The US Bank Shield Visa card credit limit is a figure that can feel mysterious to many cardholders. From the moment the card arrives in the mailbox, the number printed on the back influences purchasing power, interest costs, and overall financial flexibility. Understanding how this limit is calculated, what variables the bank considers, and how you can responsibly influence it is essential for anyone who wants to use the card wisely.

This article walks you through the inner workings of the credit‑limit determination process, highlights the key factors that US Bank evaluates, and offers clear, actionable advice on how to maintain a healthy credit profile. By the end, you will have a solid grasp of the mechanisms behind the US Bank Shield Visa card credit limit and the steps you can take to optimize it without risking your credit score.

Whether you are a new cardholder eager to make the most of your Shield Visa or a seasoned user looking for ways to increase your limit, the information below will serve as a practical guide. The narrative follows a straightforward, factual style, avoiding hype while delivering depth and clarity.

Understanding the US Bank Shield Visa Card

The US Bank Shield Visa is positioned as a low‑interest, rewards‑focused credit card. It offers a straightforward rewards structure, no annual fee, and a competitive APR that appeals to both everyday shoppers and travelers. The card’s design emphasizes simplicity, but the credit limit—often the most critical feature—carries nuances that deserve careful examination.

Key Features of the Shield Visa

- Variable APR ranging from 14.99% to 24.99% depending on creditworthiness.

- Cash back rewards on groceries, gas, and dining.

- No foreign transaction fees, making it suitable for international use.

- Built‑in security tools such as fraud alerts and zero‑liability protection.

Why Credit Limit Matters

The credit limit determines the maximum amount you can borrow on the card at any given time. It directly affects your credit utilization ratio, a major component of the FICO scoring model. A higher limit, when used responsibly, can improve your credit score, while a low limit that is maxed out can have the opposite effect.

How US Bank Determines Your Credit Limit

US Bank employs a multifaceted algorithm to set the credit limit for each Shield Visa applicant. The process is not based on a single data point but rather a blend of quantitative metrics and qualitative assessments. Below is a breakdown of the primary components that influence the final number.

1. Credit Score and History

Credit scores remain the cornerstone of any credit‑limit decision. US Bank typically looks at FICO scores ranging from 670 (good) to 800+ (excellent). Applicants with higher scores generally receive higher limits because they have demonstrated a pattern of timely payments and low default risk.

2. Income and Employment Stability

Reported annual income provides the bank with an indication of repayment capacity. Stable employment, especially in a long‑term position, can boost confidence in the borrower’s ability to manage higher balances.

3. Existing Debt Obligations

The bank reviews total outstanding debt, including mortgages, student loans, and other credit cards. A lower debt‑to‑income (DTI) ratio signals that the applicant can comfortably handle additional credit.

4. Credit Utilization on Existing Accounts

Current utilization rates across all credit lines are examined. Low utilization suggests disciplined credit use, encouraging the bank to assign a higher limit.

5. Banking Relationship

Customers who already maintain checking or savings accounts with US Bank may receive preferential treatment. A strong banking relationship can serve as an additional assurance of financial responsibility.

Factors That Can Change Your Limit Over Time

Even after the initial assignment, the US Bank Shield Visa credit limit is not static. Several events and behaviors can trigger a review, leading to either an increase or a reduction.

Periodic Review Process

US Bank conducts annual or semi‑annual reviews for many credit products. During these reviews, the bank reassesses the cardholder’s credit profile, income changes, and payment patterns. If the review is favorable, the limit may be automatically raised.

Requesting a Manual Increase

Cardholders can proactively request a limit increase through the online banking portal or by calling customer service. The bank will then evaluate the request based on the latest financial information supplied by the applicant.

Significant Life Events

- Promotion or salary raise.

- Purchase of a new home or car, which may affect debt ratios.

- Graduation from school, leading to a change in employment status.

Negative Triggers

Late payments, increased credit utilization, or new delinquencies on other accounts can prompt the bank to lower the limit as a risk mitigation measure.

Strategies to Increase Your US Bank Shield Visa Credit Limit

For many users, a higher limit is a goal that aligns with better credit utilization and greater purchasing flexibility. Below are evidence‑based strategies that can improve the likelihood of receiving an increase.

Maintain Timely Payments

Pay the full statement balance or at least the minimum payment by the due date each month. Consistent on‑time payments demonstrate reliability and reduce perceived risk.

Keep Utilization Below 30%

Even with a modest limit, keeping balances well below 30% of the available credit sends a positive signal to the issuer. This habit also protects your FICO score from the negative impact of high utilization.

Report Income Increases Promptly

When you receive a raise or start a higher‑paying job, update your income information through the US Bank online portal. A higher reported income can directly influence the limit‑increase decision.

Leverage Existing Banking Relationships

If you have other US Bank accounts, consider consolidating some of your financial activities there. Demonstrating a broader relationship can make the bank more comfortable extending additional credit.

Request a Limit Increase After a Positive Credit Event

Timing your request after a credit score boost (e.g., after a successful debt payoff) can improve the odds of approval. Include supporting documentation, such as recent pay stubs, to strengthen the case.

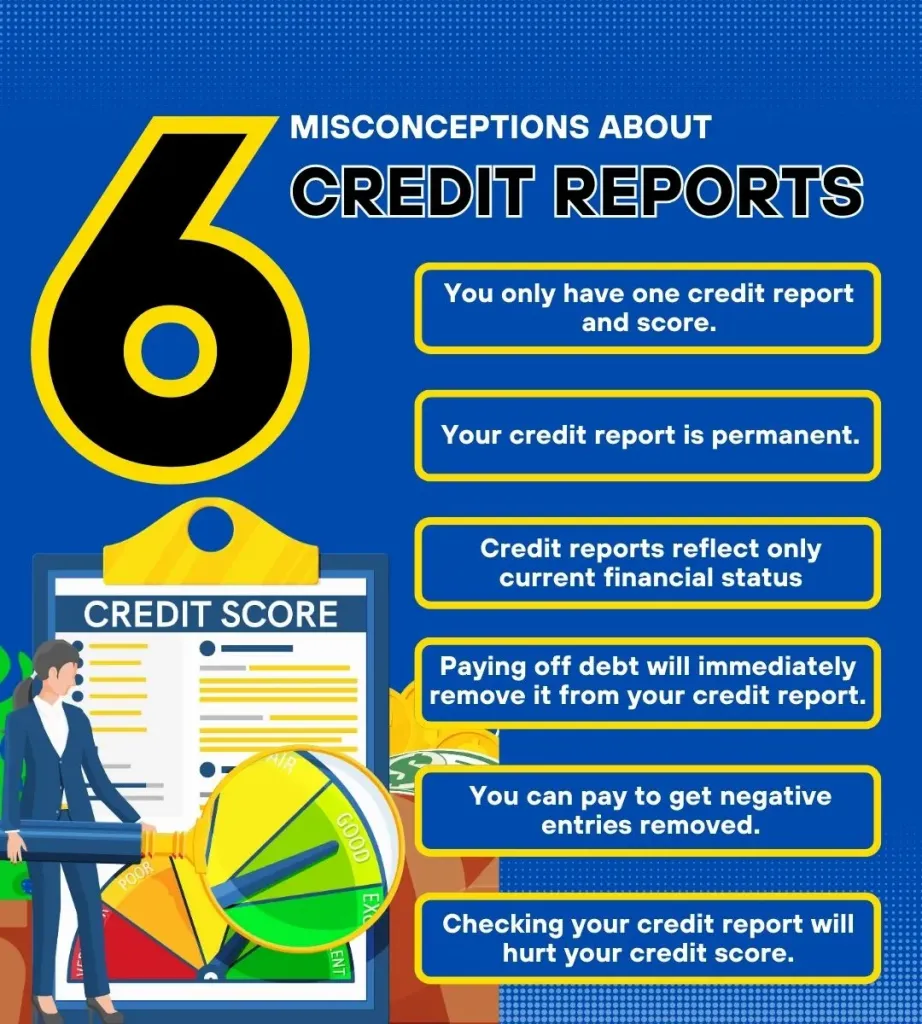

Common Misconceptions About Credit Limits

Misunderstandings about how credit limits work can lead to suboptimal financial decisions. Clarifying these myths helps cardholders avoid unnecessary pitfalls.

Myth: A Higher Limit Means Higher Debt

A higher limit does not compel you to spend more. In fact, it can lower your utilization ratio, which benefits your credit score if you maintain the same spending level.

Myth: Requesting an Increase Will Hurt Your Credit Score

US Bank typically performs a “soft pull” when you request a limit increase, meaning the inquiry does not affect your credit score. Only if a “hard pull” is required will there be a minor impact, and the bank usually informs you beforehand.

Myth: Only New Cardholders Can Get Increases

Long‑standing cardholders who demonstrate consistent responsible use are often eligible for automatic or discretionary increases during periodic reviews.

Managing Your Shield Visa Credit Responsibly

Having a clear understanding of the limit is only half the equation; managing it responsibly completes the picture. Below are best practices to keep your credit health intact.

Set Up Automatic Payments

Enroll in automatic payments for at least the minimum amount due. This eliminates the risk of missed payments, which can quickly erode your credit standing.

Monitor Statements Regularly

Review transaction details each month to spot any unauthorized activity early. US Bank offers real‑time alerts that can be customized for purchases over a certain amount.

Use the Card for Planned Purchases Only

Allocate the Shield Visa for recurring expenses such as groceries, gas, and subscriptions—categories that earn cash back. This strategy maximizes rewards while keeping spending predictable.

Consider Paying More Than the Minimum

When possible, pay the full balance to avoid interest charges. If you need to carry a balance, paying more than the minimum reduces overall interest costs and demonstrates financial discipline.

Leverage Online Banking Tools

The US Bank website includes a credit‑limit calculator and utilization tracker. Using these tools helps you visualize how different spending scenarios affect your credit health.

By integrating these habits into your routine, you not only protect your current credit limit but also position yourself for future increases. Responsible management, combined with a clear grasp of the underlying factors, creates a virtuous cycle of financial well‑being.

For those interested in broader banking strategies, exploring how to open a business bank account online can complement personal credit management. The Fast‑Track Guide to opening a business bank account offers actionable steps that align with the disciplined approach outlined here.

Similarly, understanding wealth management options such as those provided by JPMorgan Private Bank can provide insight into how high‑net‑worth individuals manage credit limits alongside investment portfolios. Read more in the article Inside JPMorgan Private Bank – The Elite Wealth Management Engine for a deeper perspective.

Finally, if you are transitioning from a personal credit card to a small business credit line, the process of securing an online business bank account quickly and hassle‑free offers useful parallels. The guide How to Secure an Online Business Bank Account Quickly and Hassle‑Free highlights steps that echo many of the credit‑limit considerations discussed for the Shield Visa.

In summary, the US Bank Shield Visa card credit limit is determined by a blend of credit score, income, existing debt, utilization, and banking relationship. By maintaining timely payments, low utilization, and updated income information, you can influence the limit positively. Avoid common myths, use the card for planned purchases, and leverage US Bank’s digital tools to keep your credit health on track. With disciplined use, the Shield Visa can serve as a reliable financial instrument that supports both everyday spending and long‑term credit growth.