Finding the right protection for both your vehicle and your residence used to involve countless phone calls, endless paperwork, and visits to local agents. Today, a simple web browser and a few minutes of your time can produce a detailed picture of the market, allowing you to compare policies side‑by‑side. This transformation has not only streamlined the buying process but also empowered consumers to make data‑driven decisions about their coverage.

In this article we explore the mechanics behind obtaining online car and home insurance quotes, the technology that powers the process, and practical steps you can take to ensure the figures you see are accurate and comparable. Whether you are a first‑time buyer, a seasoned policyholder looking to switch, or simply curious about how digital platforms have reshaped the industry, the information here will help you navigate the landscape with confidence.

We’ll also touch on common pitfalls, such as overlooking hidden fees or misinterpreting coverage limits, and provide actionable tips to avoid them. By the end of the piece, you’ll have a clear roadmap for securing the best possible rates while maintaining the level of protection you need for both your car and your home.

How Online Car and Home Insurance Quotes Are Generated

The core of any digital insurance platform is a sophisticated algorithm that pulls data from multiple sources—public records, driver histories, property assessments, and even real‑time weather patterns. When you enter basic information—like your vehicle’s make, model, year, and your home’s square footage, construction type, and location—the system instantly cross‑references this data against underwriting criteria used by dozens of insurers.

Most providers rely on a combination of:

- Credit‑based insurance scores that predict risk based on financial behavior.

- Telematics data for car insurance, which may include mileage, driving speed, and braking habits.

- Geospatial analysis for home insurance, assessing flood zones, fire risk, and crime statistics.

Because these inputs are standardized, the resulting online car and home insurance quotes are generated within seconds, allowing you to view multiple offers on a single screen. This speed is made possible by API integrations that connect comparison sites directly to insurers’ underwriting engines.

Key Factors That Influence Your Online Car and Home Insurance Quotes

Understanding the variables that affect pricing will help you interpret the numbers you receive. Below are the most common drivers of premium differences:

- Driving record: A clean record typically reduces car insurance rates, while violations or accidents raise them.

- Vehicle type: High‑performance or luxury cars often cost more to insure due to repair costs and theft rates.

- Home age and construction: Older homes or those built with less fire‑resistant materials may attract higher home insurance premiums.

- Location: Urban areas with higher traffic density or crime rates can increase both car and home insurance costs.

- Deductibles and coverage limits: Choosing higher deductibles generally lowers premiums, but it also means you’ll pay more out‑of‑pocket after a claim.

- Bundling discounts: Many insurers offer a discount when you purchase both car and home policies from the same company, which is often reflected in the online car and home insurance quotes you receive.

When you see a quote that looks unusually low, double‑check that the coverage limits and deductibles match what you need. A lower price can sometimes mean reduced protection or omitted endorsements that you might consider essential.

Steps to Obtain Accurate Online Car and Home Insurance Quotes

While the technology does the heavy lifting, the quality of your results still depends on the information you provide. Follow these steps for the most reliable figures:

- Gather essential documents: Have your driver’s license, vehicle registration, current insurance policy, and recent mortgage or property tax statements handy.

- Enter precise details: Input the exact mileage, VIN, and any safety or anti‑theft devices installed in your car. For your home, note the square footage, roof type, and any recent renovations.

- Use multiple comparison sites: Different platforms may have exclusive partnerships with certain carriers, so checking more than one can uncover additional options.

- Review coverage options: Look beyond the base premium; examine liability limits, comprehensive coverage, personal property protection, and optional riders such as flood insurance.

- Check for discounts: Look for multi‑policy, good‑driver, low‑mileage, or loyalty discounts that could further lower your final cost.

- Validate insurer’s financial strength: A low premium is attractive, but you also want a company that can pay claims. Resources like the Financial Strength and Industry Reputation guide can help you assess stability.

After you have a shortlist of promising offers, it’s wise to contact the insurer directly to verify any nuances that the online form may not capture. This step can also uncover additional savings opportunities that aren’t displayed on comparison pages.

Common Pitfalls When Using Online Quote Tools

Even with a streamlined process, users sometimes encounter obstacles that can lead to inaccurate or misleading results. Being aware of these issues can save you time and money.

Over‑reliance on the Lowest Price

The most tempting quote is often the cheapest one. However, a minimal premium might exclude coverage for events like natural disasters, which can be critical depending on your region. Always compare the coverage details, not just the price tag, when evaluating online car and home insurance quotes.

Incomplete or Inaccurate Data Entry

Missing a single detail—such as the presence of a home security system or a driver’s annual mileage—can skew the calculations. Double‑check each field before submitting the form to ensure the algorithm has the full picture.

Ignoring Policy Exclusions

Every policy has exclusions—situations that are not covered. For example, some home policies exclude damage from mold unless it’s a result of a covered peril. Understanding these exclusions before you purchase is essential to avoid surprise claim denials.

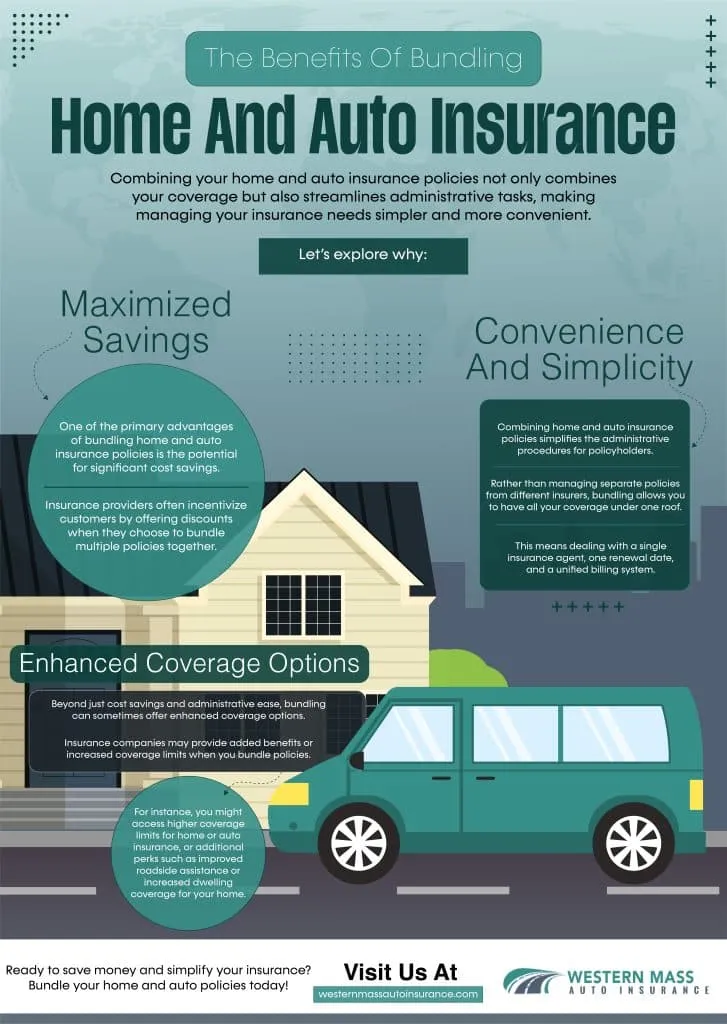

Benefits of Bundling Car and Home Insurance Online

One of the biggest advantages of using digital platforms is the ease with which you can bundle policies. Most insurers provide a single quote that reflects discounts for holding both a car and a home policy. Bundling can lead to savings of 10‑20% on the combined premium, and it simplifies claims management by giving you a single point of contact.

When you request online car and home insurance quotes together, the comparison engine can instantly calculate the bundled discount, allowing you to see the net cost versus purchasing each policy separately. This transparency helps you decide whether the convenience and savings outweigh any potential trade‑offs in coverage flexibility.

How to Transition from Quote to Policy

Once you’ve identified the best offer, the transition to an active policy is typically straightforward. Most insurers allow you to finalize the purchase online, upload necessary documents, and set up automatic payments—all within a few clicks.

Before you click “Buy,” verify the following:

- All personal and vehicle/home details match the information used for the quote.

- The policy start date aligns with any existing coverage to avoid gaps.

- You have read and understood the cancellation process, which can be useful if you later decide to switch providers. For guidance on cancellation, see How to Cancel Your Allstate Insurance – Complete Guide.

After payment, you’ll receive an electronic proof of insurance, which can be printed or saved on your mobile device. Many carriers also provide an online portal where you can track claims, adjust deductibles, and add endorsements as your needs evolve.

In summary, the digital age has transformed the way consumers obtain online car and home insurance quotes. By understanding the underlying data, carefully entering accurate information, and scrutinizing coverage details, you can secure a policy that balances cost and protection. The convenience of bundling, the transparency of side‑by‑side comparisons, and the ability to switch providers with minimal friction all contribute to a more empowered insurance experience.

As you move forward, remember that the cheapest quote isn’t always the best. Focus on comprehensive coverage, the insurer’s reputation, and the specific risks pertinent to your vehicle and property. With these considerations in mind, you’ll be well positioned to protect what matters most, all while enjoying the efficiency that online quoting platforms provide.