Credit card and ACH payment processing are the two most common ways businesses move money in the digital age. Understanding how each system works helps merchants choose the right tool for their cash flow, customer experience, and bottom line. This article walks you through the inner workings, compares the two methods, and offers practical guidance for integrating them into your operations.

Imagine a small online retailer that suddenly receives a surge of orders during a holiday promotion. The retailer’s ability to accept payments quickly, securely, and at a reasonable cost can determine whether the promotion turns into profit or lost sales. By the end of this story, you will see why the choice between credit card and ACH processing matters and how to make that choice wisely.

Understanding Credit Card Processing

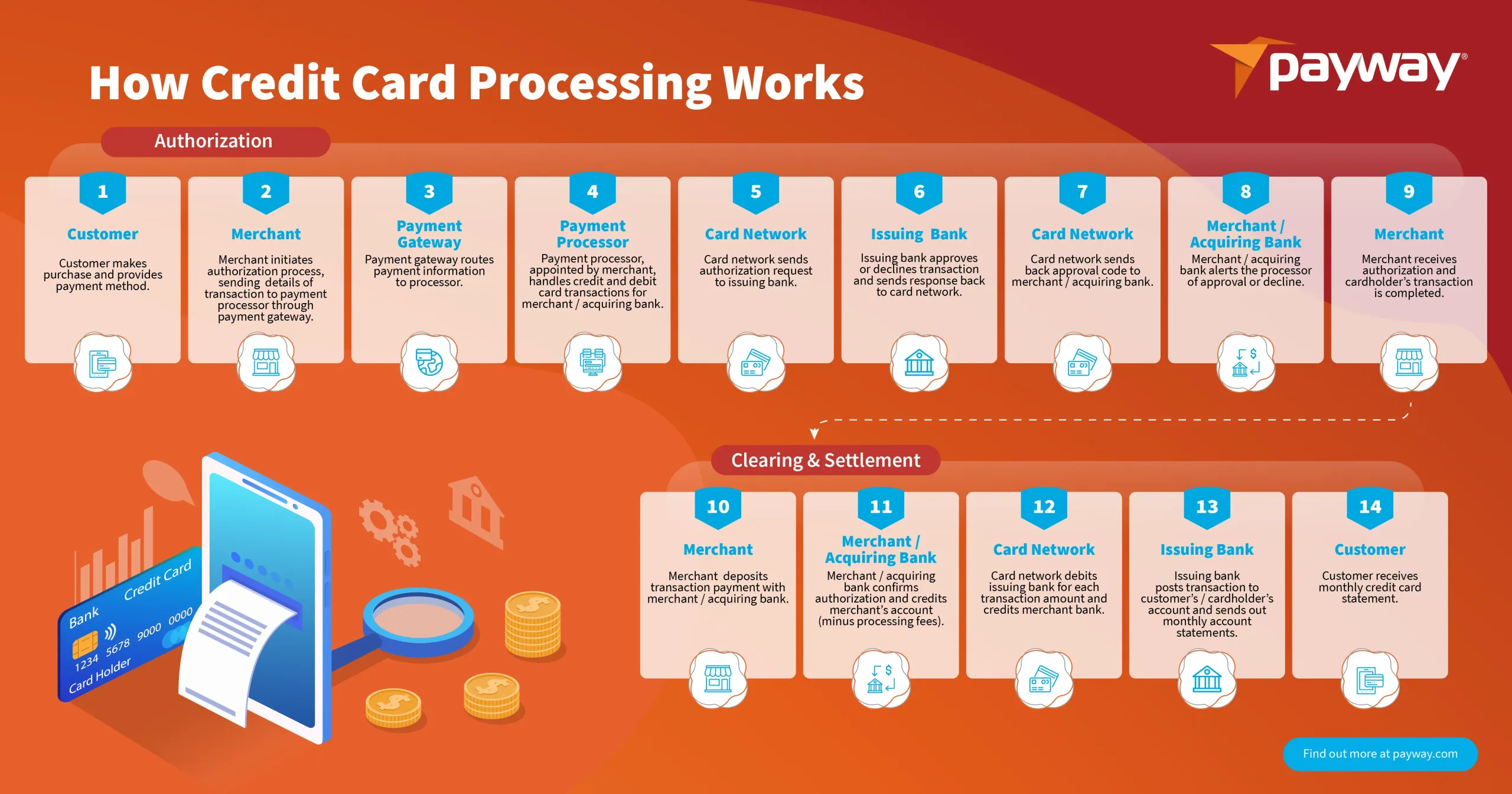

When a customer swipes, taps, or enters a credit card number on a website, a complex network of parties springs into action. The process begins with the merchant’s point‑of‑sale (POS) or e‑commerce platform, which captures the card data and sends it to the acquiring bank (the merchant’s bank). The acquiring bank forwards the transaction request to the card network—Visa, Mastercard, Discover, or American Express—where it is routed to the issuing bank that actually holds the customer’s credit line.

The issuing bank checks the cardholder’s balance, validates the security codes, and decides whether to approve or decline the transaction. An approval code travels back through the network to the acquiring bank, which then deposits the funds into the merchant’s account, usually within one to two business days. This entire journey, from swipe to settlement, is called the authorization‑capture‑settlement cycle.

For a deeper dive into the nuances of credit card processing, see The Ultimate Guide to Credit Card Processing for Online Businesses – Boost Sales & Slash Fees. That guide explains how fees are structured, how to negotiate rates, and how to optimize the checkout experience.

Key Components of Credit Card Processing

- Merchant Account: A specialized account that allows the business to accept card payments.

- Payment Gateway: Software that encrypts card data and transmits it securely to the acquiring bank.

- Acquiring Bank (Acquirer): The financial institution that processes card transactions on behalf of the merchant.

- Card Network: The scheme (Visa, Mastercard, etc.) that sets the rules and routes the transaction.

- Issuing Bank: The bank that issued the credit card to the consumer and authorizes the payment.

Typical Fees Associated with Credit Cards

Credit card processing fees usually consist of three parts: interchange, assessment, and the processor’s markup. Interchange fees are set by the card networks and vary by card type, transaction size, and merchant category. Assessment fees are a small percentage charged by the network for each transaction. Finally, the processor adds its own markup, which may be a flat fee, a percentage, or a blend of both.

High‑risk merchants—those in industries such as travel, gaming, or subscription services—often face higher interchange rates and additional underwriting requirements. For insight into the challenges high‑risk merchants encounter, refer to Understanding the Landscape of High‑Risk Credit Card Processing.

ACH Payment Processing Explained

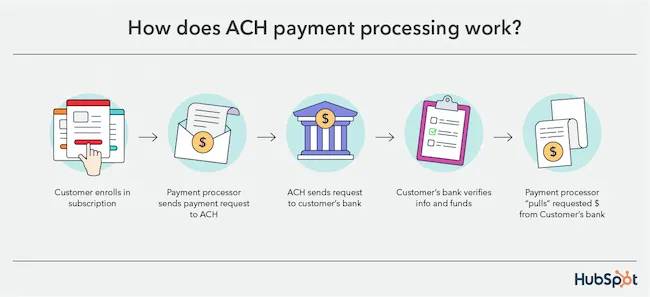

Automated Clearing House (ACH) is an electronic network used for batch‑processing of financial transactions in the United States. Unlike the real‑time nature of credit card authorizations, ACH moves money in groups, typically once or twice per business day. When a consumer authorizes an ACH debit—often called a direct debit—the merchant’s bank sends a file of transaction details to its ACH operator (the Federal Reserve or a private clearinghouse). The operator then routes the file to the consumer’s bank, which debits the consumer’s checking or savings account and credits the merchant’s account.

Because ACH relies on the banking system rather than a card network, the cost structure is simpler and generally lower. Most ACH transactions carry a flat fee ranging from $0.20 to $1.50, with no percentage component. Settlement usually occurs within one to three business days, depending on whether the transaction is a standard ACH or an ACH “same‑day” credit.

How ACH Works – Step by Step

- Authorization: The consumer provides bank account details and consents to the debit or credit.

- File Creation: The merchant’s software compiles a batch file of all ACH entries for the day.

- Submission: The batch file is transmitted to the merchant’s ACH processor.

- Clearing: The processor forwards the file to the ACH operator, which sorts and routes it.

- Settlement: Funds are moved between the consumer’s and merchant’s banks, completing the transaction.

When ACH Is Most Effective

- Recurring payments such as subscriptions, utilities, or rent.

- High‑ticket B2B invoices where the percentage fees of credit cards would be prohibitive.

- Businesses that prioritize lower transaction costs over instant settlement.

Comparing Credit Card and ACH Processing

Both payment methods have distinct strengths and trade‑offs. Choosing the right one depends on factors like transaction size, customer preferences, and cost sensitivity.

Cost Considerations

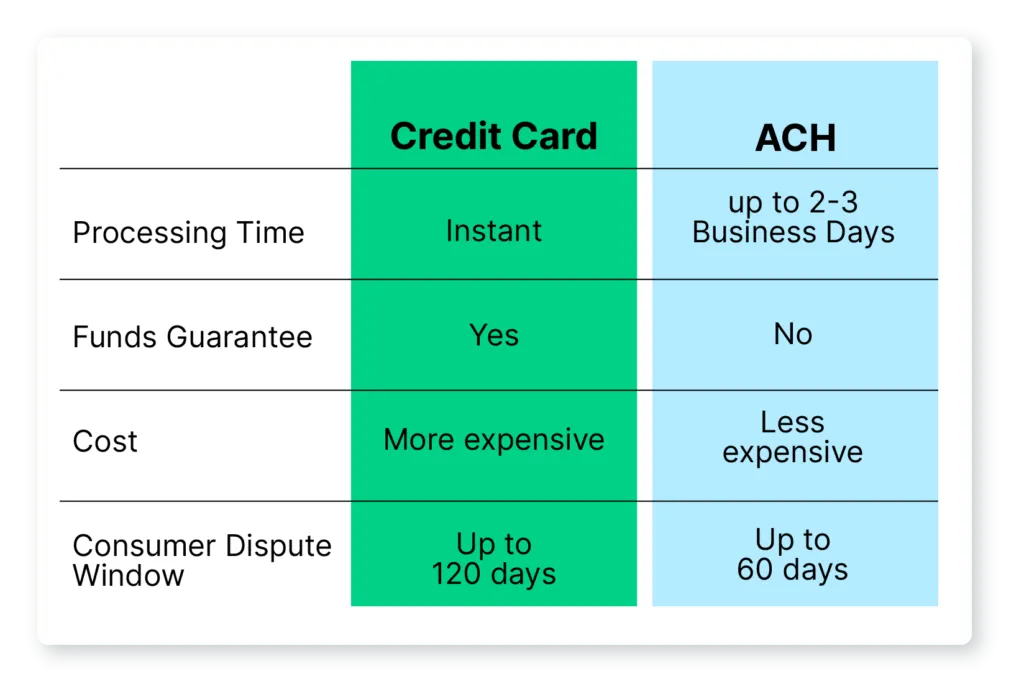

Credit cards typically charge 1.5%–3.5% of the transaction amount plus a flat fee, while ACH fees stay flat regardless of amount. For a $500 purchase, a credit card could cost $12.50–$20 in fees, whereas ACH might cost just $0.30. Over thousands of transactions, those differences compound dramatically.

Settlement Speed

Credit card settlements are often completed within 24–48 hours, making them ideal for merchants who need quick cash flow. ACH, on the other hand, can take 1–3 days for standard entries, though same‑day ACH offers faster processing at a modest premium.

Risk and Chargebacks

Credit card transactions carry a higher risk of chargebacks—disputed transactions that can be reversed by the issuing bank. Merchants must maintain robust evidence and may incur additional fees for each chargeback. ACH transactions have a lower chargeback rate, but they are subject to “Unauthorized Debit” claims within a limited window (usually 60 days). The risk profile influences how merchants design their fraud prevention and dispute handling procedures.

Customer Experience

Consumers are accustomed to the speed and convenience of credit card checkout. The frictionless experience of entering a card number or using digital wallets can boost conversion rates. ACH requires the customer to provide bank routing and account numbers, which can feel more invasive. However, for B2B clients and large‑ticket purchases, many buyers prefer ACH to avoid credit card fees.

Choosing the Right Solution for Your Business

Many businesses opt for a hybrid approach—accepting credit cards for low‑value, impulse purchases while offering ACH for high‑value or recurring payments. This strategy balances convenience, cost, and cash‑flow needs.

Factors to Evaluate

- Average Transaction Value (ATV): High ATVs favor ACH due to flat fees.

- Payment Frequency: Recurring billing aligns well with ACH.

- Customer Demographics: Younger consumers may prefer card payments; older or corporate clients may lean toward ACH.

- Integration Capabilities: Ensure your e‑commerce platform or accounting software can handle both payment types.

- Security and Compliance: PCI‑DSS applies to credit cards; NACHA rules govern ACH. Both require encryption, tokenization, and audit trails.

Integration and Security Best Practices

When adding a new payment method, start by selecting a processor that supports both credit card and ACH APIs. This reduces the need for multiple vendor relationships and simplifies reporting. Implement tokenization to store payment details securely, and use multi‑factor authentication for access to the payment dashboard.

If you are looking to expand your credit options, consider reading How to Seamlessly Apply for a Business Credit Card Online – The Complete 2026 Guide. That article outlines steps to obtain a business credit card, which can be paired with ACH to give you a full suite of payment options.

Future Trends

Emerging technologies such as real‑time payments (RTP) and open banking are blurring the lines between card and ACH processing. RTP enables instant settlement of bank‑to‑bank transfers, while open banking APIs allow merchants to initiate payments directly from consumer bank accounts with the same speed as credit cards. Keeping an eye on these developments can help you stay competitive.

In practice, most merchants today will continue to use both credit card and ACH channels, adjusting the mix as their business evolves. By monitoring transaction data, assessing fee structures, and staying informed about regulatory changes, you can fine‑tune your payment strategy for optimal performance.

Whether you run a boutique e‑store, a SaaS platform, or a wholesale distribution business, understanding the mechanics behind credit card and ACH processing empowers you to make data‑driven decisions. The right combination reduces costs, improves cash flow, and delivers a smoother experience for your customers.