Table of Contents

- How to Refinance Student Loans Lower Interest Rate: Core Steps

- Refinance Student Loans Lower Interest Rate – Eligibility Checklist

- Comparing Lender Options to Refinance Student Loans Lower Interest Rate

- Key Factors When Comparing Lenders for Refinance Student Loans Lower Interest Rate

- Financial Impact of Refinancing Student Loans Lower Interest Rate

- Strategic Timing: When Is the Best Moment to Refinance Student Loans Lower Interest Rate?

- Potential Drawbacks and How to Mitigate Them

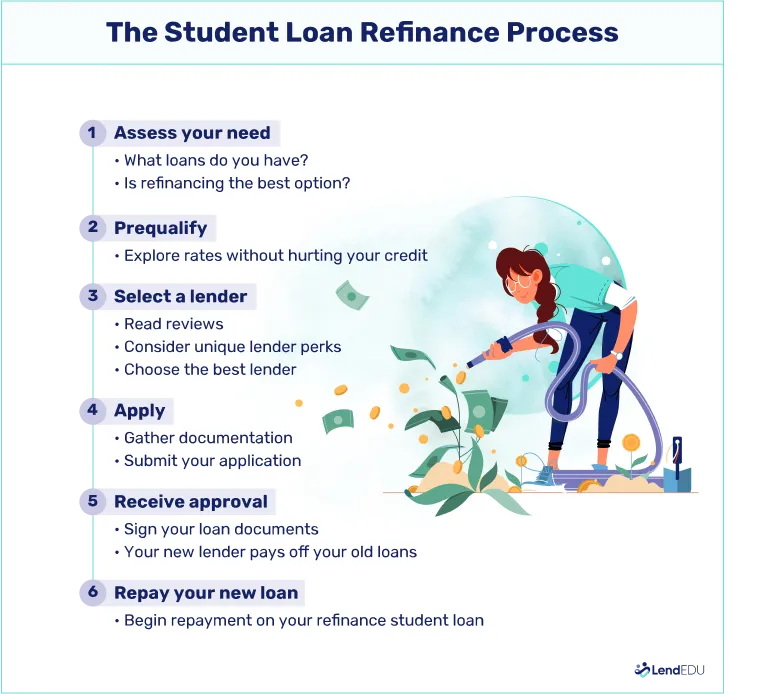

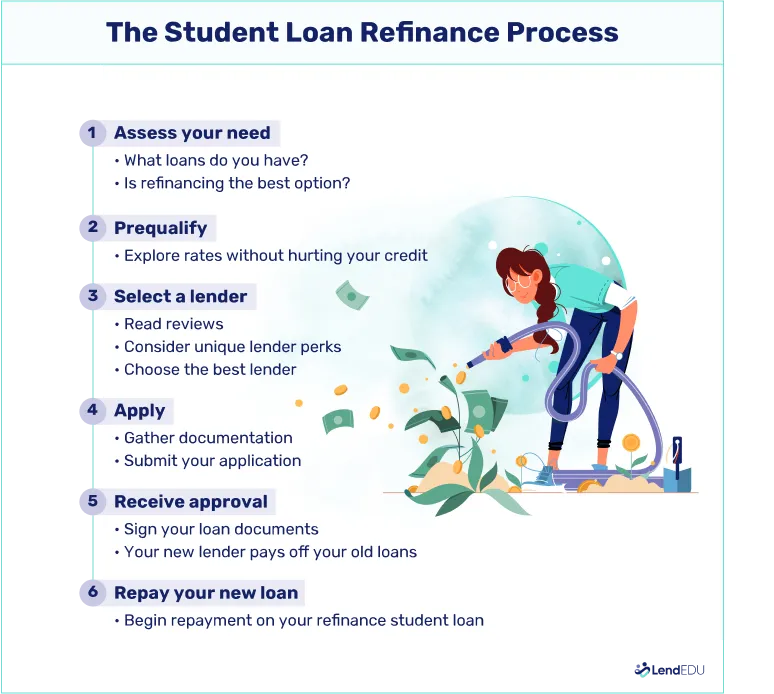

- Step‑by‑Step Guide to Refinance Student Loans Lower Interest Rate

- Additional Resources for Informed Decision‑Making

For many borrowers, the weight of a student loan balance feels permanent. The original interest rate, set years ago, may no longer reflect today’s market conditions. When that happens, a strategic move—refinancing—can turn a long‑term financial burden into a more manageable obligation. This article follows a borrower’s journey from the first question about rates to the final decision to refinance student loans lower interest rate, offering concrete steps and data‑driven insights.

Imagine a recent graduate, Maya, who accepted a 6.8 % interest rate on a private loan to finish her degree. Two years later, the same loan still carries that rate, while the average market rate for similarly‑credited borrowers has fallen to about 4 %. Maya’s monthly payment remains unchanged, but the interest she pays each year is significantly higher than it could be. By exploring refinancing, Maya hopes to lower her interest rate, shorten the repayment term, and ultimately free up cash for other goals.

This narrative mirrors the experience of millions of borrowers who discover that refinancing student loans lower interest rate is not just a buzzword but a practical financial tool. The following sections outline the process, the criteria lenders examine, and the potential pitfalls to avoid, all while keeping the focus on real‑world application.

How to Refinance Student Loans Lower Interest Rate: Core Steps

The first step toward refinancing student loans lower interest rate is to assess your current loan portfolio. Gather statements for every loan—federal, private, and any consolidation—so you know the exact balances, rates, and remaining terms. This baseline allows you to calculate the total interest you would pay if you continue with the existing schedule.

Refinance Student Loans Lower Interest Rate – Eligibility Checklist

Not every borrower qualifies automatically. Lenders typically evaluate the following factors:

- Credit score: Most lenders require a minimum score of 660; scores above 720 unlock the best rates.

- Debt‑to‑income (DTI) ratio: A DTI below 35 % signals that you can handle additional debt responsibly.

- Employment stability: Steady income, often verified by at least two years of employment, reduces perceived risk.

- Loan type: Private loans are generally eligible for refinancing; federal loans can be refinanced only after they are removed from federal benefits.

Meeting these criteria does not guarantee approval, but it positions you well for a competitive offer.

Comparing Lender Options to Refinance Student Loans Lower Interest Rate

Once you understand eligibility, the next phase is market research. Lenders differ in the interest rates they quote, the fees they charge, and the flexibility of repayment terms. A systematic comparison helps you identify the option that truly lowers your interest rate without hidden costs.

Key Factors When Comparing Lenders for Refinance Student Loans Lower Interest Rate

Use this checklist to evaluate potential lenders:

- APR vs. nominal rate: The annual percentage rate (APR) includes any origination fees or processing costs, giving a clearer picture of total cost.

- Fixed vs. variable rates: Fixed rates lock in a low rate for the life of the loan, while variable rates may start lower but can rise with market changes.

- Loan terms: Shorter terms reduce total interest but increase monthly payments; longer terms lower payments but may not achieve the lowest possible rate.

- Customer service and online tools: Responsive support and easy‑to‑use portals can simplify the refinancing experience.

For example, a borrower who qualifies for a 4.2 % fixed rate on a 10‑year term will pay considerably less interest than staying at a 6.8 % rate on a 20‑year term, even if the monthly payment is slightly higher.

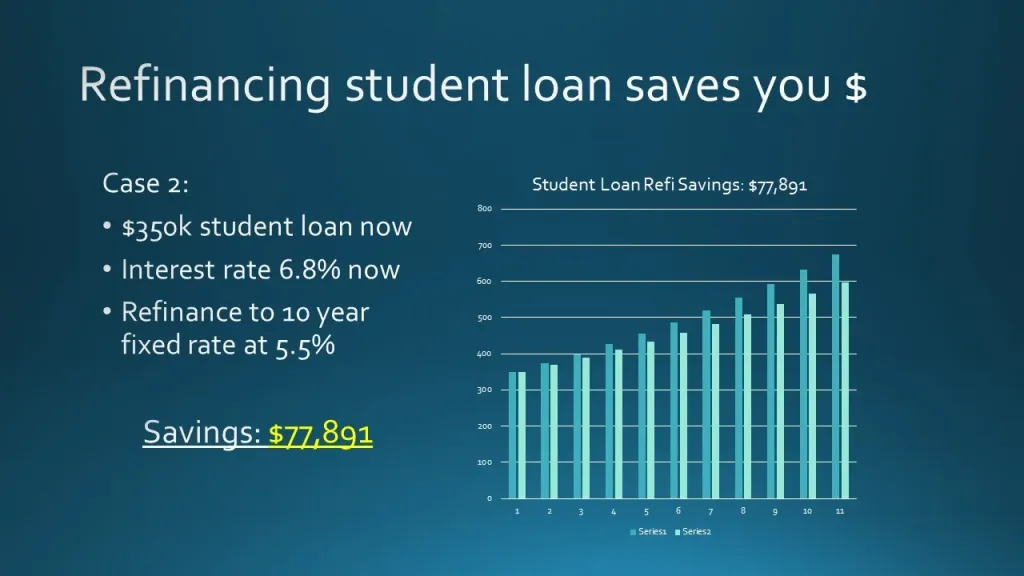

Financial Impact of Refinancing Student Loans Lower Interest Rate

Calculating the tangible benefit of refinancing is essential. Use a simple loan calculator: input your current balance, existing rate, and remaining term, then compare it with the proposed refinanced rate and term. The difference in total interest paid over the life of the loan is the primary metric.

Consider Maya’s situation: $30,000 remaining at 6.8 % over 12 years translates to roughly $13,000 in interest. If she refinances to a 4.2 % fixed rate over the same 12 years, total interest drops to about $7,500, saving $5,500. If she also shortens the term to 8 years at 4.2 %, the total interest further declines to $4,200, though her monthly payment rises. These calculations illustrate how refinancing student loans lower interest rate can align with both short‑term cash flow needs and long‑term savings goals.

Strategic Timing: When Is the Best Moment to Refinance Student Loans Lower Interest Rate?

The optimal time to refinance depends on market conditions and personal milestones. Generally, borrowers should act when:

- Market rates have fallen at least 0.5–1 % below their current loan rates.

- They have improved their credit score through consistent on‑time payments.

- They have achieved a stable employment situation, reducing the risk of future income disruption.

Additionally, avoid refinancing during periods of high market volatility if you are considering a variable‑rate product. A stable, low fixed rate often provides the most predictable path to lowering interest costs.

Potential Drawbacks and How to Mitigate Them

Refinancing student loans lower interest rate is not without trade‑offs. The most common concerns include loss of federal loan protections, such as income‑driven repayment plans, deferment, and forbearance options. Borrowers should weigh these benefits against the interest savings.

If you rely on federal protections, consider a hybrid approach: refinance only the private portion while keeping federal loans in their original program. This strategy preserves essential safeguards while still reducing the overall cost of debt.

Step‑by‑Step Guide to Refinance Student Loans Lower Interest Rate

Below is a concise roadmap that mirrors Maya’s experience from start to finish:

- Gather loan details: Compile statements for every loan, noting balances, rates, and terms.

- Check credit health: Pull a free credit report, dispute any errors, and aim for a score above 700.

- Research lenders: Use the comparison checklist to shortlist three to five reputable lenders.

- Get pre‑approval quotes: Submit basic information (income, credit, loan amounts) to receive rate offers without a hard pull.

- Run side‑by‑side calculations: Compare total interest, monthly payments, and any fees for each offer.

- Select the best offer: Choose the loan that provides the lowest effective interest rate while meeting your term preferences.

- Submit a formal application: Provide documentation (pay stubs, tax returns, ID) and authorize a hard credit inquiry.

- Close the loan: Review the final loan agreement, sign electronically, and allow the new lender to pay off existing balances.

- Update autopay: Set up automatic payments to avoid missed due dates and potentially earn rate discounts.

Following this sequence helps ensure that you truly refinance student loans lower interest rate and avoid unexpected costs.

Additional Resources for Informed Decision‑Making

To deepen your understanding of related topics, explore these guides:

- Should I Refinance My Private Student Loans? A Practical Guide – Offers a broader look at when refinancing makes sense for private debt.

- Income Limit Student Loan Interest Deduction – What You Need to Know – Explains tax implications that can further affect the net cost of borrowing.

- Will Student Loan Interest Rates Go Up? An In‑Depth Look – Provides insight into market trends that influence refinancing timing.

By reviewing these resources, borrowers can align refinancing decisions with broader financial strategies, such as tax planning and long‑term savings goals.

In summary, refinancing student loans lower interest rate is a structured process that begins with a clear inventory of existing debt, moves through careful eligibility assessment, and concludes with a data‑driven selection of a new loan product. When executed correctly, the approach can shave thousands of dollars off interest payments, shorten the repayment horizon, and restore flexibility to personal budgets. Maya’s story illustrates that, with disciplined preparation and strategic timing, the goal of a lower interest rate is attainable for many borrowers.