Applying for an online business bank account has become a routine yet crucial step for entrepreneurs looking to separate personal finances from company cash flow. The keyword “apply for online business bank account” appears right at the start because the process is now largely digital, allowing business owners to set up a professional banking relationship without stepping foot inside a branch. This article walks you through every stage, from understanding the fundamentals to completing the application and activating your new account.

In today’s fast‑moving digital economy, a reliable online banking platform not only simplifies everyday transactions but also integrates with accounting software, provides real‑time analytics, and enhances security through multi‑factor authentication. Whether you run a sole‑proprietorship, a partnership, or a corporation, the right online business account can streamline payroll, manage invoices, and give you a clearer picture of cash flow.

Before diving into the mechanics, it helps to grasp why businesses are shifting to online banking. According to a recent industry report, more than 70 % of small‑to‑medium enterprises have already opened at least one digital account, citing convenience and lower fees as primary drivers. This trend mirrors the broader move toward cloud‑based financial services, a shift that is reshaping how companies handle money.

Understanding the Basics of an Online Business Bank Account

An online business bank account functions similarly to a traditional checking account but is accessed primarily through a secure web portal or mobile app. Key features typically include:

- Free or low‑cost ACH transfers and bill payments.

- Integration with popular accounting tools like QuickBooks, Xero, and Wave.

- Instant account opening with electronic identity verification (e‑KYC).

- Advanced fraud protection, including real‑time transaction alerts.

These capabilities empower business owners to manage finances on the go, reducing reliance on physical paperwork and manual processes. Moreover, many providers offer tiered pricing models that scale with transaction volume, ensuring that growing companies only pay for what they need.

Key Benefits Over Traditional Brick‑and‑Mortar Accounts

- Speed of Setup: Most online banks can approve an application within 24–48 hours, compared with the week‑long wait times of conventional banks.

- Lower Fees: Without the overhead of maintaining physical branches, digital banks often waive monthly maintenance fees and provide unlimited transactions.

- Enhanced Transparency: Real‑time dashboards give instant insight into cash flow, helping owners make data‑driven decisions.

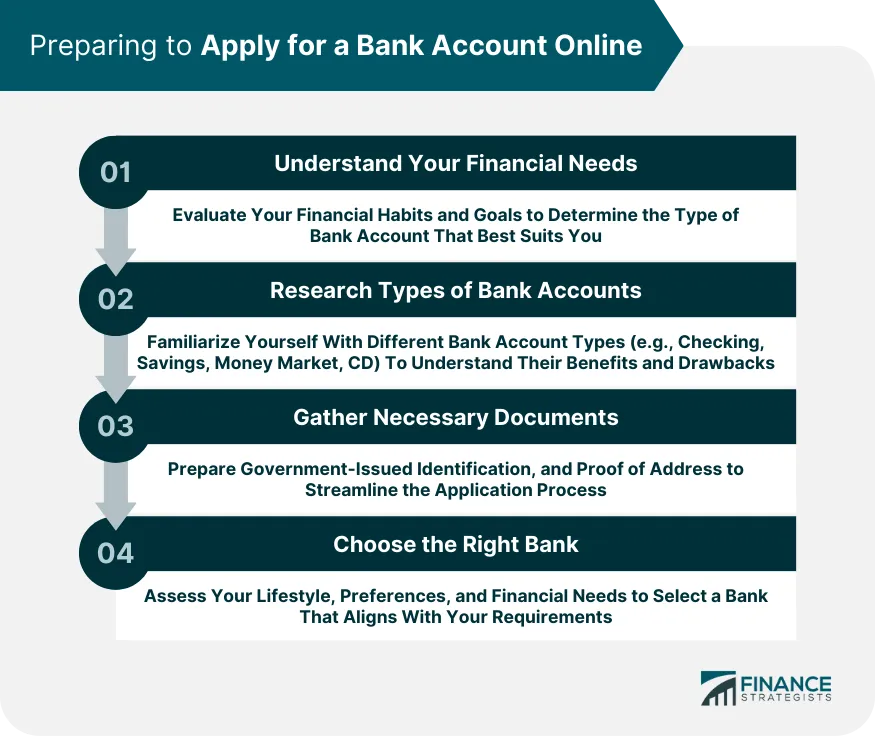

Prerequisites: Documents and Information You’ll Need

Before you click “Submit,” gather the following items to ensure a smooth application:

- Employer Identification Number (EIN): Issued by the IRS, this is the tax ID for your business.

- Business Formation Documents: Articles of Incorporation, Articles of Organization, or a DBA certificate, depending on your entity type.

- Personal Identification: Government‑issued photo ID (driver’s license or passport) for each authorized signer.

- Proof of Address: Utility bill, lease agreement, or a recent bank statement showing the business address.

- Operating Agreement or Partnership Agreement: Especially for LLCs and partnerships, to verify ownership structure.

Having these documents scanned or photographed in high resolution will prevent delays caused by illegible uploads. Some banks also request a brief description of your business activities, which can be prepared in advance.

Preparing a Business Narrative

While not always mandatory, a concise business narrative can strengthen your application. Explain what you sell, who your target market is, and how you plan to use the account. This narrative aligns well with the approach described in Historical Background and Growth Trajectory, where a clear story helps financial institutions understand a company’s long‑term potential.

Choosing the Right Online Banking Provider

The market offers a spectrum of options, from fintech‑only banks to hybrid models that combine digital interfaces with limited branch access. When evaluating providers, consider the following criteria:

- Regulatory Coverage: Ensure the bank is FDIC insured and holds a charter in your jurisdiction.

- Integration Capability: Look for native APIs or pre‑built connectors to your accounting software.

- Transaction Limits: Some digital banks cap daily ACH transfers; verify that limits match your business needs.

- Customer Support: 24/7 chat or phone support can be crucial during onboarding.

- Additional Services: Access to business credit cards, lines of credit, or merchant services may be advantageous.

For example, the Key Features of the BMO Small Business Account highlight a provider that blends robust integration with competitive fee structures, making it a solid choice for tech‑savvy startups.

Comparative Quick‑Check Table

| Provider | Monthly Fee | Free Transactions | Integration | Notable Extras |

|---|---|---|---|---|

| FinBank X | $0 | Unlimited ACH | QuickBooks, Xero | Instant virtual cards |

| Bank Y (Hybrid) | $12 | 200 per month | API access | Branch lobby in major cities |

| Traditional Bank Z | $15 | 150 per month | Limited | In‑person teller service |

Step‑by‑Step Guide to Apply for an Online Business Bank Account

Below is a practical roadmap that walks you through each phase of the application, from initial research to final activation.

- Research & Shortlist: Use the criteria above to create a shortlist of 2–3 providers.

- Gather Documentation: Scan all required documents, double‑checking that names match across forms.

- Start the Online Application: Visit the provider’s website, click “Open Business Account,” and enter basic details such as business name, EIN, and contact information.

- Identity Verification: Upload personal ID and business formation documents. Some banks employ video verification; be prepared for a brief call.

- Answer Business‑Use Questions: Provide your business narrative, anticipated monthly transaction volume, and primary banking needs.

- Review Terms & Fees: Carefully read the fee schedule, especially for outbound wire transfers and foreign currency conversions.

- Submit & Await Confirmation: Most platforms send an email within hours confirming receipt. Approval can be instant or take up to two business days.

- Fund the Account: Transfer an initial deposit—often a minimal amount, such as $100—to activate the account.

- Set Up Integrations: Connect your accounting software, enable two‑factor authentication, and configure payment gateways.

- Order Debit/ Credit Cards: If needed, request virtual or physical cards for employee expense management.

During step five, many fintech banks ask for projected monthly revenue. Providing realistic numbers helps avoid future compliance flags. If you’re unsure, refer to the guidelines in How a Business Loan Based on Bank Statements Can Unlock Growth for Your Company, which outlines how banks evaluate cash‑flow statements for loan eligibility—similar data points are used in account underwriting.

Common Pitfalls and How to Avoid Them

- Mismatched Information: Ensure the business name and EIN match exactly across all documents; a single typo can trigger a rejection.

- Insufficient Funding: Some providers require a minimum opening balance; check this before you fund the account.

- Overlooking International Capabilities: If you deal with overseas clients, verify that the bank supports SWIFT transfers and multi‑currency accounts.

- Neglecting Security Settings: Activate alerts for large transactions and set up role‑based access for employees.

Post‑Onboarding: Maximizing the Value of Your Online Business Account

Opening the account is just the beginning. To truly benefit, integrate the banking platform with your operational tools and adopt best practices for financial management.

Automate Routine Payments

Schedule recurring vendor payments, payroll runs, and tax deposits directly within the banking portal. Automation reduces manual errors and frees up time for strategic tasks.

Leverage Real‑Time Reporting

Many online banks provide dashboards that break down expenses by category, flag duplicate charges, and project cash‑flow trends. Regularly reviewing these reports helps you stay ahead of liquidity challenges.

Consider Ancillary Services

Once your account is stable, explore additional products such as a business credit card for travel rewards, a line of credit for short‑term financing, or merchant services for card‑present transactions. Bundling services with the same provider often yields discounts and simplifies bookkeeping.

Regulatory and Compliance Considerations

Even though the application process is digital, compliance obligations remain unchanged. Your online bank must adhere to the Bank Secrecy Act (BSA), anti‑money‑laundering (AML) rules, and Know‑Your‑Customer (KYC) standards. As a business owner, you are responsible for maintaining accurate records, filing required reports (e.g., IRS Form 1099‑NEC), and ensuring that all signatories are authorized.

Periodic audits may be requested, especially if your transaction volume exceeds certain thresholds. Keeping digital copies of all incorporation paperwork, board meeting minutes, and shareholder agreements in a secure cloud repository can simplify audit preparation.

Data Privacy and Security

Choose a provider that employs encryption at rest and in transit, offers biometric login options, and undergoes regular third‑party security assessments. Look for certifications such as SOC 2 Type II and ISO 27001, which indicate a mature security posture.

Future Trends: What’s Next for Online Business Banking?

The next wave of innovation is likely to involve AI‑driven cash‑flow forecasting, embedded banking services within ERP platforms, and the rise of decentralized finance (DeFi) solutions that allow businesses to earn yield on idle cash. Staying informed about these developments will help you adapt your banking strategy as the ecosystem evolves.

For businesses that anticipate rapid scaling, an online account that can seamlessly transition to more sophisticated treasury management tools will be a strategic advantage. Keep an eye on providers that announce open APIs and partnerships with fintech ecosystems, as these will enable you to build custom workflows tailored to your industry.

In conclusion, applying for an online business bank account is a streamlined, digitally‑first process that, when executed with attention to documentation, provider selection, and post‑onboarding integration, can significantly enhance financial efficiency. By following the structured steps outlined above, you can set up a robust banking foundation that supports growth, simplifies compliance, and leverages technology to keep your business agile.