Table of Contents

- Retirement Plans for Small Business Owners: Core Options Explained

- SEP IRA – Simplicity Meets Flexibility

- Solo 401(k) – High Limits for the Self‑Employed

- SIMPLE IRA – A Cost‑Effective Choice for Small Teams

- Choosing the Right Plan: Factors to Consider

- Business Size and Growth Trajectory

- Cash‑Flow Volatility

- Administrative Capacity

- Employee Recruitment and Retention

- Tax Planning Objectives

- Implementation Steps: From Idea to Execution

- 1. Assess Eligibility and Objectives

- 2. Compare Plan Providers

- 3. Consult a Professional

- 4. Complete the Required Paperwork

- 5. Educate Your Team

- 6. Set Up Payroll Integration

- 7. Review Annually

- Common Pitfalls and How to Avoid Them

- Neglecting Contribution Deadlines

- Overlooking Non‑Discrimination Tests

- Underestimating Administrative Costs

- Failing to Communicate Benefits

- Future Trends: What’s Next for Small‑Business Retirement Planning?

Running a small business often means wearing many hats—owner, manager, marketer, and sometimes even accountant. While the daily grind focuses on cash flow, client acquisition, and employee satisfaction, a crucial piece of the puzzle can be overlooked: the founder’s own retirement security. Unlike large corporations that automatically enroll workers in 401(k) plans, small‑business owners must actively select and fund a retirement vehicle that fits their unique cash‑flow patterns, tax situation, and long‑term goals.

Choosing the right retirement plan not only safeguards personal financial freedom but also creates a compelling benefit for attracting and retaining talent. When employees see that the owner cares about future security, morale and loyalty often rise. Moreover, many retirement options provide tax deductions that can lower the business’s taxable income, creating a win‑win scenario for both the company and its staff.

In the following sections we will explore the most common and effective retirement plans for small business owners, compare their features, and provide actionable steps to get started. The discussion will also highlight when it makes sense to involve a professional, such as a Chartered Retirement Planning Counselor, and how third‑party administrators can simplify plan management.

Retirement Plans for Small Business Owners: Core Options Explained

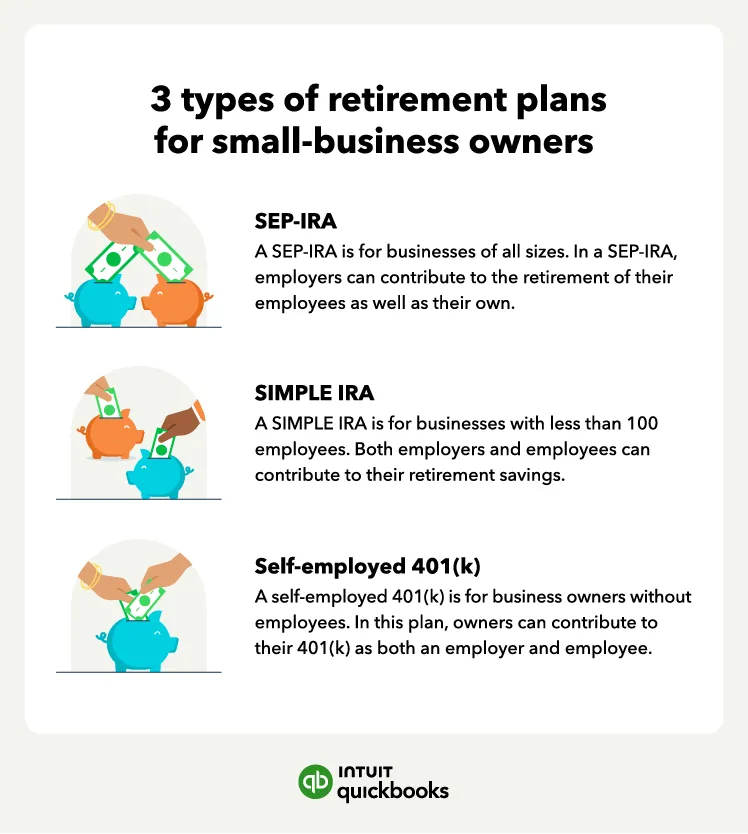

Small business owners typically consider three primary vehicles: the Simplified Employee Pension (SEP) IRA, the Solo 401(k) (also known as an Individual 401(k)), and the Savings Incentive Match Plan for Employees (SIMPLE) IRA. Each plan differs in contribution limits, eligibility, administrative burden, and suitability for businesses with or without employees.

SEP IRA – Simplicity Meets Flexibility

A SEP IRA allows the employer to contribute up to 25% of each eligible employee’s compensation, capped at $66,000 for 2023. For a solo owner with no employees, the contribution can be up to 25% of net earnings from self‑employment, making it a powerful tool for accelerating retirement savings while reducing taxable income.

- Eligibility: Any employee who is at least 21 years old, has worked for the business for three of the previous five years, and earned at least $750 in the year.

- Contribution Deadline: Contributions can be made up until the tax filing deadline, including extensions, giving owners extra time to assess cash flow.

- Administration: Minimal paperwork; the plan is established with a simple IRS Form 5305‑SEP.

Because the SEP IRA is easy to set up, many owners start here before expanding to more complex plans. However, the inability for employees to make salary‑deferral contributions can be a drawback when trying to attract talent.

Solo 401(k) – High Limits for the Self‑Employed

The Solo 401(k) is designed for business owners with no full‑time employees (apart from a spouse). It combines employee salary‑deferral contributions (up to $22,500 for 2023, or $30,000 if age 50 or older) with employer profit‑sharing contributions (up to 25% of compensation), allowing total contributions that can exceed $66,000.

- Dual Contribution Structure: Owners can contribute both as employee and employer, maximizing tax‑deferred growth.

- Roth Option: Many Solo 401(k) plans offer a Roth component, enabling after‑tax contributions that grow tax‑free.

- Loan Feature: Some plans permit borrowing up to 50% of the account balance, providing a source of liquidity without a taxable event.

When a business begins to hire a few part‑time staff, the Solo 401(k) can be converted to a traditional 401(k) with broader coverage, but that transition adds complexity and cost.

SIMPLE IRA – A Cost‑Effective Choice for Small Teams

The SIMPLE IRA is tailored for businesses with 100 or fewer employees. It requires either a matching contribution of up to 3% of compensation or a nonelective contribution of 2% for all eligible employees, regardless of whether they contribute themselves.

- Contribution Limits: Employees can defer up to $15,500 for 2023, with an additional $3,500 catch‑up contribution for those 50 or older.

- Employer Obligations: Mandatory contributions make the plan more attractive to staff, but they also increase the owner’s cash‑outflow.

- Administrative Simplicity: Compared with a traditional 401(k), the SIMPLE IRA has lower setup and filing costs.

For owners who want to offer a retirement benefit without the high administrative overhead of a full 401(k), the SIMPLE IRA strikes a practical balance.

Choosing the Right Plan: Factors to Consider

Deciding which retirement plan for small business owners best fits your situation involves evaluating several key dimensions:

Business Size and Growth Trajectory

If your company currently has only you and perhaps a spouse, the Solo 401(k) often provides the highest contribution ceiling. As you add full‑time staff, a SIMPLE IRA or a traditional 401(k) may become more appropriate to meet employee expectations.

Cash‑Flow Volatility

Businesses with irregular income streams may favor the SEP IRA because contributions are flexible and can be adjusted each year. Conversely, if earnings are stable, a plan with fixed employer contributions, like the SIMPLE IRA, can be budgeted more predictably.

Administrative Capacity

While all three plans require some record‑keeping, the SEP IRA has the least paperwork. The Solo 401(k) and SIMPLE IRA involve annual filing (Form 5500‑e) once assets exceed $250,000. For owners who prefer to outsource these tasks, partnering with a third‑party administrator can streamline compliance.

Employee Recruitment and Retention

Offering a retirement plan can be a differentiator in a competitive labor market. Employees often value employer matching contributions, making the SIMPLE IRA an attractive option despite the higher cost to the owner.

Tax Planning Objectives

Both SEP IRAs and Solo 401(k)s allow substantial pre‑tax contributions that lower the business’s taxable income. If the goal is aggressive tax reduction, the higher limits of a Solo 401(k) may be preferable. However, the Roth component in a Solo 401(k) or a Roth IRA can also provide tax‑free withdrawals in retirement, adding diversification.

Implementation Steps: From Idea to Execution

Turning the concept of retirement plans for small business owners into a functional program involves several concrete actions. Below is a roadmap that any owner can follow.

1. Assess Eligibility and Objectives

Start by listing all current employees, their ages, compensation, and projected hiring plans. Define your retirement savings goals—whether they focus on maximizing personal contributions, providing employee benefits, or both.

2. Compare Plan Providers

Financial institutions differ in fees, investment choices, and customer service. Look for providers that offer low‑cost index funds, automatic rebalancing, and user‑friendly dashboards. Some platforms also provide educational resources, which can be valuable for employees unfamiliar with retirement investing.

3. Consult a Professional

Complex tax implications and compliance rules make it wise to seek expert advice. A Chartered Retirement Planning Counselor can help you model different contribution scenarios, evaluate the impact on cash flow, and ensure that the chosen plan meets IRS requirements.

4. Complete the Required Paperwork

Each plan has a specific IRS form—Form 5305‑SEP for SEP IRA, adoption agreement for Solo 401(k), and Form 5304‑SIMPLE for SIMPLE IRA. Many providers allow electronic submission, speeding up the onboarding process.

5. Educate Your Team

Hold a brief meeting or webinar explaining the benefits of the new plan, how to enroll, and the importance of regular contributions. Providing a simple guide or linking to resources like the Vanguard Target Retirement 2035 Trust II – In‑Depth Analysis can demystify investment concepts for employees.

6. Set Up Payroll Integration

Integrate the retirement plan with your payroll software to automate salary‑deferral contributions and employer matching. Automation reduces errors and ensures timely deposits, which is essential for maintaining compliance.

7. Review Annually

Business circumstances change, and so do IRS contribution limits. Conduct an annual review to adjust contribution levels, add or remove employees, and evaluate whether a different retirement plan for small business owners might better serve your evolving needs.

Common Pitfalls and How to Avoid Them

Even with a solid plan in place, small business owners can stumble over a few frequent challenges.

Neglecting Contribution Deadlines

Missing the tax‑year deadline can forfeit valuable tax deductions. Set calendar reminders well before the filing date, especially if you use an extension.

Overlooking Non‑Discrimination Tests

Traditional 401(k) plans must pass annual ADP/ACP tests to ensure that contributions for highly compensated employees (often the owners) are not disproportionately high compared to non‑highly compensated staff. Failure can lead to corrective distributions or penalties.

Underestimating Administrative Costs

While a SEP IRA is cheap to maintain, a Solo 401(k) or SIMPLE IRA may involve annual filing fees, record‑keeping expenses, and possible third‑party administrator charges. Include these costs in your budgeting process.

Failing to Communicate Benefits

Employees who don’t understand the value of the retirement plan may not participate, reducing the overall effectiveness of the benefit. Ongoing education, transparent communication, and easy enrollment are critical.

Future Trends: What’s Next for Small‑Business Retirement Planning?

Technology continues to reshape how retirement plans are administered. Digital platforms now offer real‑time dashboards, AI‑driven investment advice, and seamless integration with payroll systems. As these tools become more affordable, even the smallest firms can provide sophisticated retirement solutions without hiring a full‑time benefits manager.

Additionally, legislative proposals aimed at expanding retirement access—such as the Secure 2.0 Act—may introduce new tax credits for small employers that set up retirement plans. Keeping abreast of policy changes can help owners capitalize on emerging incentives.

Finally, the rise of ESG (environmental, social, and governance) investing is influencing employee preferences. Offering ESG‑focused fund options within a Solo 401(k) or SIMPLE IRA can attract younger talent who prioritize responsible investing.

In summary, selecting the appropriate retirement plan for small business owners involves balancing personal savings goals, employee benefits, tax considerations, and administrative capacity. By methodically evaluating options, seeking professional guidance when needed, and leveraging modern fintech solutions, owners can build a retirement framework that supports both their future security and the growth of their enterprise.