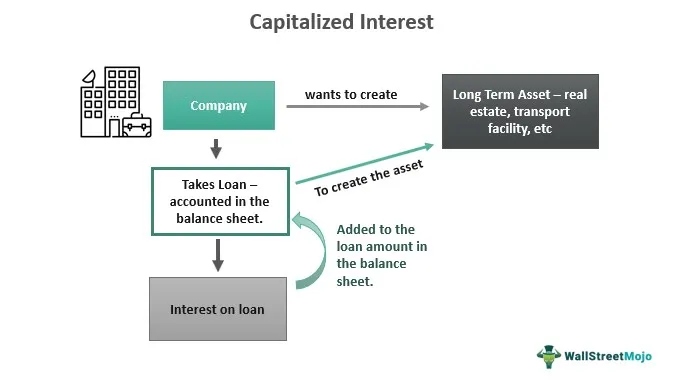

When you borrow money to fund higher education, the terms of that loan can sometimes feel as complex as the subjects you study. One concept that often trips borrowers up is capitalized interest. While the phrase sounds technical, its core idea is straightforward: interest that is added to the principal balance of a loan rather than being paid off immediately.

Understanding what is capitalized interest student loan helps you see why your balance can grow even when you’re not actively making payments. This knowledge becomes especially important during periods like school, grace periods, or deferment, when regular payments are paused. By the end of this article, you’ll have a clear picture of how capitalized interest works, its tax implications, and practical steps you can take to keep it under control.

Before diving into the mechanics, it’s worth noting that capitalized interest is not a penalty or a hidden fee. It is simply a method of accounting for unpaid interest that accrues over time. The way it is handled can affect the total amount you owe, the length of your repayment term, and even the amount of interest you can deduct on your tax return.

What is Capitalized Interest Student Loan?

In the context of student loans, what is capitalized interest student loan refers to the practice of adding accrued interest to the original loan principal. This usually happens at specific points in the loan lifecycle—most commonly at the end of a grace period, during deferment, or when a borrower consolidates multiple loans into a single new loan.

When interest is capitalized, the balance you owe increases because the unpaid interest becomes part of the principal. From that moment forward, future interest calculations are based on this higher principal amount, which can cause the total cost of the loan to rise significantly over time.

What is Capitalized Interest Student Loan and How It Works

The process begins the moment you take out a loan. While you are in school, many federal loans (such as Direct Subsidized Loans) do not accrue interest, but unsubsidized loans do. If you have an unsubsidized loan, interest starts accumulating from the day the funds are disbursed. During school, the grace period, or any deferment, you typically are not required to pay this interest. Instead, the interest accrues and is recorded separately.

At the end of the deferment or grace period, the lender will add (or “capitalize”) the accrued interest to the principal balance. For example, if you borrowed $10,000 and $500 of interest accrued during school, after capitalization your new principal becomes $10,500. From that point, each monthly payment will include interest on $10,500, not the original $10,000.

Capitalization also occurs when you choose to consolidate several loans into a single consolidation loan. The new loan’s balance will include the sum of the original principals plus any accrued interest that had not yet been paid.

Why Capitalized Interest Happens

There are several reasons lenders capitalize interest:

- Administrative Simplicity: Adding accrued interest to the principal simplifies accounting for both the lender and the borrower.

- Regulatory Requirements: Certain federal loan programs mandate capitalization at specific milestones, such as the end of the six-month grace period for Direct Loans.

- Borrower Choice: In some cases, borrowers voluntarily allow interest to capitalize, often when they refinance or consolidate to obtain a lower interest rate.

Understanding why it occurs can help you anticipate when your balance might jump and plan accordingly. For instance, if you know your loan will capitalize interest after graduation, you might start making small interest payments while still in school to keep the amount low.

Impact on Repayment and Total Cost

Capitalized interest directly influences three key aspects of a student loan:

- Monthly Payments: A higher principal means larger monthly payments, assuming the repayment term remains unchanged.

- Repayment Term: If you keep the same monthly payment after capitalization, the loan term will extend, prolonging the time you carry debt.

- Total Interest Paid: Since interest compounds on a larger base, you will ultimately pay more interest over the life of the loan.

Consider two scenarios for a $20,000 unsubsidized loan at a 5% interest rate:

- Scenario A – No Capitalization: You begin making interest payments while in school, keeping the principal at $20,000. Over a 10‑year term, total interest paid is roughly $5,300.

- Scenario B – Capitalization After 4 Years: No interest is paid during school; $4,000 of interest capitalizes, raising the principal to $24,000. Over the same 10‑year term, total interest rises to about $7,800.

The difference—over $2,500—highlights why many borrowers aim to prevent or minimize capitalization wherever possible.

Tax Implications of Capitalized Interest

Interest on qualified student loans is generally tax‑deductible up to $2,500 per year, provided you meet income requirements. However, capitalized interest is treated differently:

- If the interest is capitalized at the time the loan is originated (as with most federal loans), it remains deductible.

- When interest is capitalized later—such as during consolidation—it may not be deductible for that tax year because it is considered part of the new principal.

For detailed guidance on income limits and deduction rules, see the article Income Limit Student Loan Interest Deduction – What You Need to Know. Understanding these nuances can help you maximize tax benefits while managing your loan balance.

Strategies to Manage or Avoid Capitalized Interest

While you cannot always prevent capitalization—especially when required by law—there are proactive steps you can take to limit its impact:

Pay Interest While in School

If your loan accrues interest during school, making even modest interest‑only payments can keep the principal from growing. Many borrowers set up automatic monthly transfers to cover accrued interest, effectively preventing the balance from ballooning at graduation.

Consider Early Repayment Before Capitalization

Before the end of a grace period or deferment, you may choose to pay off the accrued interest in a lump sum. This reduces the amount that will be added to the principal, keeping future interest calculations lower.

Explore Consolidation Wisely

Consolidating loans can simplify repayment, but it also triggers capitalization of any unpaid interest. If you decide to consolidate, aim to do so after you have paid down as much accrued interest as possible. For a step‑by‑step guide on how consolidation works, read Student Loan Consolidation for Private Loans – A Complete Guide.

Refinance to Lower Rates

Refinancing with a private lender may offer a lower interest rate, which can offset the effect of capitalized interest. However, refinancing federal loans means losing certain protections, such as income‑driven repayment plans. If you’re considering this route, the article Refinance Student Loans Lower Interest Rate – A Comprehensive Guide provides a thorough overview.

Stay Informed About Grace Periods

Each loan type has its own grace period rules. For example, Direct Subsidized Loans offer a six‑month grace period after graduation, during which no interest accrues. Unsubsidized loans, however, continue to accrue interest throughout this period. Knowing the specifics helps you plan payments strategically.

Common Misconceptions About Capitalized Interest

Many borrowers hold mistaken beliefs that can lead to costly errors:

- “Capitalized interest is a hidden fee.” In reality, it is simply interest that has not yet been paid. The lender is transparent about when and how it will be capitalized.

- “Paying extra will not affect the capitalized amount.” Extra payments that go toward interest before capitalization can reduce the amount added to principal.

- “Consolidation always saves money.” While consolidation can lower monthly payments, it may increase total interest paid if large amounts of accrued interest are capitalized.

Clearing up these myths enables you to make better-informed decisions throughout your loan journey.

Real‑World Example: From Campus to Repayment

Imagine Maya, a recent graduate with two federal loans:

- $8,000 unsubsidized loan at 4.5% interest.

- $12,000 subsidized loan at 4.5% interest.

During her four years of study, the unsubsidized loan accrued $1,620 in interest, while the subsidized loan accrued none. Maya chose not to make any payments while in school. At graduation, the $1,620 of interest on the unsubsidized loan was capitalized, raising that loan’s principal to $9,620.

If Maya had paid $50 per month toward interest while in school, she would have reduced the accrued interest to $620, resulting in a lower principal after capitalization. Over a standard 10‑year repayment schedule, that $1,000 difference translates to roughly $300 less paid in total interest.

This example underscores the tangible benefits of addressing interest early, even in small increments.

When Capitalized Interest Becomes Part of the Tax Deduction

The IRS permits a deduction for interest paid on qualified student loans, but the timing matters. If interest is capitalized at the moment a loan is originated, the borrower can still deduct that interest in the year it is paid. However, when interest is capitalized later—such as during consolidation—it is treated as part of the new loan balance, and the borrower cannot claim it as a deduction for that tax year.

To maximize deductions, keep detailed records of when interest is capitalized and how much is added to the principal. Consulting a tax professional or reviewing the IRS Publication 970 can provide additional clarity.

Final Thoughts on Managing Capitalized Interest

Grasping what is capitalized interest student loan is essential for any borrower who wants to keep their debt manageable. By recognizing the moments when interest will be added to the principal, you can plan payments that mitigate its impact, choose consolidation or refinancing options wisely, and stay aware of tax implications.

Remember that the key to minimizing the cost of capitalized interest lies in early and consistent interest payments, strategic use of consolidation, and staying informed about the terms of each loan. Armed with this knowledge, you can navigate the repayment landscape with confidence, ensuring that the growth of your loan balance stays under control and that you remain on track to achieve your financial goals.