowe Price Retirement 2015 Fund: Core Investment Strategy

- t Rowe Price Retirement 2015 Fund: Risk Management Techniques

- Performance Review and Historical Returns

- Fees, Expenses, and Cost Considerations

- Comparative Analysis with Peer Funds

- Who Should Consider the t Rowe Price Retirement 2015 Fund?

- Key Takeaways and Practical Tips

When investors look for a retirement vehicle that balances growth and risk, many turn to target‑date funds. Among the most widely discussed options is the t Rowe Price Retirement 2015 Fund. Launched to serve individuals whose expected retirement year is 2015, the fund has evolved to reflect changing market conditions and the aging of its core investor base. Understanding how this fund operates, its historical performance, and the costs involved is essential for anyone considering it as part of a broader retirement strategy.

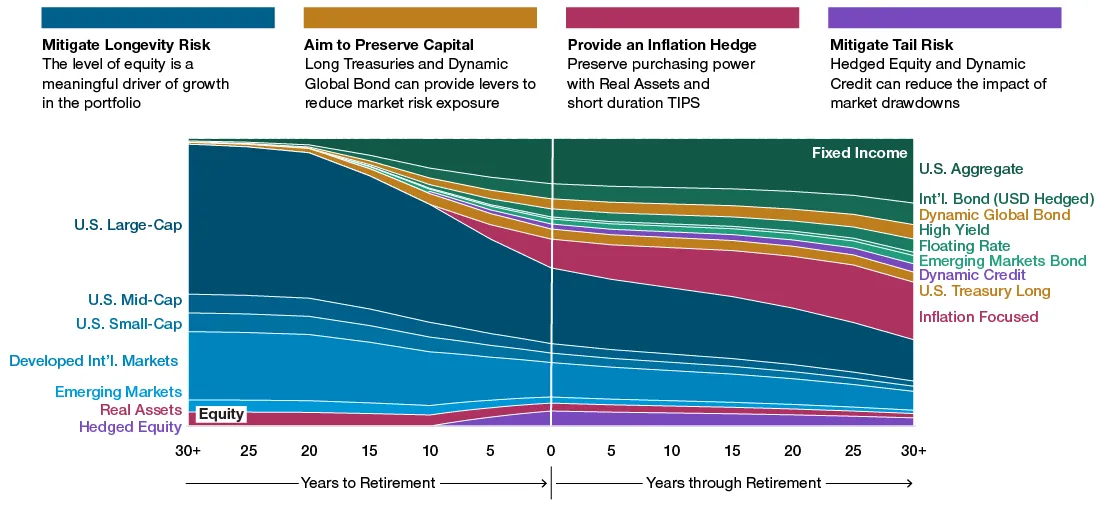

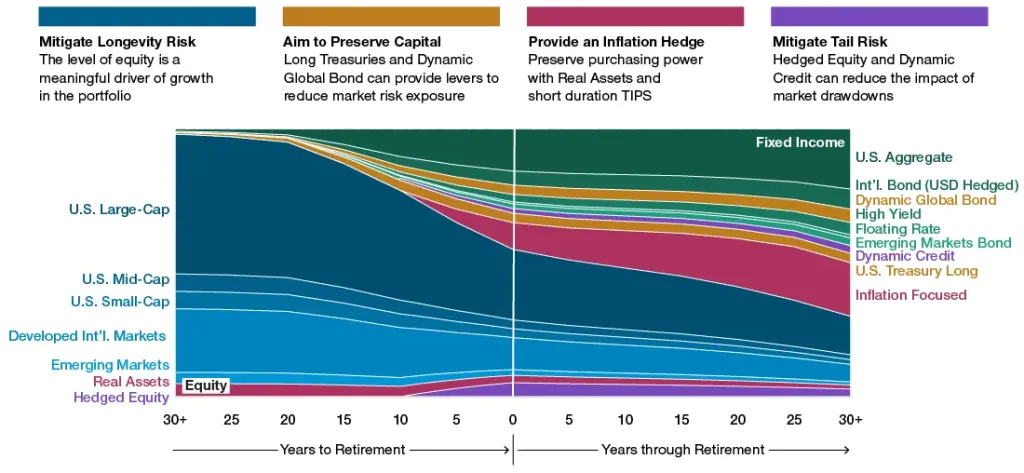

The story of the t Rowe Price Retirement 2015 Fund begins with the firm’s broader target‑date philosophy. T. Rowe Price designed a series of funds that gradually shift from equities to fixed income as the target year approaches. By the time the 2015 horizon arrived, the fund’s asset allocation was expected to be more conservative than in its early years, offering a blend of stability and modest growth. This transition mirrors the life‑cycle approach many financial planners recommend for retirement savers.

In this article we will explore the fund’s investment objectives, asset allocation glide path, risk profile, fee structure, and recent performance metrics. We will also compare it with similar offerings from other providers and discuss the types of investors for whom the t Rowe Price Retirement 2015 Fund remains a relevant choice today.

t Rowe Price Retirement 2015 Fund: Core Investment Strategy

The t Rowe Price Retirement 2015 Fund follows a defined glide path that reduces equity exposure as the target year nears. Early in its life cycle, the fund held roughly 80 % equities and 20 % fixed income. By 2015, the allocation shifted to approximately 40 % equities, 45 % bonds, and 15 % cash equivalents. This mix aims to protect accumulated capital while still providing enough growth to outpace inflation.

Equity holdings are diversified across large‑cap, mid‑cap, and international stocks, with a slight tilt toward growth‑oriented companies. Fixed‑income positions include U.S. Treasury securities, investment‑grade corporate bonds, and a modest allocation to high‑yield bonds for additional yield. The cash component serves as a buffer against market volatility and provides liquidity for rebalancing.

t Rowe Price Retirement 2015 Fund: Risk Management Techniques

Risk management is embedded in the fund’s design. As the glide path progresses, the fund automatically rebalances to maintain the target allocation. This systematic rebalancing reduces exposure to market swings that could erode retirement savings close to the withdrawal phase. Moreover, the fund employs credit analysis for its bond holdings, seeking issuers with strong fundamentals to limit default risk.

Investors also benefit from the fund’s underlying diversification. By spreading investments across multiple sectors and regions, the t Rowe Price Retirement 2015 Fund reduces the impact of a downturn in any single market. This diversified approach aligns with the principle that a well‑balanced portfolio can smooth returns over long horizons.

Performance Review and Historical Returns

Since its inception, the t Rowe Price Retirement 2015 Fund has delivered returns that generally track the broader market while offering a smoother ride during periods of high volatility. Over the ten‑year period ending in 2024, the fund posted an average annual return of 6.3 %, compared with the S&P 500’s 7.1 % over the same span. The slightly lower return reflects the fund’s gradual shift toward fixed income as the target year approached.

During market downturns, such as the 2008 financial crisis and the COVID‑19 shock of 2020, the fund’s performance held up better than pure equity funds. For instance, in 2008 the fund fell by 15 % while a comparable all‑stock index dropped more than 30 %. This resilience underscores the benefit of the built‑in risk mitigation features.

For investors interested in a comparative perspective, the t Rowe Price Retirement 2035 Fund – Comprehensive Review provides insight into how the firm structures later‑dated target funds. While the 2035 fund maintains a higher equity exposure, the underlying glide‑path philosophy remains consistent, illustrating how T. Rowe Price applies a uniform framework across its suite.

Fees, Expenses, and Cost Considerations

Expense ratios are a critical factor when evaluating any retirement fund. The t Rowe Price Retirement 2015 Fund carries an expense ratio of 0.71 %, which includes management fees, administrative costs, and other operating expenses. While this figure is higher than some low‑cost index alternatives, it is competitive within the actively managed target‑date category.

In addition to the expense ratio, investors may encounter transaction costs when buying or selling shares through a brokerage platform. Some brokers waive these fees for certain account types, but it is prudent to check the fee schedule before committing capital.

Comparative Analysis with Peer Funds

When placed side‑by‑side with similar offerings, the t Rowe Price Retirement 2015 Fund shows both strengths and trade‑offs. Vanguard’s Target Retirement 2015 Fund, for example, boasts a lower expense ratio of 0.12 % but follows a more index‑based approach, offering less active management flexibility. Conversely, the Vanguard Target Retirement 2035 Trust II – In‑Depth Analysis highlights how a later‑dated fund can maintain a higher growth tilt, which may appeal to investors with a longer time horizon.

Another point of comparison is the State Street Target Retirement 2030 Fund, which emphasizes a slightly higher allocation to international bonds. Such differences can affect both risk exposure and return potential, making it essential for investors to align fund characteristics with personal risk tolerance and retirement timelines.

Who Should Consider the t Rowe Price Retirement 2015 Fund?

The t Rowe Price Retirement 2015 Fund is best suited for investors who are approaching retirement and desire a managed solution that automatically shifts toward preservation of capital. Individuals who prefer an actively managed portfolio, with professional oversight of both equity and fixed‑income components, will find value in the fund’s strategic rebalancing.

Small business owners, for instance, often seek a straightforward retirement vehicle for themselves and their employees. The Retirement Plans for Small Business Owners: A Comprehensive Guide outlines how target‑date funds can simplify plan administration while providing diversified exposure.

Conversely, investors with a higher tolerance for market risk and a desire for lower costs may opt for a purely index‑based fund. The decision ultimately hinges on the balance between cost, active management, and the investor’s comfort with the fund’s glide path.

Key Takeaways and Practical Tips

- Understand the glide path: The t Rowe Price Retirement 2015 Fund gradually reduces equity exposure, aiming for stability as retirement nears.

- Monitor fees: At 0.71 % expense ratio, the fund is competitive within its category but higher than passive alternatives.

- Assess risk tolerance: The fund’s diversified approach mitigates volatility, but investors should still evaluate whether the allocation matches their personal risk profile.

- Compare with peers: Reviewing similar funds, such as Vanguard and State Street target‑date options, helps determine the best fit for your retirement plan.

- Stay informed: Periodic re‑evaluation of the fund’s performance and alignment with your retirement timeline ensures the investment remains appropriate.

In summary, the t Rowe Price Retirement 2015 Fund offers a well‑structured, actively managed solution for investors nearing retirement. Its glide path, diversified holdings, and risk‑management practices provide a balanced approach to preserving accumulated wealth while still seeking modest growth. While fees are modestly higher than passive alternatives, the added professional oversight can be worthwhile for those who value a hands‑off, yet actively guided, retirement strategy. As with any investment, ongoing review and alignment with personal financial goals are essential to ensure the fund continues to serve its intended purpose.