Table of Contents

- State Street Target Retirement 2030 Fund: Core Features and Investment Approach

- State Street Target Retirement 2030 Fund Asset Allocation Over Time

- Performance History and Risk Considerations

- Cost Structure and Fees

- How the State Street Target Retirement 2030 Fund Fits Into a Retirement Plan

- Comparing State Street with Other Target‑Date Providers

- Tax Implications and Distribution Rules

- Practical Steps to Invest in the State Street Target Retirement 2030 Fund

Investors approaching retirement often search for a single‑fund solution that simplifies portfolio management while aligning with a specific retirement horizon. The State Street Target Retirement 2030 Fund is designed to meet that need, offering a glide‑path that gradually shifts from growth‑oriented assets to more conservative holdings as 2030 approaches. Understanding how this fund operates, its underlying assets, and its risk profile is essential for anyone considering it as a core component of a retirement plan.

This article provides a detailed examination of the State Street Target Retirement 2030 Fund, covering its investment philosophy, asset allocation methodology, cost structure, and performance history. By the end, readers will have a clear picture of whether the fund matches their retirement objectives and risk tolerance.

We will also compare the State Street offering with similar target‑date products from other providers, such as Vanguard and Fisher Investments, to highlight key differentiators. Throughout the discussion, relevant internal resources are referenced to help broaden your understanding of retirement planning.

State Street Target Retirement 2030 Fund: Core Features and Investment Approach

The State Street Target Retirement 2030 Fund is a mutual fund that follows a target‑date strategy, automatically rebalancing its asset mix over time. The fund’s primary objective is to provide long‑term capital growth and preservation of wealth for investors who plan to retire around the year 2030. To achieve this, the fund employs a “glide‑path” – a predetermined schedule that reduces exposure to equities and increases allocation to fixed‑income and cash equivalents as the target date nears.

Key components of the fund’s structure include:

- Dynamic asset allocation: The fund starts with a higher proportion of stocks (approximately 80%) and gradually shifts to a more balanced mix (around 40% stocks) by 2030.

- Diversified holdings: It invests across multiple regions, sectors, and market capitalizations to mitigate concentration risk.

- Professional management: State Street’s Global Equity and Fixed Income teams oversee the selection and monitoring of underlying securities.

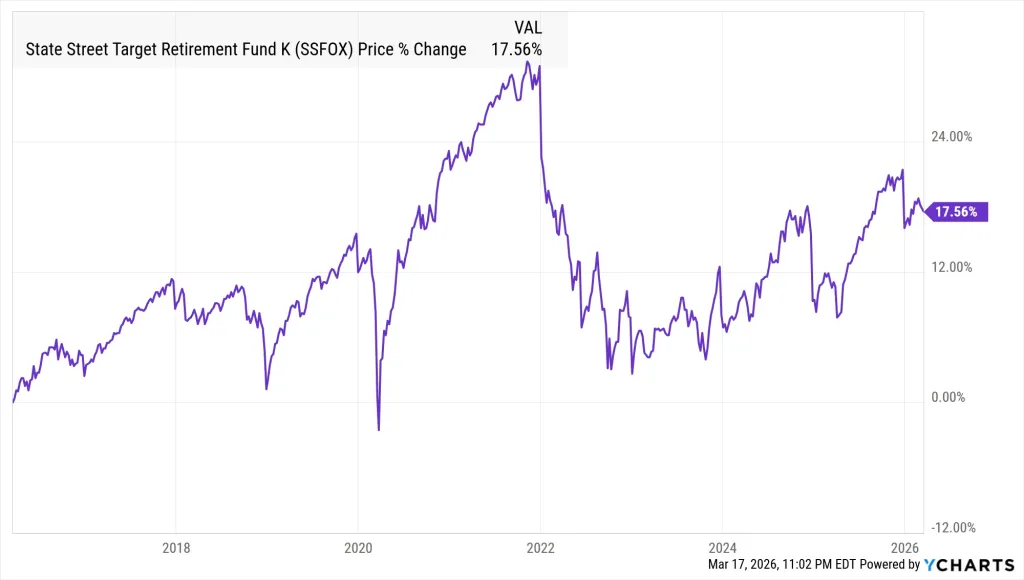

State Street Target Retirement 2030 Fund Asset Allocation Over Time

The glide‑path is the cornerstone of the State Street Target Retirement 2030 Fund’s strategy. Below is a simplified illustration of the asset allocation at three pivotal points:

- 2024 (Early Stage): 80% equities, 15% fixed income, 5% cash.

- 2027 (Mid‑Lifecycle): 60% equities, 30% fixed income, 10% cash.

- 2030 (Target Year): 40% equities, 50% fixed income, 10% cash.

This transition aims to preserve accumulated wealth while still providing growth potential. Investors benefit from reduced need to manually rebalance, as the fund automatically adjusts its composition in line with the predetermined schedule.

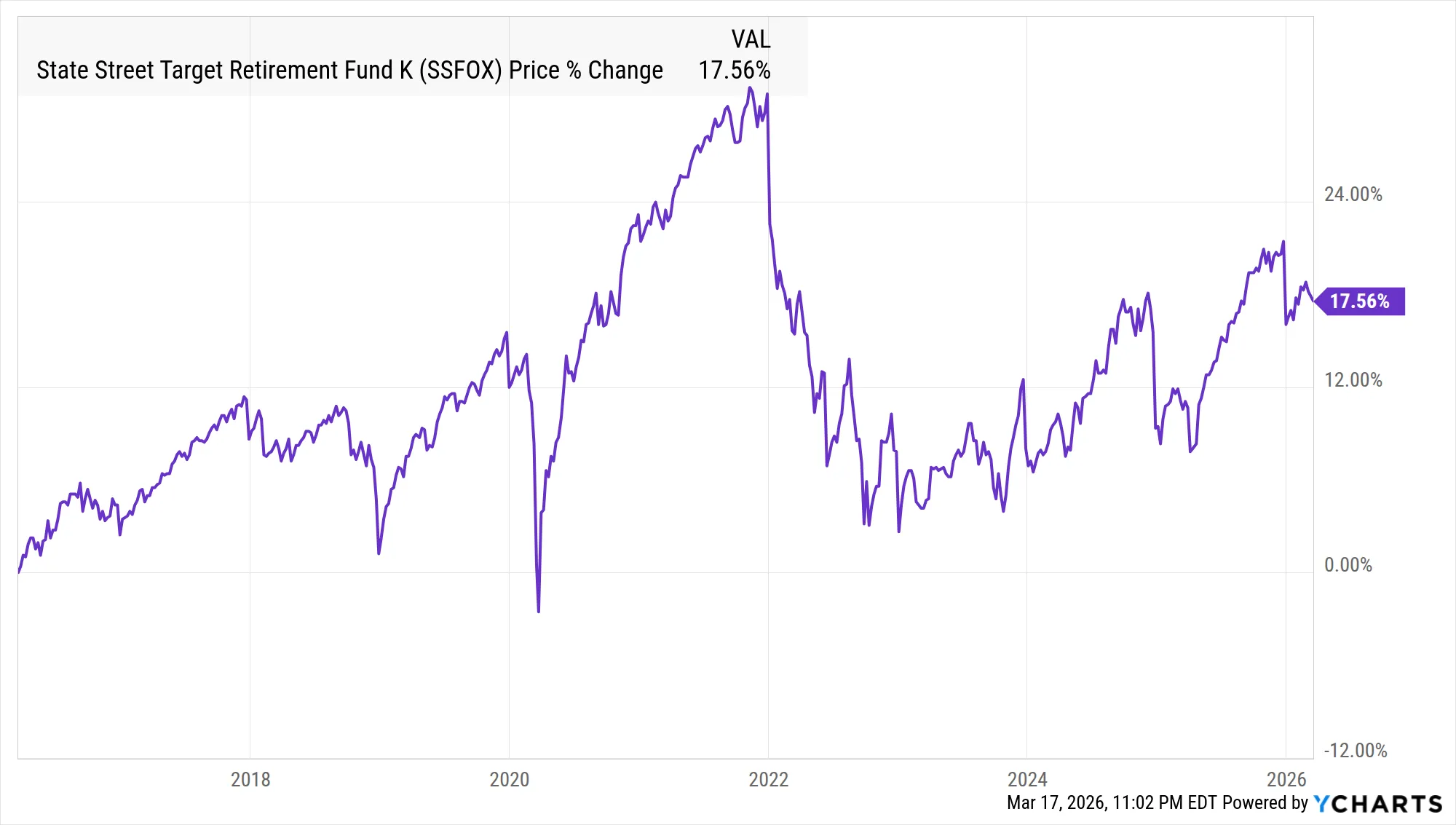

Performance History and Risk Considerations

Since its inception, the State Street Target Retirement 2030 Fund has delivered returns that closely track its benchmark indices, reflecting the fund’s commitment to a disciplined asset allocation. While past performance does not guarantee future results, examining historical data helps assess the fund’s consistency and volatility.

During market upturns, the fund’s equity exposure contributed to solid gains, whereas during downturns, the increasing fixed‑income component helped cushion losses. This balance is essential for investors seeking a smoother ride toward retirement.

Risk factors to consider include:

- Market risk: Equity holdings remain susceptible to market fluctuations, especially in the early years.

- Interest‑rate risk: Fixed‑income securities can lose value if rates rise sharply.

- Liquidity risk: While the fund holds primarily liquid assets, certain niche securities may be harder to trade.

Investors should evaluate these risks in relation to their personal financial situation and overall retirement strategy.

Cost Structure and Fees

Expense ratios are a critical component of any long‑term investment. The State Street Target Retirement 2030 Fund maintains a competitive expense ratio, typically ranging between 0.20% and 0.35% of assets under management. This includes management fees, administrative costs, and other operational expenses.

Compared with similar offerings—such as the Vanguard Target Retirement 2025 Trust Select, which often carries a slightly lower expense ratio—the State Street fund’s fees are justified by its robust research capabilities and active management approach. For a comprehensive comparison of target‑date fund fees, see our guide on Vanguard Target Retirement 2025 Trust Select – Comprehensive Overview.

How the State Street Target Retirement 2030 Fund Fits Into a Retirement Plan

When constructing a retirement portfolio, diversification across different asset classes and providers can enhance resilience. The State Street Target Retirement 2030 Fund can serve as a core holding within a broader retirement strategy, especially for investors who prefer a “set‑and‑forget” approach.

Here are some practical ways to incorporate the fund:

- Primary retirement account: Use the fund as the main investment in an employer‑sponsored 401(k) or an individual retirement account (IRA).

- Supplemental savings: Pair the fund with a taxable brokerage account that holds complementary assets, such as real estate investment trusts (REITs) or alternative investments.

- Legacy planning: The fund’s gradual shift to lower‑risk assets can help preserve wealth for beneficiaries.

For those who need to understand how third‑party administrators support retirement plans, our article Third Party Administrators for Retirement Plan – Complete Guide provides valuable insights.

Comparing State Street with Other Target‑Date Providers

While the State Street Target Retirement 2030 Fund offers a solid blend of active management and diversified exposure, it’s beneficial to benchmark it against peers. Below is a brief comparison with two notable alternatives:

- Vanguard Target Retirement 2025 Trust Select: Known for its low-cost index‑based approach, Vanguard’s fund typically has a lower expense ratio but less active security selection.

- Fisher Investments 7 Retirement Income Strategies: Fisher focuses on tailored income generation, often employing higher equity exposure even near retirement, which may result in higher volatility.

Investors should weigh factors such as fee structure, management style, and historical performance when choosing the most suitable fund. A deeper look at Fisher Investments’ methodology can be found in Fisher Investments 7 Retirement Income Strategies – A Comprehensive Guide.

Tax Implications and Distribution Rules

Target‑date funds, including the State Street Target Retirement 2030 Fund, are subject to the same tax rules as other mutual funds. Distributions may include qualified dividends, ordinary income, and capital gains, each taxed at different rates. Holding the fund within a tax‑advantaged account (e.g., 401(k) or IRA) can defer or eliminate taxes on earnings until withdrawal.

It’s also important to understand required minimum distributions (RMDs) that begin at age 73 under current law. For a detailed discussion on how the IRS may affect retirement assets, refer to Can the IRS Take Your Retirement Money? A Detailed Look.

Practical Steps to Invest in the State Street Target Retirement 2030 Fund

Getting started with the State Street Target Retirement 2030 Fund involves a few straightforward actions:

- Confirm that your brokerage or retirement plan offers the fund under its ticker symbol.

- Review the fund’s prospectus to understand its investment objectives, risks, and fees.

- Determine the appropriate allocation based on your overall retirement plan and other holdings.

- Set up automatic contributions to maintain consistent investment over time.

- Monitor the fund’s performance periodically, but avoid frequent trading that may disrupt the glide‑path.

By following these steps, investors can seamlessly integrate the State Street Target Retirement 2030 Fund into their retirement roadmap.

In summary, the State Street Target Retirement 2030 Fund provides a disciplined, professionally managed path toward retirement, balancing growth and preservation through a systematic glide‑path. Its moderate expense ratio, diversified asset base, and automatic rebalancing make it a compelling choice for investors targeting a 2030 retirement horizon. As with any investment decision, individuals should assess their personal financial goals, risk tolerance, and the broader composition of their retirement portfolio before committing.