North Country Savings Bank (NCSB) has been a cornerstone of community banking in the Upper Midwest for decades, offering a range of deposit products designed to meet the needs of both individual savers and small businesses. Among these offerings, certificates of deposit (CDs) remain a popular choice for customers seeking a predictable, low‑risk way to grow their savings. In this article, we dive deep into the current CD rates at North Country Savings Bank, explore the factors that shape those rates, and provide actionable guidance for anyone looking to make the most of a CD investment.

Understanding the mechanics of CD rates is essential before committing funds. A CD is essentially a time‑bound deposit where the bank agrees to pay a fixed interest rate for a predetermined term, ranging from a few months to several years. The appeal lies in its safety—most CDs are insured by the FDIC up to $250,000 per depositor per institution—combined with the certainty of a locked‑in return. Yet, not all CDs are created equal; rates can vary dramatically based on term length, deposit size, and the bank’s strategic goals.

Current North Country Savings Bank CD Rate Landscape

As of the latest quarterly update, North Country Savings Bank offers a tiered CD rate structure that aligns with industry trends while reflecting the bank’s regional focus. Below is a snapshot of the rates available to new customers:

- 3‑Month CD: 0.55% APY

- 6‑Month CD: 0.65% APY

- 12‑Month CD: 0.85% APY

- 24‑Month CD: 1.10% APY

- 36‑Month CD: 1.25% APY

- 48‑Month CD: 1.40% APY

- 60‑Month CD: 1.55% APY

These rates are competitive for a community bank operating in a low‑interest environment, especially when contrasted with the national average for similarly sized institutions. However, they sit slightly below the yields offered by some online‑only banks, which can push the upper 2% range for longer terms. The key advantage with NCSB, though, is its strong local presence and personalized service, which often translates into flexible rollover options and lower minimum deposit requirements.

How North Country Savings Bank Sets Its CD Rates

CD rates are not set in a vacuum. Several macro‑ and micro‑level factors converge to determine the exact APY a bank offers:

Federal Reserve Policy

The Federal Reserve’s target federal funds rate influences the entire interest‑rate ecosystem. When the Fed raises rates, banks typically respond by increasing CD yields to stay attractive to depositors. Conversely, a dovish stance leads to tighter rates. North Country Savings Bank closely monitors Fed announcements, adjusting its CD ladder accordingly to balance liquidity needs with competitive positioning.

Liquidity Management

Deposits are a bank’s lifeblood. By offering a variety of CD terms, NCSB can smooth out cash flow and align asset‑liability matching. Longer‑term CDs provide a stable funding source, allowing the bank to pursue longer‑duration loans such as mortgages. This strategic need often explains why the 48‑ and 60‑month CDs carry a premium over shorter terms.

Competitive Landscape

While NCSB enjoys a loyal regional customer base, it still competes with national chains and fintech platforms. The bank regularly conducts market research, benchmarking its rates against peers like money market offerings from larger banks and adjusting its CD rates to avoid erosion of deposit share.

Deposit Volume and Cost of Funds

When a bank experiences a surge in deposits—perhaps due to a local economic boom—it may lower CD rates because the cost of acquiring additional funds drops. Conversely, in tighter markets, the bank may need to raise rates to attract new capital.

Key Features of North Country Savings Bank CDs

Beyond the headline APY, several attributes make NCSB’s CD products noteworthy for both novice savers and seasoned investors.

- Low Minimum Deposits: Most terms start at $1,000, with the 3‑month CD available for as little as $500, lowering the entry barrier.

- FDIC Insurance: All CDs are fully insured up to the standard $250,000 limit, providing peace of mind.

- Automatic Renewal Options: Upon maturity, CDs can automatically renew at the prevailing rate, or customers can opt for a cash payout.

- Early Withdrawal Penalties: While penalties apply (typically 3 months’ interest for terms under one year, and 6 months’ interest for longer terms), they are clearly disclosed, allowing customers to weigh liquidity needs.

- Joint and Trust Account Compatibility: NCSB permits CDs to be opened under joint ownership or trust arrangements, adding flexibility for estate planning.

Strategic Tips for Maximizing CD Returns at NCSB

To extract the most value from a CD investment, consider the following proven strategies, each grounded in sound financial planning principles.

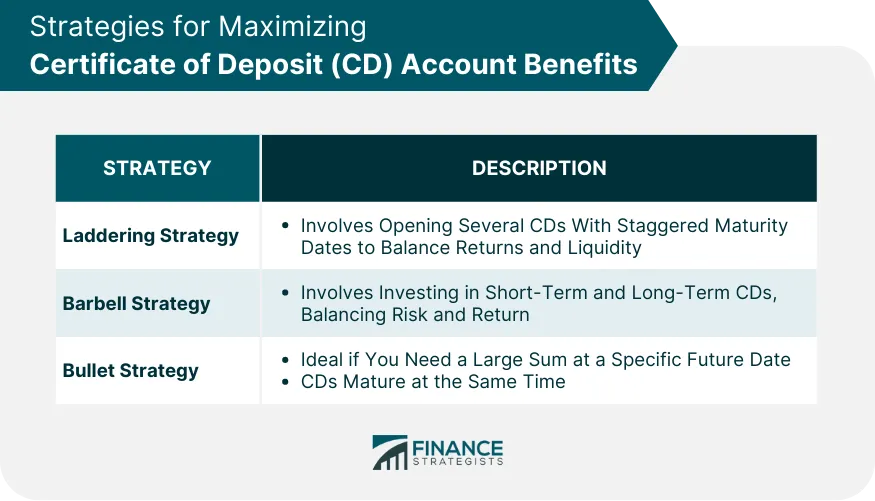

1. Ladder Your CDs

Laddering involves spreading your investment across multiple CD terms—say, a 12‑month, a 24‑month, and a 36‑month CD. This approach offers a blend of liquidity and higher yields, ensuring that a portion of your money becomes available periodically without sacrificing the higher rates associated with longer terms.

2. Take Advantage of Promotional Rates

North Country Savings Bank occasionally runs limited‑time promotions, especially for new customers or for deposits exceeding $10,000. Keep an eye on the bank’s website or sign up for alerts to capture these short‑lived boosts.

3. Align CD Terms with Financial Goals

If you’re saving for a specific milestone—such as a down payment on a house in two years—choose a CD that matches that horizon. This minimizes the need to break the CD early and incur penalties.

4. Reinvest Matured CDs Promptly

When a CD matures, compare the prevailing rate to the rate you earned. If the market has moved favorably, reinvest the principal into a new, higher‑yielding CD. This “rollover” technique can compound returns over time.

5. Consider Tax Implications

Interest earned on CDs is taxable as ordinary income. If you’re in a high tax bracket, you might explore holding CDs within a tax‑advantaged account, such as an IRA, provided the bank allows it. Consult a tax professional to assess the impact.

Comparing NCSB CD Rates to National Averages

To gauge the competitiveness of NCSB’s offerings, let’s juxtapose its rates with the latest national averages reported by the FDIC (as of Q4 2025):

- 3‑Month CD: NCSB 0.55% vs. national average 0.40%

- 12‑Month CD: NCSB 0.85% vs. national average 0.70%

- 36‑Month CD: NCSB 1.25% vs. national average 1.10%

- 60‑Month CD: NCSB 1.55% vs. national average 1.30%

While NCSB trails some online‑only banks that push rates into the 2% range for 5‑year CDs, it consistently outperforms many regional competitors and the overall market median. This positioning reflects the bank’s balance between competitive pricing and the added value of face‑to‑face service.

Potential Risks and Considerations

No investment is without risk, even a seemingly safe CD. Here are a few cautionary points to keep in mind:

- Interest Rate Risk: If the market rate spikes after you lock in a CD, you could be stuck with a lower yield until maturity.

- Liquidity Constraints: Early withdrawal penalties can erode a portion of the earned interest, making CDs less suitable for emergency funds.

- Inflation Impact: In periods of high inflation, real returns (interest minus inflation) may turn negative, diminishing purchasing power.

Balancing CDs with other instruments—such as high‑yield savings accounts, money market funds, or short‑term Treasury securities—can mitigate these concerns. For a deeper dive into how money‑market rates compare, see the article Why s& t Bank Money Market Rates Matter More Than You Think – A Deep Dive.

How to Open a CD with North Country Savings Bank

Opening a CD at NCSB is straightforward. Follow these steps to ensure a smooth experience:

- Gather Documentation: Valid ID (driver’s license or passport), Social Security number, and proof of address.

- Choose the Term and Amount: Decide on the CD length that aligns with your financial timeline and the amount you wish to lock in.

- Complete the Application: You can apply online through the bank’s portal, over the phone, or in person at a local branch.

- Fund the CD: Transfer the deposit via electronic funds transfer (EFT), wire, or cash/cheque at a branch.

- Set Up Automatic Renewal (Optional): Indicate whether you want the CD to renew automatically at the prevailing rate.

For customers interested in broader banking products, the bank also offers high‑yield savings accounts—details of which are explored in Unlock the Secrets of Cit Bank’s High‑Yield Savings Rate – What You Need to Know. Understanding the full suite of options can help you allocate assets more efficiently.

In summary, North Country Savings Bank provides a solid suite of CD products that blend competitive rates with the reassurance of local, personalized banking. By employing laddering techniques, staying alert to promotional offers, and aligning CD terms with personal milestones, savers can harness these instruments to build a reliable, low‑risk component of their broader financial strategy. As interest‑rate environments evolve, keeping a pulse on NCSB’s updates and comparing them to national benchmarks will ensure that your CD investments remain both relevant and rewarding.