Citibank add joint account holder is a process that many families, couples, and business partners consider when they want shared access to a single banking relationship. Whether you are looking to combine finances, simplify bill payments, or provide a trusted person with emergency access, Citibank offers a structured method to include an additional name on an existing account. This article walks you through everything you need to know, from eligibility requirements to the exact steps you’ll take at a branch or online, and highlights the practical advantages of joint ownership.

Understanding the mechanics behind joint accounts helps you avoid unexpected surprises—such as credit checks, liability issues, or documentation delays—that can turn a simple request into a time‑consuming ordeal. By following the guidance below, you’ll be able to add a joint holder efficiently, ensuring both parties enjoy equal rights and responsibilities from day one.

What Is a Joint Account and Why It Matters at Citibank

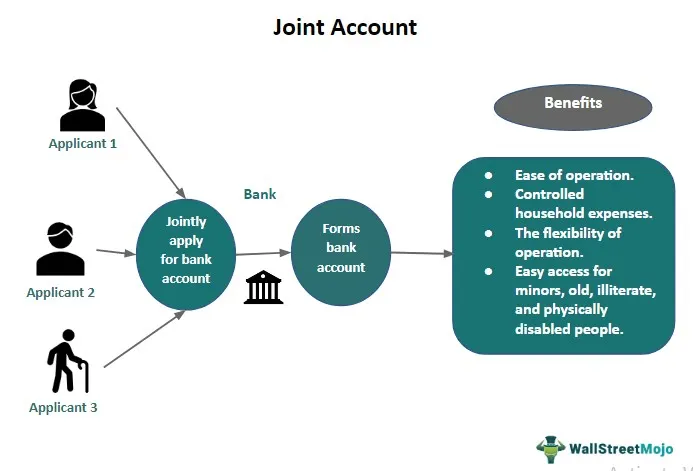

A joint account is a single banking relationship that lists two or more individuals as owners. In Citibank, joint accounts function under a “joint tenancy” model, meaning each holder has equal authority to deposit, withdraw, and manage the account. This structure is especially useful for couples sharing household expenses, parents managing a minor’s allowance, or business partners needing a unified financial hub.

Key Features of Citibank Joint Accounts

- Equal ownership: All parties can perform transactions without needing the other’s approval.

- Survivorship rights: If one holder passes away, the surviving holder typically retains full control, subject to state laws.

- Shared liability: Both holders are responsible for overdrafts, fees, and any negative activity.

- Convenient access: Each holder receives a separate debit card and online login credentials.

Eligibility Criteria and Required Documentation

Before you can add a joint account holder, Citibank verifies that both individuals meet specific criteria. The bank’s policies aim to protect existing customers and comply with federal regulations, such as the Know‑Your‑Customer (KYC) rules.

Basic Eligibility Requirements

- Both parties must be at least 18 years old (or the legal age of majority in your jurisdiction).

- Each individual must provide a valid government‑issued photo ID (e.g., passport, driver’s license).

- Social Security Number (SSN) or Tax Identification Number (TIN) for credit and tax reporting purposes.

- Proof of residence, such as a utility bill or lease agreement, dated within the last 90 days.

Additional Documents for Specific Situations

- If one holder is a minor, a parent or legal guardian must sign a custodial agreement.

- Non‑U.S. residents may need to present a foreign passport, visa, and a U.S. address.

- Business partners adding a corporate entity must submit the entity’s EIN and formation documents.

Having these documents ready speeds up the approval process and reduces the likelihood of a second visit to the branch. For a smoother experience, you might also want to review The Ultimate Guide to VPNs with No Logs and Strong Encryption – Stay Private & Secure to understand how online security tools can protect your personal data while you submit sensitive information electronically.

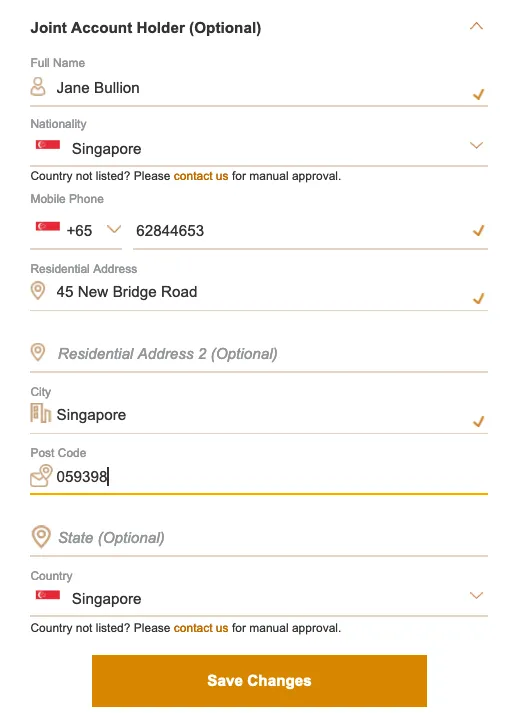

Step‑by‑Step Process to Add a Joint Account Holder

The actual addition of a joint holder can be completed either in person at a Citibank branch or through the bank’s secure online portal, depending on the account type and your region. Below is a detailed walkthrough for both methods.

Option 1: In‑Branch Procedure

- Schedule an appointment: Call your local Citibank branch or use the online scheduler to set a time. Walk‑in services are available but may involve longer wait times.

- Gather required documents: Bring the IDs, SSNs, and proof of address for both existing and prospective holders.

- Complete the Joint Account Addendum: A bank representative will provide a form titled “Joint Account Addendum” or similar. Both parties must sign this document.

- Submit a credit check authorization: Citibank runs a soft credit pull on the new holder to verify identity and assess risk. This does not affect the credit score.

- Review and sign the updated terms: The joint account agreement outlines each holder’s rights and responsibilities. Read it carefully before signing.

- Receive new debit cards and login credentials: Both holders will be issued fresh cards and online access details on the spot or via mail within a few days.

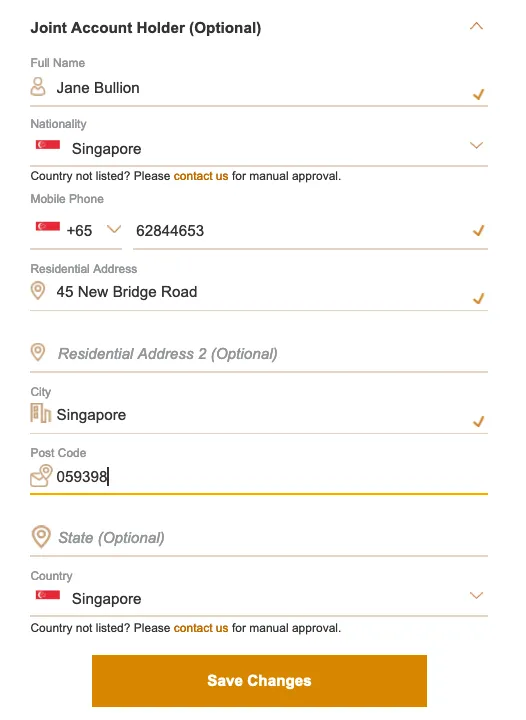

Option 2: Online Submission (Where Available)

- Log into Citibank Online: Use your existing username and password. Navigate to the “Account Services” section.

- Select “Add Joint Owner”: The system will prompt you to enter the prospective holder’s personal information.

- Upload scanned documents: Attach clear images of the required IDs and proof of address. The portal supports JPEG, PNG, and PDF formats.

- Electronic signature: Both parties must sign electronically using the bank’s secure e‑signature tool.

- Verification step: Citibank may request a brief video call to confirm identity, especially for high‑value accounts.

- Confirmation email: Once approved, you’ll receive an email outlining the next steps, including how to order additional debit cards.

Online addition can be quicker for tech‑savvy users, but keep in mind that certain account types (e.g., business checking) still require a physical signature. If you encounter any difficulty, the bank’s live chat support can provide real‑time assistance.

Common Issues and How to Resolve Them

Even with careful preparation, you might face obstacles during the joint holder addition process. Below are typical challenges and practical solutions.

Issue: Inconsistent Personal Information

Citibank cross‑checks names, addresses, and SSNs against federal databases. A mismatch (e.g., a typo in the SSN) can trigger a delay. Double‑check every entry before submission, and if an error is discovered after filing, contact the branch immediately to amend the record.

Issue: Credit Check Decline

If the prospective holder has a recent bankruptcy, significant delinquencies, or a fraud alert, the soft pull may flag the account. While a joint account does not require a hard credit inquiry, the bank may request additional documentation (e.g., a letter of explanation) before proceeding.

Issue: Limited Online Availability

Some regions still mandate an in‑person visit for joint account changes, especially for accounts linked to mortgages or investment portfolios. In such cases, schedule a branch appointment well in advance to avoid long wait times.

Issue: Duplicate Debit Cards

Citibank typically issues one card per holder. If you accidentally order multiple cards, you can cancel the extras through the online portal or by calling customer service. Unused cards should be destroyed securely.

Benefits of Adding a Joint Account Holder

Beyond convenience, joint accounts provide tangible financial and relational advantages.

Financial Management

- Shared budgeting: Both parties can see real‑time balances, making it easier to track household expenses.

- Emergency access: If one holder is unavailable due to illness or travel, the other can still manage the funds.

- Consolidated statements: One monthly statement reduces paperwork and simplifies tax preparation.

Relationship Building

- Transparency: Joint accounts foster open communication about spending habits.

- Trust: Sharing an account signals confidence and commitment, useful for couples and business partners.

- Estate planning: In many jurisdictions, joint tenancy with right of survivorship ensures that assets pass automatically to the surviving holder.

If you are managing a small business, you might also find the article How to Choose an Affordable VPN for Small Businesses Without Compromising Security useful for protecting your financial data while conducting joint transactions online.

Frequently Asked Questions (FAQs)

Can I add a joint holder to a savings account?

Yes. Citibank allows joint ownership for most savings products, though interest‑bearing accounts may have additional tax reporting requirements.

Will adding a joint holder affect my credit score?

The bank conducts a soft credit inquiry on the new holder, which does not impact credit scores. However, any negative activity (overdrafts, missed payments) on the joint account will affect both parties’ credit histories.

Can I remove a joint holder later?

Removing a holder requires the consent of all current owners. You’ll need to fill out a “Joint Account Removal Form” and provide identification for the remaining holder(s).

What happens if one holder passes away?

In most states, the surviving holder automatically assumes full ownership under the right‑of‑survivorship provision, but the estate may still need to file a death certificate with the bank.

Is there a fee for adding a joint holder?

Citibank generally does not charge a fee for adding a joint owner, but some account types (e.g., premium checking) may have associated service charges.

Adding a joint account holder at Citibank is a straightforward process when you come prepared with the right documents, understand the responsibilities involved, and follow the bank’s step‑by‑step instructions. Whether you pursue the in‑branch route or use the online portal, the key is clear communication with the other party and diligent record‑keeping. By doing so, you’ll enjoy the practical benefits of shared financial management while safeguarding both participants against potential liabilities.