Student loan debt has become a defining financial challenge for many graduates. While federal loans often provide flexible repayment plans, private student loans can carry higher interest rates and fewer borrower protections. As the cost of living rises and personal finances shift, borrowers frequently wonder, can i refinance my private student loan to achieve a lower monthly payment or a better interest rate.

Refinancing a private student loan is not a decision to take lightly. It involves evaluating your credit profile, understanding the loan market, and weighing the trade‑offs between a potentially lower rate and the loss of certain federal benefits. This article walks you through the entire process, from eligibility checks to selecting the right lender, so you can answer the question with confidence.

Below, you’ll find a step‑by‑step guide that blends factual information with practical tips. Whether you are a recent graduate or a seasoned professional, the insights shared here aim to help you decide whether refinancing makes sense for your unique situation.

can i refinance my private student loan: eligibility and basics

Before you can answer the central question—can i refinance my private student loan—you must first confirm that you meet the basic eligibility criteria that most lenders require. While each lender has its own set of rules, the most common requirements include:

- Good to excellent credit score (typically 670 or higher)

- Stable employment and sufficient income to cover the new monthly payment

- At least one year of repayment history on the existing private loan

- A debt‑to‑income (DTI) ratio below 45 %

If you fall short on any of these factors, you may still be able to refinance, but you might need a co‑signer or a larger down‑payment to offset the perceived risk.

can i refinance my private student loan: interest rate considerations

The most compelling reason borrowers explore refinancing is the possibility of a lower interest rate. Private student loans can be either fixed or variable. When you ask, “can i refinance my private student loan,” the answer often hinges on the current market environment. If rates have dropped since you first took out the loan, a refinance could reduce your interest cost by 1–3 percentage points, translating into thousands of dollars saved over the life of the loan.

Here are three rate‑related factors to examine:

- Fixed vs. variable rates: Fixed rates provide predictability, while variable rates can start lower but may rise over time. Choose the structure that aligns with your risk tolerance.

- Loan term: Shorter terms usually carry lower rates but higher monthly payments. Longer terms spread the payment but may increase total interest paid.

- Lender incentives: Some lenders offer rate discounts for automatic payments or for borrowers with strong credit profiles.

By comparing the APR (annual percentage rate) of your current loan with the APRs offered by potential lenders, you can determine whether the refinance truly benefits you.

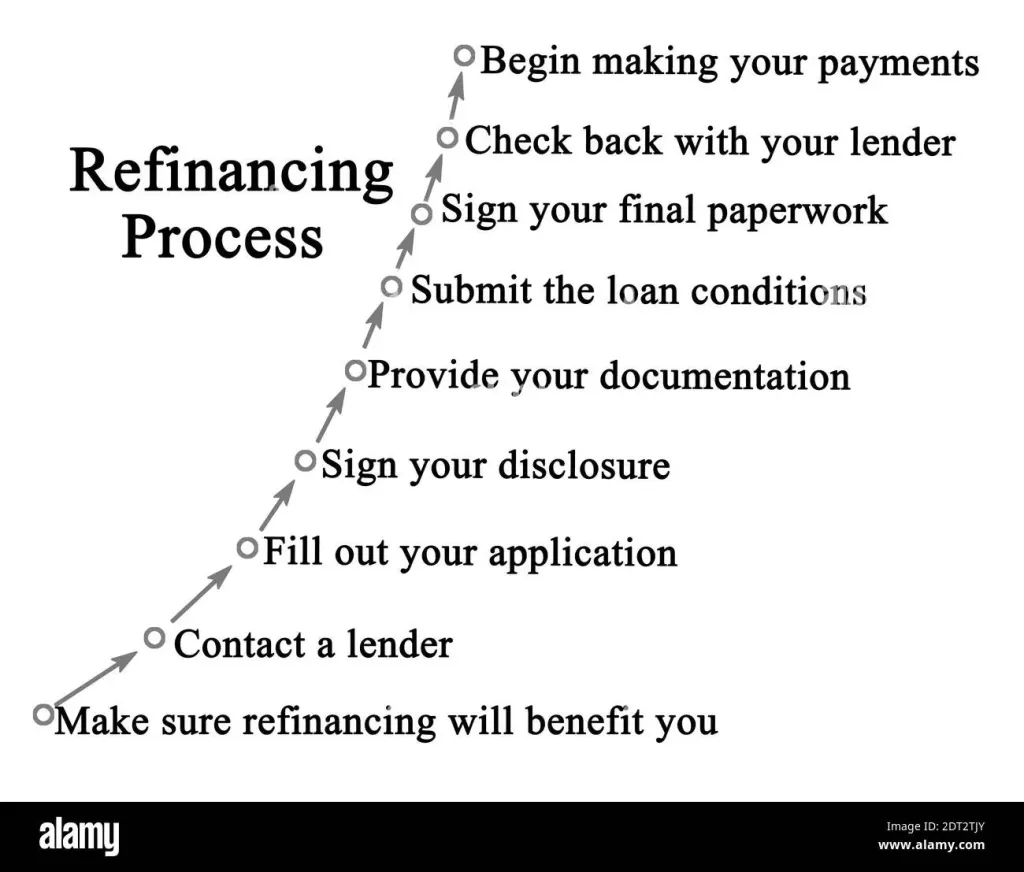

Understanding the refinance process

Once you have established that you can refinance your private student loan, the next step is to navigate the application process. The typical workflow includes:

- Gather documentation: Recent pay stubs, tax returns, existing loan statements, and proof of identity.

- Shop around: Use online comparison tools or contact lenders directly to obtain rate quotes.

- Submit an application: Most lenders allow you to apply online; you’ll input personal and financial details and authorize a credit check.

- Receive approval and terms: If approved, the lender will present the new loan terms, including interest rate, repayment period, and any fees.

- Close the old loan: The new lender pays off your existing private loan, and you begin making payments to the new lender.

It’s essential to read the fine print. Some lenders charge origination fees (typically 1–4 % of the loan amount) that can offset the savings from a lower rate. Others may have prepayment penalties on the original loan, which could affect the overall benefit.

Potential drawbacks of refinancing private student loans

While the prospect of a lower rate is attractive, asking “can i refinance my private student loan” should also involve a realistic look at possible downsides:

- Loss of federal protections: If you refinance a federal loan into a private loan, you forfeit benefits such as income‑driven repayment plans, deferment, and forgiveness options.

- Credit impact: The hard inquiry required for a refinance application can temporarily lower your credit score.

- Longer repayment horizon: Extending the loan term to reduce monthly payments can increase the total interest paid.

- Variable rates risk: If you choose a variable‑rate loan, future rate hikes could raise your payment unexpectedly.

Weigh these considerations against the potential savings before moving forward.

Strategic tips for a successful refinance

Here are practical recommendations to maximize the benefits when you answer the question, “can i refinance my private student loan?”:

Boost your credit score before applying

Pay down existing credit card balances, correct any errors on your credit report, and avoid opening new credit lines in the months leading up to your application. Even a 20‑point increase can secure a more favorable rate.

Consider a co‑signer if needed

A creditworthy co‑signer can lower the interest rate you’re offered, especially if your own credit history is limited. However, both parties become legally responsible for the loan.

Leverage automatic payment discounts

Many lenders shave off 0.25–0.5 percentage points if you set up automatic monthly debits from a checking account. This small discount can add up over the life of the loan.

Compare multiple lenders

Don’t settle for the first offer you receive. Use resources like How to Apply for Home Equity Loan Online – A Complete Guide to understand how lenders evaluate applications and what documentation they require. A broader search increases the chance of finding a competitive rate.

Read reviews and check lender reputation

Beyond rates, assess customer service, repayment flexibility, and any hidden fees. Online forums and the Better Business Bureau can provide insight into a lender’s track record.

When refinancing might not be the best choice

If you answer “can i refinance my private student loan” with a “no” after careful analysis, it could be due to one of the following scenarios:

- You rely heavily on federal loan benefits such as Public Service Loan Forgiveness (PSLF). Refinancing would eliminate eligibility.

- Your credit score is still building, and taking on a new loan could introduce a higher interest rate than your current loan.

- The existing loan has a very low fixed rate, and market rates have risen, making a refinance disadvantageous.

In these cases, focusing on accelerated repayment or income‑driven plans may be more effective than seeking a refinance.

Frequently asked questions

Can I refinance a private loan that is already in deferment?

Yes, most lenders will allow you to refinance while the loan is in deferment, but you’ll need to provide proof of the deferment status. Keep in mind that you’ll start repaying immediately once the new loan is in place.

Do I need a perfect credit score to refinance?

No. While a higher score improves your odds of getting the best rate, many lenders accept scores in the mid‑600s, especially if you have a stable income and a low debt‑to‑income ratio.

Will refinancing affect my ability to claim student loan interest deductions?

The IRS allows a deduction for interest paid on qualified student loans, regardless of whether they are federal or private. However, the deduction phases out at higher income levels, so refinancing does not change eligibility on its own.

Is it possible to refinance only a portion of my private loan?

Yes, partial refinancing—also known as “refinancing a segment”—is offered by some lenders. This strategy can lower the rate on the highest‑interest portion while keeping the remainder unchanged.

Next steps: making an informed decision

Answering the central question—can i refinance my private student loan—requires a balanced view of your financial health, the loan market, and personal goals. Start by pulling your credit report, calculating your current loan’s APR, and researching at least three reputable lenders. Use the insights from this guide to compare offers side‑by‑side, keeping an eye on hidden fees and the overall cost of the loan over its lifetime.

If the numbers show clear savings and you are comfortable with any trade‑offs, the refinance can be a powerful tool to reduce monthly stress and accelerate debt freedom. Conversely, if the analysis reveals minimal benefit or loss of crucial protections, it may be wiser to stick with your existing loan and explore other repayment strategies.

Whichever path you choose, staying informed and proactive will help you keep your student debt manageable and your financial future on track.