When you hear the name “Cit Bank,” the first question that often arises is whether this entity is a bona‑fide, regulated financial institution. The phrase “Cit Bank” can appear in various contexts – from online advertisements promising high‑yield savings accounts to social media posts discussing joint accounts. Understanding the legitimacy of Cit Bank is essential for anyone considering a relationship with the brand, especially in a landscape where fraudsters frequently imitate reputable banks.

In this article, we will trace the origins of Cit Bank, examine the regulatory framework that governs it, and outline practical steps you can take to verify its authenticity. By the end, you should have a clear, fact‑based picture of whether Cit Bank meets the standards of a legitimate bank, without relying on speculation or unverified claims.

Historical Background and Corporate Identity

Cit Bank is not a brand that stands alone; rather, it is a shorthand or colloquial reference to a specific subsidiary within the larger Citigroup umbrella. Citigroup Inc., founded in 1998 through the merger of Citicorp and Travelers Group, is a global financial services corporation headquartered in New York City. The institution operates under the name “Citibank” for its consumer banking division, which is widely recognized and regulated in multiple jurisdictions.

Over the years, the name “Cit Bank” has occasionally been used in marketing materials, particularly in regions where a shorter brand name is preferred for local audiences. Despite the naming variation, the underlying entity remains the same – a fully chartered bank that is subject to the oversight of major regulatory bodies such as the Federal Reserve, the Office of the Comptroller of the Currency (OCC), and the FDIC in the United States.

Key Milestones in Citibank’s Evolution

- 1864 – The original City Bank of New York is founded, later evolving into Citibank.

- 1998 – Merger of Citicorp and Travelers Group creates Citigroup, establishing one of the largest banking conglomerates worldwide.

- 2008 – After the global financial crisis, Citigroup receives a substantial U.S. Treasury bailout, reinforcing its regulatory scrutiny and capital requirements.

- 2015 – Citibank launches a suite of digital banking services, expanding its online presence and modernizing its customer experience.

Regulatory Oversight and Licensing

One of the strongest indicators of a bank’s legitimacy is the presence of a banking charter and ongoing supervision by recognized authorities. Citibank, and by extension any operation marketed as “Cit Bank,” holds a Federal Deposit Insurance Corporation (FDIC) insurance policy. This means that deposits up to $250,000 per account holder are protected by the U.S. government, a hallmark of a legitimate banking institution.

Beyond FDIC coverage, Citibank is also regulated by the Federal Reserve System, which conducts regular examinations of its capital adequacy, risk management, and compliance practices. In the United Kingdom, the bank is authorized by the Prudential Regulation Authority (PRA) and the Financial Conduct Authority (FCA), ensuring cross‑border compliance for its international customers.

How to Verify Regulatory Status

- Visit the FDIC’s BankFind tool and search for “Citibank” or “Cit Bank” to confirm the bank’s charter number and insurance status.

- Check the OCC’s database for a list of nationally chartered banks; Citibank appears with a distinct charter number.

- For non‑U.S. customers, consult the regulator’s website in your country (e.g., FCA’s register in the UK) to verify the bank’s authorization.

Products and Services Offered by Cit Bank

Cit Bank, mirroring the broader Citibank portfolio, provides a comprehensive range of financial products. These include checking and savings accounts, credit cards, personal loans, mortgages, and wealth‑management services. A notable offering that often appears in search queries is the joint account, which allows two or more individuals to share ownership of a single account while retaining separate access credentials.

For readers interested in how joint accounts work at Citibank, a detailed exploration is available in the article What Is a Joint Account and Why It Matters at Citibank. This resource explains the benefits, responsibilities, and potential pitfalls of joint ownership, helping prospective customers make informed decisions.

Interest Rates and Fee Structures

Interest rates on savings products and loans are subject to market conditions and regulatory caps. Cit Bank’s interest‑rate policies are transparent and published on its official website. The bank also provides an in‑depth analysis of its rate calculations in the article The Inside Look at What Is Cit Bank Interest Rate – How It Works and What It Means for You. By reviewing that guide, you can understand how the bank determines rates for different account tiers, and what factors could influence future adjustments.

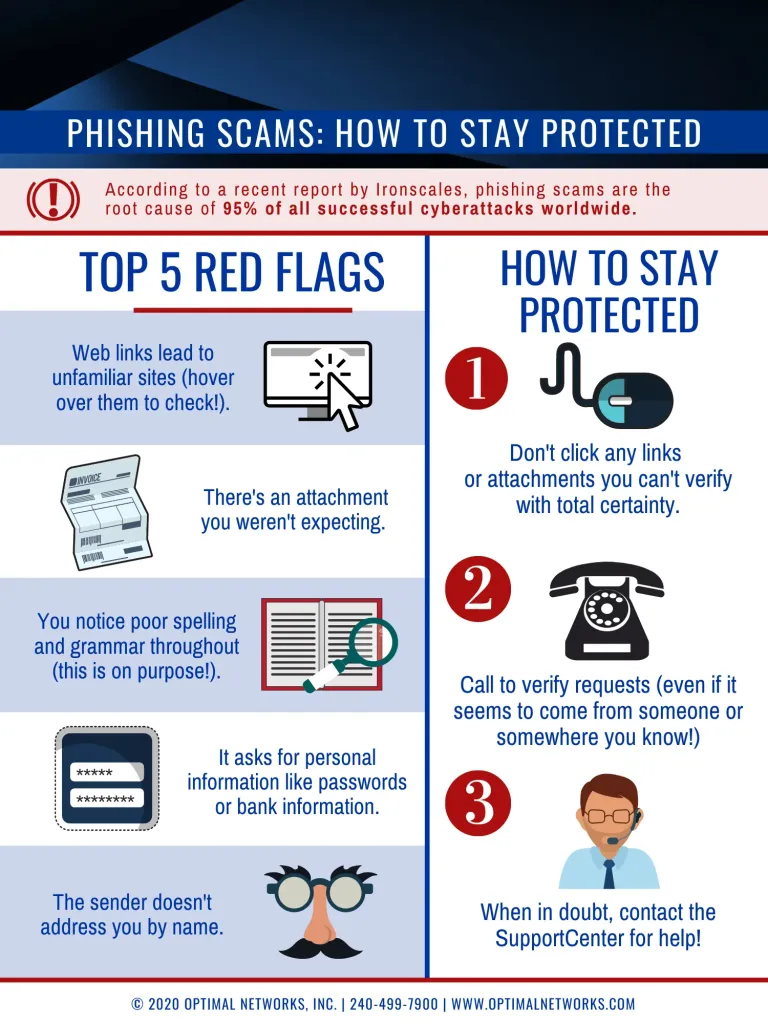

Common Red Flags and How to Avoid Scams

Even legitimate banks can become targets for phishing schemes, fake websites, and fraudulent advertisements. Below are some warning signs that the “Cit Bank” you are encountering may not be the authentic institution:

- Unusual URLs: Look for domains that deviate from the official “citi.com” address. Misspellings or extra characters often indicate counterfeit sites.

- Requests for Personal Information: Legitimate banks never ask for full passwords or PINs via email or text.

- Too‑Good‑to‑Be‑True Offers: Promises of unusually high yields or “guaranteed” returns are classic hallmarks of scams.

- Lack of Regulatory Disclosures: Authentic banks provide clear information about FDIC insurance, charter numbers, and regulatory oversight on their landing pages.

Steps to Safeguard Yourself

- Always type the bank’s URL directly into your browser instead of clicking on links from unsolicited messages.

- Enable two‑factor authentication (2FA) on your online banking portal to add an extra security layer.

- Verify any promotional offers by contacting Citibank’s official customer service line, which can be found on the bank’s verified website.

- Report suspicious activity to the Federal Trade Commission (FTC) or your local consumer protection agency.

Customer Experience and Reputation

Beyond regulatory compliance, the reputation of a bank is shaped by its customer service quality, digital platform reliability, and overall satisfaction metrics. Independent consumer surveys and rating agencies such as J.D. Power and the Better Business Bureau (BBB) consistently list Citibank among the top‑ranked banks for customer service in the United States.

Digital banking experience is another crucial factor. Citibank’s mobile app, available on both iOS and Android, supports features like instant transfers, mobile check deposit, and real‑time fraud alerts. These functionalities are regularly updated to comply with security standards, reinforcing the bank’s commitment to safeguarding user data.

Comparative Perspective

When comparing Cit Bank’s services to other major U.S. banks, several points stand out:

- Global Reach: Citibank operates in more than 100 countries, offering cross‑border account management that many regional banks cannot match.

- Technology Investment: The bank invests heavily in AI‑driven risk analysis and cybersecurity, positioning it ahead of many traditional institutions.

- Fee Structure: While some accounts carry monthly maintenance fees, these can often be waived by meeting balance or transaction thresholds, a practice common across the industry.

Conclusion

Assessing the legitimacy of Cit Bank ultimately comes down to verifying its regulatory standing, reviewing its corporate history, and confirming that you are interacting with official channels. The bank is a fully chartered, FDIC‑insured entity under the Citibank brand, with a robust oversight framework administered by multiple financial regulators. Its product suite, from joint accounts to competitive interest‑rate offerings, aligns with those of other reputable global banks.

Nevertheless, vigilance remains essential. By employing the verification steps outlined above, you can protect yourself from impostor schemes and ensure that your banking relationship is built on a solid, trustworthy foundation. Whether you are opening a new savings account, considering a joint account, or simply exploring the bank’s interest rates, the key is to rely on official resources and to stay informed about the bank’s regulatory credentials.

As the financial industry continues to evolve, maintaining a skeptical but informed mindset will help you navigate the complexities of modern banking safely.