Do insurance still cover covid tests? That question has lingered since the pandemic’s early days and continues to puzzle many policyholders. In the first months of the outbreak, most major health insurers stepped in to eliminate out‑of‑pocket costs for diagnostic testing, recognizing the public health imperative. As vaccination rates rose and case numbers fluctuated, insurers began to reassess their commitments. This article unpacks the current state of coverage, the factors that influence it, and the steps you can take to verify your benefits.

Understanding the interplay between public health directives, federal legislation, and private insurance contracts is essential. While some insurers have rolled back universal coverage, many still offer test reimbursement under specific conditions. By examining policy language, recent regulatory updates, and real‑world examples, you can determine whether a COVID‑19 test will be billed to your insurer or your own pocket.

How Federal Policies Shaped Early Coverage

When the coronavirus first spread across the United States, the Centers for Medicare & Medicaid Services (CMS) issued emergency waivers that required private insurers to cover COVID‑19 testing without cost‑sharing. The financial strength of insurers became a point of discussion, as the waivers aimed to protect both consumers and the insurers’ fiscal health.

Key elements of the early mandates included:

- Zero copayments or deductibles for diagnostic tests ordered by a medical professional.

- Coverage extended to both PCR and rapid antigen tests.

- Inclusion of testing done at pharmacies, urgent care centers, and at‑home kits when prescribed.

These rules applied to most employer‑sponsored plans, individual policies, and Medicaid. However, the language often left room for interpretation, especially regarding “prescribed” versus “self‑initiated” testing.

Transition Period: From Mandatory Coverage to Conditional Reimbursement

By mid‑2022, the public health emergency status was lifted in many states, prompting insurers to revisit their coverage frameworks. The shift can be broken down into three main trends:

1. Retention of Core Diagnostic Coverage

Many insurers kept a baseline coverage for tests ordered by a healthcare provider. This approach aligns with standard preventive‑care clauses that many plans already contain. If your doctor orders a PCR test because you exhibit symptoms or have been exposed, the claim will likely be processed similarly to a flu test.

2. Introduction of Cost‑Sharing for Non‑Prescribed Tests

Tests that are not medically indicated—such as routine screening for travel or employment—may now be subject to copays, deductibles, or even full patient responsibility. Some plans have created separate “wellness” benefits that can be used for these scenarios, but the reimbursement rates often differ from those for medically necessary testing.

3. Expanded Use of Telehealth and At‑Home Kits

Telehealth visits surged during the pandemic, and insurers have adapted by allowing virtual orders of at‑home test kits. Coverage for these kits varies; some insurers reimburse the full cost when a telehealth provider orders the test, while others apply a reduced allowance. Understanding the specifics of your plan’s telehealth benefits is crucial.

What Your Specific Plan Might Say

Insurance contracts are notoriously dense, but there are common sections you can review to gauge COVID‑19 test coverage:

- Preventive Services Clause: Look for language referencing “screening for infectious diseases” or “CDC‑recommended testing.”

- Diagnostic Testing Section: This typically outlines coverage for tests ordered to diagnose a condition.

- Out‑of‑Network Benefits: If you use a testing site outside the insurer’s network, you may face higher cost‑sharing.

- Telehealth Provisions: Some plans have separate rules for virtual care, which can affect at‑home test reimbursement.

If you are uncertain, contacting your insurer’s member services line and asking specifically about “COVID‑19 diagnostic testing coverage” can clarify any ambiguities.

Employer‑Sponsored Plans vs. Individual Policies

Employer‑sponsored health plans often include additional wellness benefits that can be leveraged for COVID‑19 testing. For example, many large companies partnered with testing vendors to provide free or low‑cost kits directly to employees. These arrangements are usually separate from the insurance policy itself, but they can reduce out‑of‑pocket expenses.

Individual policies purchased through the health insurance marketplace or directly from insurers may have more variation. Some states have mandated that all marketplace plans cover COVID‑19 testing, while others leave it to the insurer’s discretion.

State‑Specific Regulations

State health departments sometimes impose their own requirements. For instance, California’s Department of Managed Health Care (DMHC) issued an order that all health plans must cover COVID‑19 testing without cost‑sharing, regardless of whether the test was prescribed. Conversely, in states like Texas, insurers have more leeway to impose cost‑sharing for non‑prescribed tests.

Checking your state’s insurance commissioner website can provide up‑to‑date guidance on mandated coverage.

Impact on Billing and Reimbursement

Even when a test is covered, the billing process can affect how much you owe. Common scenarios include:

- In‑Network Provider Billing: The provider submits the claim directly to the insurer, and you typically see no charge on your explanation of benefits (EOB).

- Out‑of‑Network Provider Billing: You may receive a bill for the difference between the provider’s charge and what the insurer reimburses.

- Self‑Pay Followed by Reimbursement: Some pharmacies allow you to pay up front and then file a claim for reimbursement. The success of this approach depends on the insurer’s policy language.

Understanding these pathways can prevent surprise bills.

Special Considerations for Travel and International Testing

Travel requirements frequently demand a negative COVID‑19 test within a specific time frame. Most U.S. insurers consider these tests “non‑medical” and therefore subject to full cost‑sharing. However, if you travel for work and your employer’s travel policy includes testing as a covered benefit, the cost may be reimbursed through a separate expense system rather than health insurance.

How to Maximize Your Coverage

Below are practical steps you can take to ensure you receive the most benefit from your insurance plan:

Verify Provider Network Status

Always confirm that the testing site is in‑network. Many pharmacy chains like CVS and Walgreens are widely accepted, but smaller labs may not be.

Obtain a Prescription When Possible

A documented order from a healthcare professional strengthens the case for coverage under the diagnostic testing clause.

Leverage Telehealth Services

Use your insurer’s telehealth portal to request a test. This often triggers the same coverage rules as an in‑person visit.

Document All Communications

Keep copies of emails, text messages, and EOBs. If a claim is denied, having a clear paper trail can support an appeal.

Explore Employer Wellness Programs

Check whether your employer offers free testing kits or partners with local testing sites. This can bypass insurance entirely.

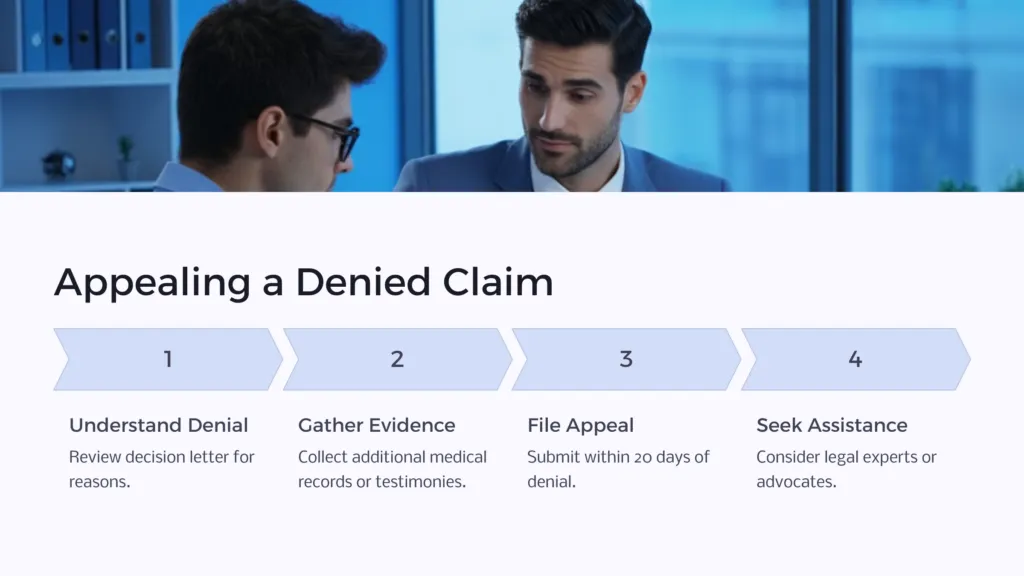

Appealing a Denied Claim

If your insurer denies coverage for a COVID‑19 test, you have the right to appeal. The typical appeal process includes:

- Reviewing the denial letter to understand the specific reason.

- Gathering supporting documentation, such as the doctor’s order, lab result, and relevant policy excerpts.

- Submitting a written appeal to the insurer’s appeals department within the timeframe indicated (often 30 days).

- If the internal appeal fails, escalating to an external review by your state’s insurance regulator.

For more guidance on navigating insurance complexities, you might find the article How to Cancel Allstate Car Insurance – The Complete Step‑by‑Step Guide useful, as it outlines how to interact with insurers and understand policy terms.

Future Outlook: Will Coverage Remain Stable?

Predicting the long‑term stance of insurers on COVID‑19 testing involves several variables:

- Public Health Trends: A resurgence of cases or the emergence of new variants could prompt renewed mandates.

- Legislative Action: Federal or state bills could codify coverage requirements, as seen with the earlier emergency waivers.

- Insurer Financial Health: Companies with strong capital reserves may be more willing to sustain broader coverage, a concept explored in the article Financial Strength and Industry Reputation.

At present, many large insurers continue to cover medically necessary tests while reserving cost‑sharing for routine screening. Monitoring your plan’s annual notice of changes will keep you informed of any adjustments.

In summary, the answer to “do insurance still cover covid tests?” is nuanced. Coverage generally persists for doctor‑ordered diagnostic tests, especially when performed in‑network or via telehealth. However, routine or travel‑related testing may now involve out‑of‑pocket costs. By reviewing your policy, confirming network status, and utilizing employer benefits, you can navigate the evolving landscape with confidence.