Securing financing is a pivotal step for many small and medium‑size enterprises seeking to expand, purchase inventory, or bridge cash‑flow gaps. Among the various loan products available, a business loan based on bank statements has gained traction for its streamlined application process and reduced reliance on traditional credit metrics. This financing option evaluates the health of a business primarily through the cash flow reflected in its bank statements, offering an alternative pathway for businesses that may not meet conventional underwriting standards.

In this article we trace the evolution of statement‑driven lending, examine the mechanics behind the assessment, and outline the practical steps entrepreneurs should follow to position themselves for success. By the end, readers will have a clear, factual understanding of how this loan type works, what lenders look for, and how to navigate the application journey with confidence.

While the concept sounds straightforward, the nuances of documentation, eligibility thresholds, and cost structures require careful attention. The following sections break down each component, providing a roadmap that balances detail with readability.

Understanding the Fundamentals of Statement‑Based Business Loans

A business loan based on bank statements differs from traditional term loans that rely heavily on credit scores, collateral, and financial statements prepared by accountants. Instead, lenders focus on the actual inflow and outflow of funds recorded in the company’s checking and savings accounts over a defined period, typically 12 to 24 months. This approach reflects real‑time cash‑flow performance, giving lenders insight into the business’s ability to service debt.

Key Features of the Lending Model

- Cash‑flow centric evaluation: Monthly deposits, recurring expenses, and overall balance trends are analyzed to gauge repayment capacity.

- Reduced documentation: Formal profit and loss statements, balance sheets, and tax returns may be optional or supplementary.

- Flexible credit requirements: Traditional credit scores may carry less weight, allowing newer businesses or those with limited credit history to qualify.

- Speedy approval: Automated algorithms can process statements quickly, often delivering funding within days.

Typical Use Cases

Statement‑based loans are commonly used for:

- Seasonal inventory purchases

- Marketing and advertising campaigns

- Equipment upgrades

- Working‑capital bridges during slow revenue periods

Eligibility Criteria: What Lenders Look For

Although the primary focus is on bank statements, lenders still apply a set of baseline criteria to manage risk. Understanding these thresholds helps businesses assess their readiness before applying.

Revenue Consistency

Most lenders require a minimum average monthly deposit, often ranging from $5,000 to $10,000, depending on the loan amount sought. Consistency is measured by the standard deviation of monthly deposits; large fluctuations may raise concerns about cash‑flow stability.

Account Tenure

Businesses typically need to have maintained the same banking relationship for at least six months. This ensures that the statements provide a reliable picture of operating patterns.

Industry Considerations

Some sectors—such as e‑commerce, SaaS, and subscription‑based services—are viewed favorably because recurring revenue streams are evident in bank statements. Conversely, high‑risk industries may face stricter scrutiny.

Legal and Compliance Checks

Lenders will verify that the business is properly registered, holds any required licenses, and is not subject to outstanding legal judgments or liens. This step often involves a simple background check rather than an exhaustive audit.

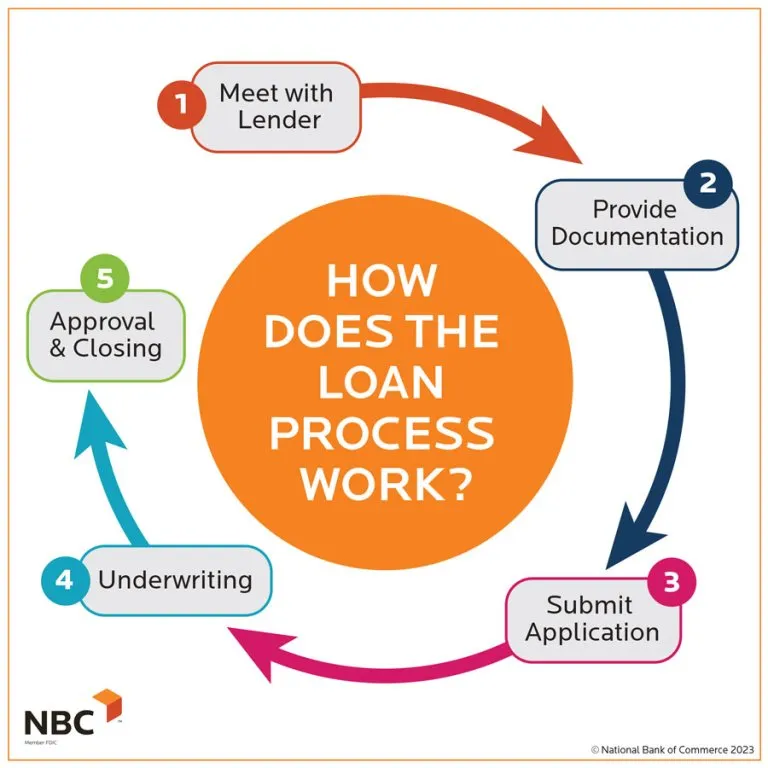

The Application Process: Step‑by‑Step Guide

Applying for a business loan based on bank statements involves several sequential actions. Below is a factual outline of the typical workflow.

1. Gather Required Documentation

- 12–24 months of bank statements (PDF or CSV format)

- Business identification documents (EIN, articles of incorporation)

- Personal identification for owners (government‑issued ID)

- Optional: Recent tax returns or a brief profit‑and‑loss summary

2. Complete the Online Application

Most lenders provide a secure portal where applicants upload statements and answer a series of questions about business operations, purpose of the loan, and anticipated repayment schedule.

3. Automated Data Extraction

Advanced algorithms parse transaction data, categorize income versus expenses, and calculate key metrics such as average monthly cash‑inflow, net cash flow, and expense ratios.

4. Manual Review (if needed)

For borderline cases, a loan officer may conduct a manual review, reaching out for clarifications on unusual spikes or large outflows.

5. Decision and Funding

Within 24–72 hours of submission, most lenders provide a decision. Approved loans are funded via ACH transfer directly into the business’s designated account.

Cost Structure: Interest Rates, Fees, and Repayment Terms

Statement‑based loans are not free of cost. Understanding the pricing model is essential for budgeting and assessing total loan expense.

Interest Rates

Rates typically range from 8% to 20% APR, reflecting the lender’s risk assessment and the borrower’s cash‑flow profile. Higher average monthly deposits often translate to lower rates.

Origination and Service Fees

Many lenders charge a one‑time origination fee (1%–5% of the loan amount) and may levy a monthly service fee for account maintenance. These fees are disclosed upfront in the loan agreement.

Repayment Schedules

Repayment terms can be flexible, with options for weekly, bi‑weekly, or monthly installments. Some lenders tie repayment amounts to a percentage of monthly deposits, creating a variable repayment model that aligns with cash flow.

Advantages and Potential Drawbacks

Like any financing solution, statement‑based loans present both benefits and challenges. A balanced view helps businesses decide if this product matches their strategic goals.

Advantages

- Speed: Rapid approval and funding support time‑sensitive opportunities.

- Accessibility: Lower reliance on credit scores opens doors for newer enterprises.

- Transparency: Lenders evaluate actual cash movement, reducing guesswork.

- Flexibility: Variable repayment structures can ease pressure during low‑revenue months.

Potential Drawbacks

- Higher Cost: Interest rates are often above those of traditional term loans.

- Cash‑flow Dependency: A temporary dip in deposits can affect repayment capacity.

- Limited Loan Amounts: Funding caps are usually tied to average monthly cash flow, restricting large capital projects.

Practical Tips to Strengthen Your Application

Even though the process is streamlined, applicants can improve their odds by adhering to best practices.

Maintain Clean Banking Records

Regularly reconcile accounts, eliminate personal transactions from business accounts, and ensure that deposits are properly categorized. Clean records simplify data extraction and reduce the likelihood of manual review delays.

Show Consistent Revenue Growth

Demonstrating a upward trend in monthly deposits signals a healthy trajectory, which can lead to better rates. If growth is seasonal, consider providing a brief narrative explaining the pattern.

Prepare a concise purpose statement

Clearly articulate how the loan will be used and how it will contribute to revenue generation or cost reduction. Lenders appreciate a direct link between funding and anticipated cash‑flow improvement.

Leverage complementary banking products

Businesses that already hold a BMO Small Business Account or similar relationship may receive preferential terms, as existing account activity offers additional data points for risk assessment.

Consider a pilot run

If possible, apply for a smaller loan amount initially to establish a repayment track record. Successful repayment can pave the way for larger funding in future cycles.

Comparing Statement‑Based Loans with Traditional Options

To put the product in context, a side‑by‑side comparison with conventional term loans and lines of credit highlights key differentiators.

| Feature | Statement‑Based Loan | Traditional Term Loan | Line of Credit |

|---|---|---|---|

| Primary Evaluation Metric | Bank statement cash flow | Credit score, collateral, financial statements | Credit score, collateral, financial statements |

| Typical Approval Time | 1–3 days | 1–4 weeks | 1–2 weeks |

| Interest Rate Range | 8%–20% APR | 4%–12% APR | 6%–18% APR |

| Loan Amount Ceiling | Up to 25× average monthly deposits | Based on collateral and cash flow | Revolving limit set by lender |

| Repayment Flexibility | Variable, often % of deposits | Fixed schedule | Draw‑and‑repay as needed |

Regulatory Landscape and Consumer Protections

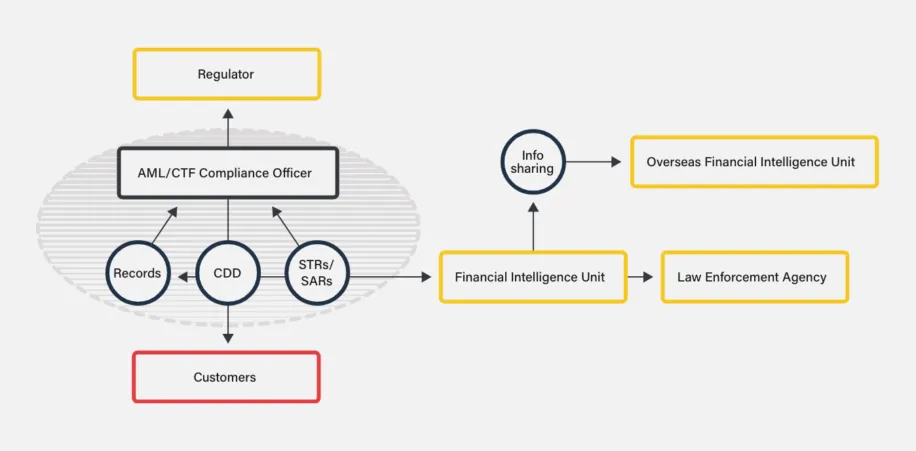

Business lending, including statement‑driven products, falls under the purview of federal and state regulations designed to protect borrowers from predatory practices. Key statutes include the Truth in Lending Act (TILA), which mandates clear disclosure of APR, fees, and repayment terms, and the Fair Credit Reporting Act (FCRA), which governs the use of credit information.

Lenders offering statement‑based loans must also comply with anti‑money‑laundering (AML) requirements, conducting due‑diligence checks on transaction patterns to detect illicit activity. Borrowers should verify that the lender is registered with the appropriate state banking authority or is a member of a reputable financing network.

Future Trends: Automation and AI in Statement Analysis

Advancements in artificial intelligence are reshaping how lenders process bank statements. Machine‑learning models can detect subtle cash‑flow trends, forecast future deposits, and flag anomalies faster than manual review. As these technologies mature, we can expect even shorter approval cycles and more personalized pricing based on nuanced risk profiles.

Moreover, integration with accounting platforms such as QuickBooks or Xero enables seamless data transfer, reducing the burden on business owners to manually export statements. This convergence of fintech and traditional banking promises to expand the accessibility of statement‑based loans to a broader segment of the entrepreneurial population.

In summary, a business loan based on bank statements offers a pragmatic financing avenue for companies that prioritize cash‑flow visibility over conventional credit metrics. By understanding eligibility requirements, preparing clean banking records, and aligning loan purpose with revenue‑generating activities, businesses can leverage this product to sustain growth and navigate short‑term financial challenges. As the lending ecosystem continues to evolve, statement‑driven loans are likely to become an integral component of the broader financing toolkit.