Insurance can feel like a maze of contracts, clauses, and specialized terms. For many small business owners, landlords, or families with multiple assets, the challenge is not just finding coverage, but finding the right kind of coverage that simplifies administration while still providing solid protection. One solution that often goes unnoticed is a blanket policy. Understanding what is a blanket policy insurance and how it differs from traditional policies can save time, reduce paperwork, and sometimes lower overall costs.

Imagine a landlord who owns several rental properties scattered across a city. Instead of purchasing separate property insurance for each building, a blanket policy can cover all of them under a single contract. The same principle applies to businesses that own many pieces of equipment, vehicles, or even multiple locations. By consolidating risk under one umbrella, policyholders gain clarity and flexibility.

In this article we will walk through the definition, mechanics, and practical scenarios where a blanket policy shines. We’ll also compare it with named‑entity policies, highlight potential pitfalls, and give actionable tips for evaluating whether this approach fits your needs.

What is a Blanket Policy Insurance? Core Concepts Explained

A blanket policy is an insurance contract that provides coverage for a group of items, locations, or people without listing each one individually. Instead of naming each asset, the insurer sets a total limit that applies to the entire collection. This “blanket” of protection can be applied to property, liability, automobile fleets, or even professional liability.

The key characteristic that answers the question “what is a blanket policy insurance?” is its flexibility. The policy does not require the insured to submit a detailed inventory each time an item is added or removed, as long as the total exposure remains within the agreed limit. Adjustments are often made by simply notifying the insurer of changes, rather than drafting a new endorsement.

What is a Blanket Policy Insurance? Key Benefits for Businesses

- Simplified Administration: One contract, one renewal date, and one premium payment streamline bookkeeping.

- Cost Efficiency: Bundling multiple assets can result in lower per‑unit rates compared with separate policies.

- Flexibility: Adding new equipment or property usually requires only a brief endorsement, not a full policy rewrite.

- Broader Coverage: Some blanket policies automatically extend to temporary locations or short‑term rentals, reducing gaps in protection.

When to Choose a Blanket Policy Over Named‑Entity Coverage

While blanket policies are powerful, they are not universally the best choice. The decision hinges on the nature of the risk, the diversity of assets, and the administrative preferences of the insured.

Scenarios Ideal for Blanket Coverage

- Multiple Real Estate Holdings: Landlords with several rental units can protect all properties under a single policy, avoiding the need to manage dozens of individual contracts.

- Fleet Management: Companies that own a fleet of delivery trucks or service vehicles often find a blanket auto policy easier to manage than separate policies for each vehicle.

- Equipment‑Intensive Industries: Construction firms, manufacturers, and IT companies with ever‑changing inventories of tools and hardware benefit from the flexibility of blanket coverage.

- Professional Services: A law firm or accounting practice that adds new partners or staff may use a blanket professional liability policy to automatically include all members.

For a practical illustration, see how online home and auto insurance quotes can be compared across different coverage models, highlighting the ease of obtaining a single quote for multiple assets.

Situations Where Named‑Entity Policies May Be Preferable

- Highly Specialized Risks: Certain high‑value items (e.g., fine art, rare collectibles) often need tailored endorsements that a blanket policy cannot adequately address.

- Regulatory Requirements: Some jurisdictions mandate separate policies for specific types of liability, such as workers’ compensation.

- Precise Limit Management: When an organization wants to allocate distinct limits to each asset, named‑entity policies provide clearer control.

How a Blanket Policy Is Structured

Even though a blanket policy appears simple on the surface, it contains several components that determine how claims are paid and how limits are applied.

Aggregate Limit

The aggregate limit is the total amount the insurer will pay for all covered losses under the policy period. If the combined losses of all assets exceed this limit, the insured may need to absorb the excess.

Sub‑Limits and Deductibles

Many blanket policies include sub‑limits for particular categories of risk. For example, a commercial property blanket policy might set a $1 million aggregate limit but impose a $100,000 sub‑limit for equipment loss. Deductibles work similarly, applying either per‑claim or per‑policy.

Coverage Extensions

Blanket policies can be written to automatically extend coverage to temporary locations, contractors, or short‑term rentals. This is especially valuable for businesses that operate pop‑up stores or seasonal events.

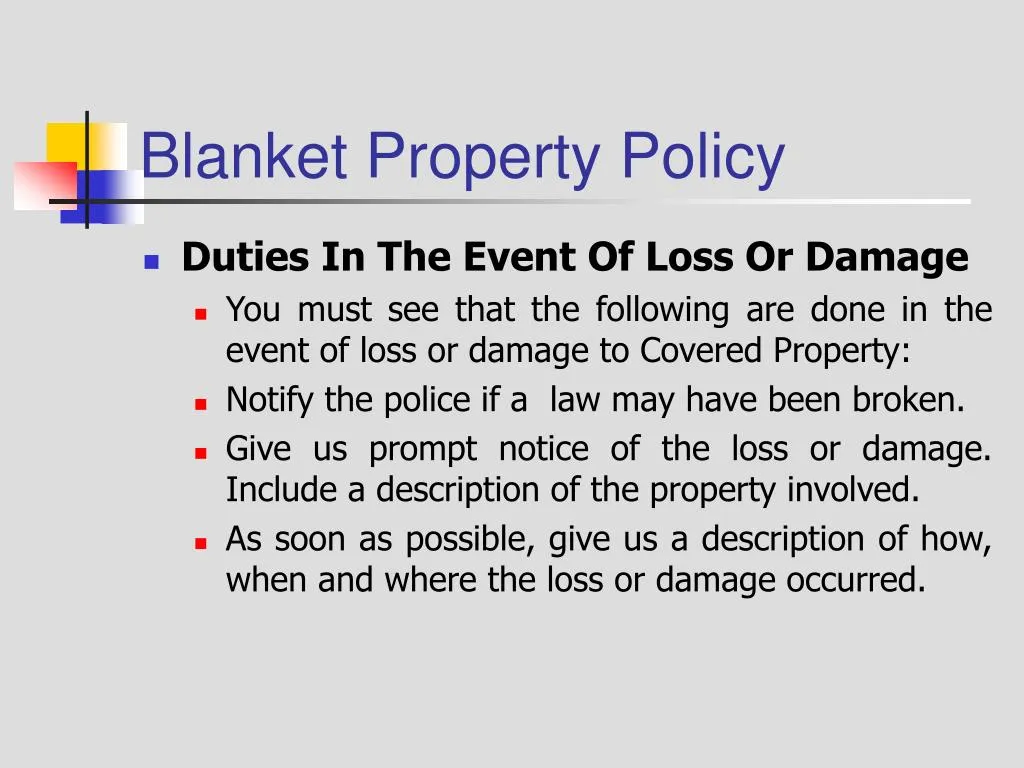

Claims Process Under a Blanket Policy

When a loss occurs, the insurer evaluates the claim against the aggregate limit and any applicable sub‑limits. The process mirrors that of a standard policy, but the key difference is that the insurer looks at the total exposure rather than a specific, named asset.

For instance, if a fire damages three warehouses covered under a blanket property policy, the insurer will total the losses across all three sites and compare the sum to the aggregate limit. If the combined loss is within the limit, the claim is paid in full; otherwise, the insured may receive a partial payment.

Documentation Tips for Claimants

- Maintain a master inventory that lists all assets covered under the blanket policy, even though individual items are not named in the contract.

- Document each loss with photographs, receipts, and police reports where applicable.

- Notify the insurer promptly, referencing the blanket policy number and the specific incident.

Cost Considerations and Premium Calculation

Premiums for blanket policies are calculated based on the total exposure, the aggregate limit, and the risk profile of the insured group. Insurers often apply a discount for bundling multiple assets because the overall risk is spread out, reducing the likelihood of large, single‑event losses.

However, it is essential to avoid over‑insuring. Setting an aggregate limit far above the realistic exposure can inflate premiums unnecessarily. Conversely, under‑insuring can leave gaps that become costly in the event of a large claim.

Comparing Quotes

When shopping for coverage, use tools that let you compare auto and home insurance quotes online side by side. This enables you to see how different carriers price blanket versus named‑entity policies, helping you make an informed decision.

Legal and Regulatory Aspects

Insurance regulation varies by state and country. Some jurisdictions have specific rules about how blanket policies must disclose coverage limits, sub‑limits, and exclusions. Always verify that the policy complies with local insurance codes and that the insurer is licensed to issue blanket coverage in your area.

Professional liability insurance for specialized fields, such as tax preparers, often includes blanket provisions. For a deeper dive, read the professional liability insurance for tax preparers – A Complete Guide, which illustrates how blanket clauses can simplify coverage for a practice with many employees.

Potential Pitfalls and How to Mitigate Them

While blanket policies offer convenience, they can also create hidden risks if not managed carefully.

Unclear Sub‑Limits

Because a blanket policy covers many items, sub‑limits may be overlooked. Always request a clear schedule of sub‑limits and confirm they align with the value of your assets.

Claims Overlap

If you hold separate policies for some assets, there is a chance of overlapping coverage, which could lead to disputes or reduced payouts. Conduct a policy audit to eliminate redundancy.

Changing Exposure

Rapid growth or acquisition of new assets can quickly outpace the original aggregate limit. Schedule regular reviews—at least annually—to adjust the limit as your exposure evolves.

Steps to Obtain a Blanket Policy

- Assess Your Total Exposure: Compile a comprehensive list of all assets, locations, or personnel you wish to cover.

- Determine Desired Coverage Limits: Choose an aggregate limit that reflects the combined value of your exposure.

- Contact Multiple Insurers: Request quotes for blanket coverage and compare terms, sub‑limits, and premiums.

- Review Policy Language: Pay special attention to exclusions, deductible structures, and any conditions for adding new items.

- Finalize and Implement: Sign the agreement, set up payment, and keep a master inventory for future reference.

For property owners, a related question often arises: does home insurance cover structural problems? The answer varies by policy, but a blanket property policy typically includes broader structural coverage, reducing the need for separate endorsements. See the article on home insurance structural coverage for more details.

In summary, a blanket policy is a versatile tool that can streamline insurance management for individuals and businesses with multiple assets. By understanding the mechanics, evaluating costs, and staying vigilant about limits and exclusions, policyholders can harness the convenience of a single contract without sacrificing adequate protection.