Table of Contents

- does rocket mortgage do va loans – Availability and Core Offerings

- Eligibility Criteria for VA Loans at Rocket Mortgage

- Benefits of Choosing Rocket Mortgage for a VA Loan

- Application Process: Step‑by‑Step Guide

- Comparing Rocket Mortgage’s VA Loans to Traditional Lenders

- Potential Drawbacks and Considerations

- Frequently Asked Questions About Rocket Mortgage VA Loans

- does rocket mortgage do va loans – What are the closing costs?

- Can I refinance an existing VA loan with Rocket Mortgage?

- Is the COE automatically retrieved, or do I need to supply it?

- Do I need a credit score of 700 to qualify?

- Real‑World Example: A Veteran’s Journey with Rocket Mortgage

- Integrating VA Loans with Broader Financial Planning

Veterans and active‑duty service members looking to purchase a home often wonder if major lenders accommodate the unique advantages of a VA loan. Among the most recognizable names in the industry, Rocket Mortgage has built a reputation for digital convenience and fast approvals. This article investigates the question “does Rocket Mortgage do VA loans,” outlining the lender’s policies, eligibility requirements, and how the process differs from traditional mortgage products.

Understanding the relationship between a well‑known online lender and the Department of Veterans Affairs (VA) loan program is essential for anyone considering this financing route. While some lenders specialize exclusively in VA mortgages, others integrate VA options into a broader portfolio of loan types. The following sections break down the specifics, providing a clear roadmap for veterans who may be contemplating Rocket Mortgage as their financing partner.

Beyond simply confirming whether Rocket Mortgage offers VA loans, we will examine the advantages of using a digital‑first platform, potential drawbacks, and the steps needed to secure approval. By the end of this guide, you will have a factual, story‑like narrative that helps you decide if Rocket Mortgage aligns with your home‑ownership goals.

does rocket mortgage do va loans – Availability and Core Offerings

Rocket Mortgage does indeed offer VA loans, positioning the product alongside conventional, FHA, and jumbo mortgages on its online platform. The company leverages its proprietary technology to streamline the application, allowing eligible veterans to start the process from a smartphone or computer. By integrating VA loan options directly into its digital workflow, Rocket Mortgage aims to reduce paperwork and accelerate underwriting, which can be especially appealing to borrowers accustomed to fast online experiences.

Eligibility Criteria for VA Loans at Rocket Mortgage

To qualify for a VA loan through Rocket Mortgage, applicants must meet the same basic eligibility standards set by the VA. These include:

- Service requirements: at least 90 days of active duty during wartime, 181 days during peacetime, or a minimum of six years in the National Guard or Reserves.

- Certificate of Eligibility (COE): a verified document proving entitlement, which Rocket Mortgage can obtain electronically on the applicant’s behalf.

- Credit standards: while the VA does not mandate a specific credit score, Rocket Mortgage typically looks for a minimum score of 620 to ensure a competitive rate.

- Debt‑to‑income (DTI) ratio: most lenders, including Rocket Mortgage, prefer a DTI of 41% or lower, though exceptions may be made based on other compensating factors.

These criteria mirror those of traditional lenders, meaning the presence of Rocket Mortgage’s online interface does not alter the fundamental VA eligibility rules. However, the convenience of uploading documents through a secure portal and receiving real‑time updates can make the verification stage feel more transparent.

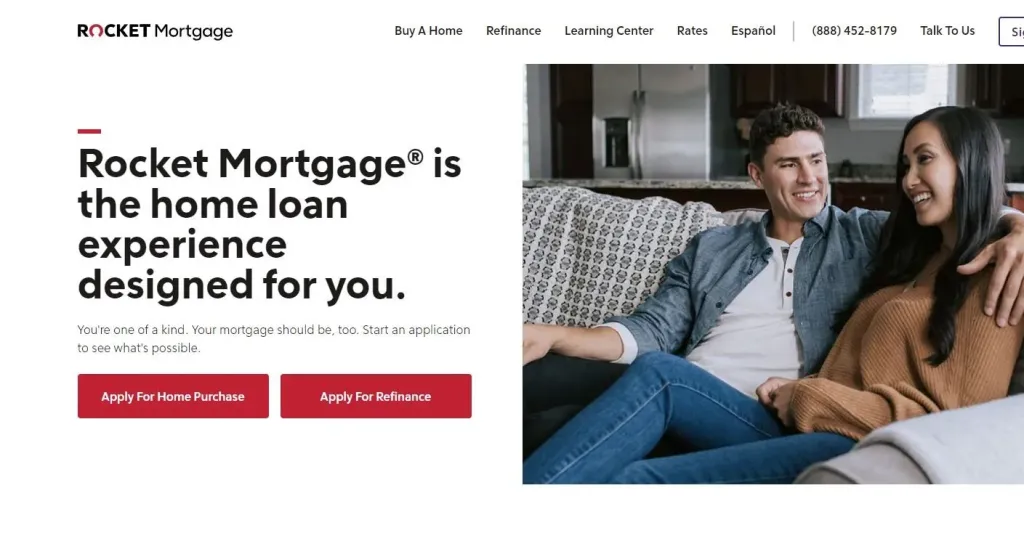

Benefits of Choosing Rocket Mortgage for a VA Loan

Veterans who elect to work with Rocket Mortgage can enjoy several distinct advantages, many of which stem from the company’s technology‑driven model:

- Speedy pre‑approval: The digital application can generate a pre‑approval decision within minutes, allowing borrowers to act quickly in competitive markets.

- Paperless process: All required documents—such as the COE, income statements, and bank statements—are uploaded securely, reducing the need for physical paperwork.

- Transparent rate shopping: Rocket Mortgage presents personalized rate quotes, enabling veterans to compare offers without contacting multiple loan officers.

- No down‑payment requirement: Like all VA loans, Rocket Mortgage’s VA product does not demand a down payment, preserving cash for moving costs or home improvements.

- Limited closing costs: The VA caps certain fees, and Rocket Mortgage often passes those savings directly to the borrower.

For those who value convenience, these features align well with the modern borrower’s expectations. Yet, it is also important to weigh potential limitations, such as the absence of a local branch for face‑to‑face consultations, which some veterans may prefer when navigating the complexities of a VA loan.

Application Process: Step‑by‑Step Guide

The journey from inquiry to closing when does Rocket Mortgage do VA loans can be divided into clear phases:

- Initial inquiry: Prospective borrowers visit Rocket Mortgage’s website or mobile app and select “VA Loan” as the desired product.

- Certificate of Eligibility retrieval: Rocket Mortgage offers an integrated COE request tool that contacts the VA’s eBenefits system on the applicant’s behalf.

- Digital application: Users complete a detailed questionnaire covering employment, income, assets, and debt. The platform automatically populates many fields using uploaded documents.

- Rate lock and underwriting: Once the application is submitted, an automated underwriting system evaluates eligibility. Borrowers can lock in an interest rate within a specified window.

- Appraisal and inspection: As with any mortgage, the property must meet VA appraisal standards. Rocket Mortgage coordinates the appraisal and ensures compliance with VA minimum property requirements.

- Closing: After underwriting approval, the closing documents are e‑signed, and the loan is funded. The entire process, from start to finish, often takes 30‑45 days, though this can vary based on market conditions.

Throughout each step, Rocket Mortgage provides real‑time status updates via email and the mobile app, which helps borrowers stay informed without the need for frequent phone calls.

Comparing Rocket Mortgage’s VA Loans to Traditional Lenders

When evaluating whether does Rocket Mortgage do VA loans, many veterans compare the digital experience to that of brick‑and‑mortar lenders. Below are a few key points of comparison:

| Feature | Rocket Mortgage | Traditional Lender |

|---|---|---|

| Application Speed | Minutes to hours | Days to weeks |

| Document Submission | Online upload, e‑sign | In‑person or mail |

| Personal Interaction | Virtual loan officers | Face‑to‑face meetings |

| Rate Transparency | Instant personalized quotes | Negotiated over calls |

| Closing Process | Electronic closing possible | Often requires physical signing |

While Rocket Mortgage’s streamlined approach may appeal to tech‑savvy veterans, some borrowers still prefer the reassurance of a local loan officer who can answer nuanced questions about VA benefits. In either case, the core loan terms—such as zero down payment and no private mortgage insurance (PMI)—remain consistent across providers.

Potential Drawbacks and Considerations

Even though does Rocket Mortgage do VA loans, there are a few factors worth noting before committing:

- Limited in‑person support: If you need hands‑on assistance, the online model may feel impersonal.

- Rate variability: While Rocket Mortgage offers competitive rates, they can fluctuate quickly. Locking in early is advisable.

- Technology reliance: Applicants with limited internet access or low digital literacy might encounter challenges navigating the portal.

- Service‑area restrictions: Some states have specific regulations that could affect the loan’s processing speed.

Understanding these nuances helps veterans make an informed decision that aligns with their comfort level and logistical needs.

Frequently Asked Questions About Rocket Mortgage VA Loans

does rocket mortgage do va loans – What are the closing costs?

The VA limits the amount veterans can be charged for certain fees, and Rocket Mortgage adheres to those caps. Typical closing costs include lender fees, appraisal fees, title insurance, and recording fees. Borrowers can negotiate some of these costs, and the lender may offer a “no‑closing‑cost” option by rolling certain fees into the loan balance.

Can I refinance an existing VA loan with Rocket Mortgage?

Yes, Rocket Mortgage offers a VA Interest Rate Reduction Refinance Loan (IRRRL), commonly known as a VA streamline refinance. This product allows eligible borrowers to lower their interest rate or switch from an adjustable‑rate mortgage to a fixed‑rate loan with minimal documentation.

Is the COE automatically retrieved, or do I need to supply it?

Rocket Mortgage’s platform can request the Certificate of Eligibility directly from the VA’s database, eliminating the need for veterans to manually obtain and upload the document. This feature speeds up the pre‑approval stage and reduces potential errors.

Do I need a credit score of 700 to qualify?

No, the VA does not set a minimum credit score. However, Rocket Mortgage typically prefers a score of 620 or higher to secure the most favorable rates. Borrowers with lower scores may still qualify but could face higher interest rates.

Real‑World Example: A Veteran’s Journey with Rocket Mortgage

Consider the case of Sergeant Alex Martinez, who served eight years in the Army and sought a home near his new civilian job. After researching lenders, he discovered that Rocket Mortgage advertised “VA loans” prominently on its website. Alex initiated the process by clicking the “VA Loan” button, entered his basic information, and within minutes received a pre‑approval estimate.

Using the integrated COE request tool, the system pulled his eligibility data from the VA’s portal. Within a day, Alex uploaded his recent pay stubs and bank statements through the secure portal. The automated underwriting engine evaluated his DTI, credit score, and employment history, approving his loan application in under 24 hours. An electronic appraisal was scheduled, and after the VA inspector confirmed the property met required standards, Alex closed the loan entirely online, signing documents with a digital signature.

Alex’s experience illustrates how does Rocket Mortgage do VA loans can translate into a swift, largely paperless transaction, especially for veterans comfortable with digital tools. Yet, his story also underscores the importance of having reliable internet access and a willingness to navigate an online platform.

Integrating VA Loans with Broader Financial Planning

Securing a VA loan through Rocket Mortgage is often one component of a larger financial strategy. Veterans may also be juggling student loans, retirement savings, or small‑business financing. Understanding how a mortgage fits into overall cash flow is crucial.

For instance, if you are also managing student debt, you might explore options like capitalized interest on student loans to gauge how future payments could impact your mortgage affordability. Similarly, refinancing high‑interest student loans (refinance student loans for a lower rate) could free up additional monthly income, making it easier to meet mortgage obligations.

By viewing the VA loan as part of a comprehensive financial picture, veterans can ensure they maintain a sustainable debt load while taking advantage of the unique benefits the VA program provides.

In summary, the answer to “does Rocket Mortgage do VA loans” is a definitive yes. The lender incorporates VA financing into its digital suite, offering veterans a modern, efficient pathway to homeownership. While the online experience may not suit everyone, the core benefits—zero down payment, limited closing costs, and competitive rates—remain intact. Prospective borrowers should evaluate their comfort with technology, compare rates with other lenders, and consider their broader financial goals before moving forward.