Graduating with a degree often means stepping into a world of financial obligations, and private student loans are a common part of that reality. As interest rates fluctuate and personal circumstances evolve, many borrowers find themselves asking, should i refinance my private student loans to achieve better terms? This question isn’t merely about chasing a lower rate; it’s about aligning debt management with long-term financial goals.

Refinancing can appear enticing when you see a headline offering a 3% interest rate compared to the 6% you’re currently paying. Yet, the decision involves more than the headline number. It requires an assessment of your credit health, employment stability, and the trade‑offs between federal protections and private flexibility. In this article we’ll walk through the essential considerations, break down the mechanics of refinancing, and provide a step‑by‑step roadmap to help you answer the question with confidence.

Should I Refinance My Private Student Loans? Core Factors to Evaluate

Answering the core question, should i refinance my private student loans, begins with a clear picture of your current loan landscape. Below are the primary variables that should influence your decision:

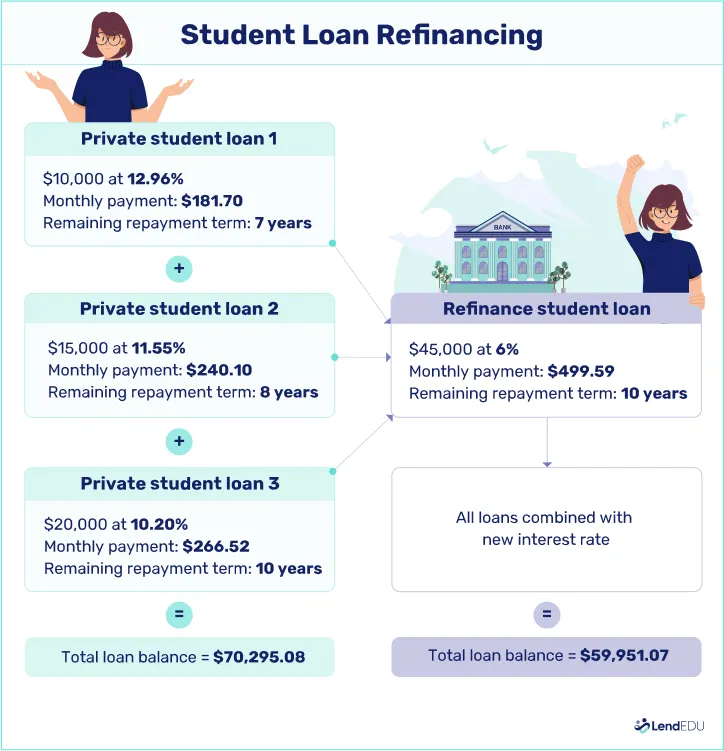

- Current interest rate vs. market rates: Compare your existing rate with the rates offered by reputable lenders. Even a 0.5% reduction can translate into significant savings over a 10‑year term.

- Credit score and credit history: Private lenders heavily weigh creditworthiness. A higher score often unlocks the best rates.

- Employment stability and income trajectory: Predictable income supports a longer repayment term, which can lower monthly payments but increase total interest paid.

- Loan term preferences: Decide whether you prefer a shorter term with higher payments to reduce interest, or a longer term for lower monthly cash flow impact.

- Federal loan benefits: Private loans lack income‑driven repayment plans, deferment, forbearance, and forgiveness options that federal loans provide. Losing those protections is a critical trade‑off.

Should I Refinance My Private Student Loans? Eligibility Checklist

Before you start shopping for a new lender, run through this quick eligibility checklist:

- Credit score of at least 670 for competitive rates; 720+ for the best offers.

- Stable employment for the past two years, with a verifiable income stream.

- Debt‑to‑income (DTI) ratio below 40%—lenders want to see you can comfortably manage payments.

- All existing private loans are in good standing (no recent delinquencies).

- Willingness to consolidate multiple loans into a single account, if that simplifies repayment.

If you meet most of these criteria, the odds are favorable that you’ll qualify for a refinance that improves your financial picture. However, if your credit or income is still developing, consider waiting until you can secure a stronger offer.

Benefits of Refinancing Private Student Loans

When the answer to should i refinance my private student loans is “yes,” the benefits can be tangible and far‑reaching:

- Lower interest rates: A reduction even by a few basis points cuts monthly payments and total interest.

- Simplified payments: Consolidating several loans into one reduces administrative hassle.

- Customizable terms: Choose a repayment period that aligns with cash flow needs—5, 10, or 15 years, for example.

- Potential credit boost: Consistently paying a refinanced loan on time can improve your credit score over time.

These advantages are especially compelling for borrowers who have progressed in their careers and now qualify for rates that were previously out of reach.

Potential Drawbacks and Risks

Even with appealing benefits, there are notable risks tied to the question, should i refinance my private student loans:

- Loss of federal protections: If any of your private loans originated as federal loans, refinancing turns them into purely private obligations, eliminating access to income‑driven repayment or forgiveness programs.

- Variable‑rate exposure: Some lenders offer variable rates that can rise unexpectedly, increasing your payment burden.

- Longer repayment term trap: Extending the loan term lowers monthly payments but can increase total interest paid by thousands of dollars.

- Origination fees: Some lenders charge a fee upfront, which can offset savings if the loan balance is modest.

Balancing these trade‑offs requires a realistic assessment of both present and future financial conditions. If you anticipate a drop in income, for instance, retaining the ability to defer or forbear might outweigh a modest rate reduction.

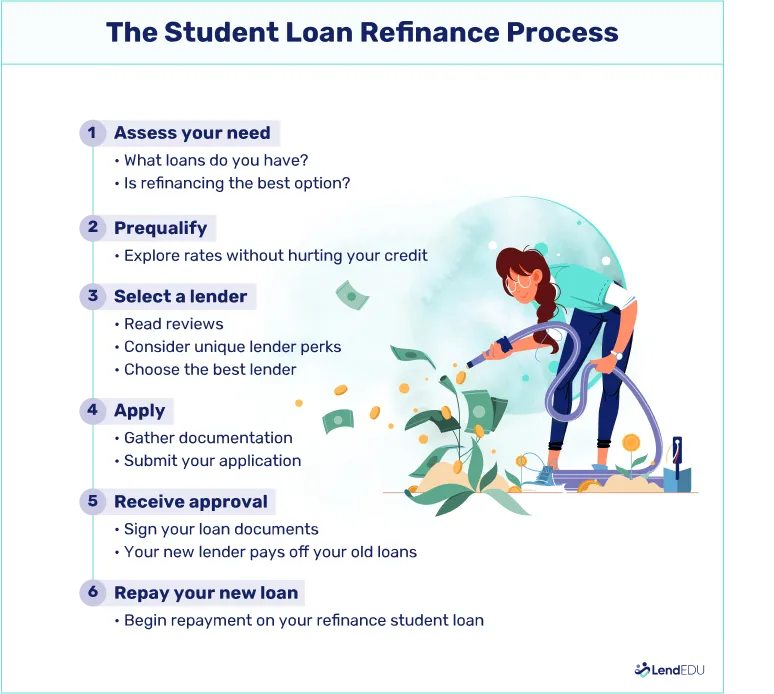

How to Refinance: Step‑by‑Step Process

Now that you’ve weighed the pros and cons, let’s walk through the practical steps to answer should i refinance my private student loans with a concrete plan.

1. Gather Loan Information

Collect the principal balance, interest rate, remaining term, and monthly payment for each private loan. Having these details on hand enables accurate comparisons with refinance offers.

2. Check Your Credit Score

Obtain a free credit report from one of the major bureaus. If your score has improved since you first borrowed, you’re in a stronger negotiating position.

3. Shop Around for Lenders

Use online marketplaces or directly visit lender websites. Pay attention to:

- APR (annual percentage rate) – reflects the true cost of borrowing.

- Fixed vs. variable rates.

- Loan term options.

- Any application or origination fees.

For a broader perspective on borrowing options, you might also explore how to apply for a business loan online – a complete guide, which outlines the documentation and credit considerations common across many loan types.

4. Use a Loan Calculator

Plug your numbers into a refinance calculator. Compare the projected monthly payment and total interest of the new loan against your current schedule. This quantitative view helps answer should i refinance my private student loans with data rather than intuition.

5. Submit Applications

Most lenders allow you to apply online. You’ll typically need:

- Personal identification (SSN, driver’s license).

- Proof of income (pay stubs, tax returns).

- Existing loan statements.

Submitting multiple applications within a short window usually results in a single hard inquiry, preserving your credit score.

6. Review the Offer and Sign

Read the terms carefully. Verify the interest rate, repayment schedule, and any prepayment penalties. Once satisfied, sign the agreement, and the lender will pay off your existing private loans directly.

Alternatives to Refinancing

If you remain uncertain about should i refinance my private student loans, consider these alternatives before committing:

- Income‑Driven Repayment (IDR) plans: While primarily for federal loans, some private lenders now offer income‑based options.

- Loan forgiveness programs: Certain public service or employer‑sponsored programs may provide partial forgiveness—usually unavailable after refinancing.

- Partial repayment: Making extra payments on high‑interest loans without consolidating can reduce overall interest.

- Forbearance or deferment: If you’re temporarily unable to pay, exploring my student loans are in forbearance – a complete guide can give you breathing room without changing loan terms.

Each alternative carries its own set of eligibility criteria and long‑term implications. Weigh them against the potential savings of a refinance to determine the most suitable path.

Impact on Credit Score

Refinancing can have a short‑term dip in your credit score due to a hard inquiry, but the long‑term effect is generally positive if you maintain on‑time payments. A lower credit utilization ratio—resulting from a consolidated balance—also contributes to score improvement. Conversely, missing payments on a refinanced loan can cause a sharper decline than if you had kept the original loans, because the new loan often carries a larger balance.

Frequently Asked Questions

Can I refinance only part of my private student loans?

Yes. Some lenders allow partial refinancing, letting you keep a portion of the original loan untouched while consolidating the rest. This can be useful if you want to retain a loan with a particularly low rate.

Do I need a cosigner?

If your credit score is below the lender’s threshold, adding a credit‑worthy cosigner can help you secure a better rate. Remember that the cosigner becomes legally responsible for the debt.

Will refinancing affect my ability to claim tax deductions?

Student loan interest is tax‑deductible up to $2,500 per year, regardless of whether the loan is federal or private. Refinancing does not change this eligibility, but you must still meet the income limits set by the IRS.

Is there a difference between refinancing and consolidating?

Consolidation typically refers to combining multiple loans into one, often through a federal program. Refinancing, on the other hand, involves replacing existing private loans with a new loan—usually from a private lender—potentially at a different interest rate or term.

How long does the refinance process take?

Once approved, most lenders complete the payoff of existing loans within 10‑14 business days. The entire application cycle, from submission to funding, can be as short as one week if documentation is complete.

Answering the central question—should i refinance my private student loans—requires a holistic view of your financial landscape. If you have a solid credit profile, stable income, and can afford a potentially higher monthly payment for a shorter term, refinancing often yields meaningful savings. Conversely, if you rely on federal protections or anticipate income volatility, retaining the original loans may be wiser.

Ultimately, the decision rests on aligning loan terms with personal goals: whether that means minimizing total interest, freeing up monthly cash flow, or preserving flexibility for future life events. Take the time to calculate, compare, and consider alternatives, and you’ll be equipped to make an informed choice that supports your long‑term financial health.