Table of Contents

- What Is Grace Period Student Loans and Why It Matters

- What Is Grace Period Student Loans: Key Features to Remember

- Eligibility and How the Grace Period Starts

- Interest Accrual During the Grace Period

- Choosing a Repayment Plan During the Grace Period

- Strategic Use of the Grace Period

- When the Grace Period Ends: Transition to Repayment or Forbearance

- Impact on Credit and Future Borrowing

- Special Cases: Graduate Students, Professional Programs, and Military Service

- Common Misconceptions About the Grace Period

- Tools and Resources to Manage the Grace Period

Student debt has become a central part of many graduates’ financial lives. Before the first payment hits the borrower’s bank account, however, most federal and many private loan programs grant a temporary reprieve known as a grace period. Understanding this window can make the difference between a smooth transition into repayment and a stressful scramble to cover unexpected costs.

This article explains what is grace period student loans, outlines the rules that govern it, and provides practical steps borrowers can take to use the period wisely. Whether you are a recent graduate, a parent of a student, or someone planning to return to school, the information here will help you navigate the early stages of loan repayment with confidence.

What Is Grace Period Student Loans and Why It Matters

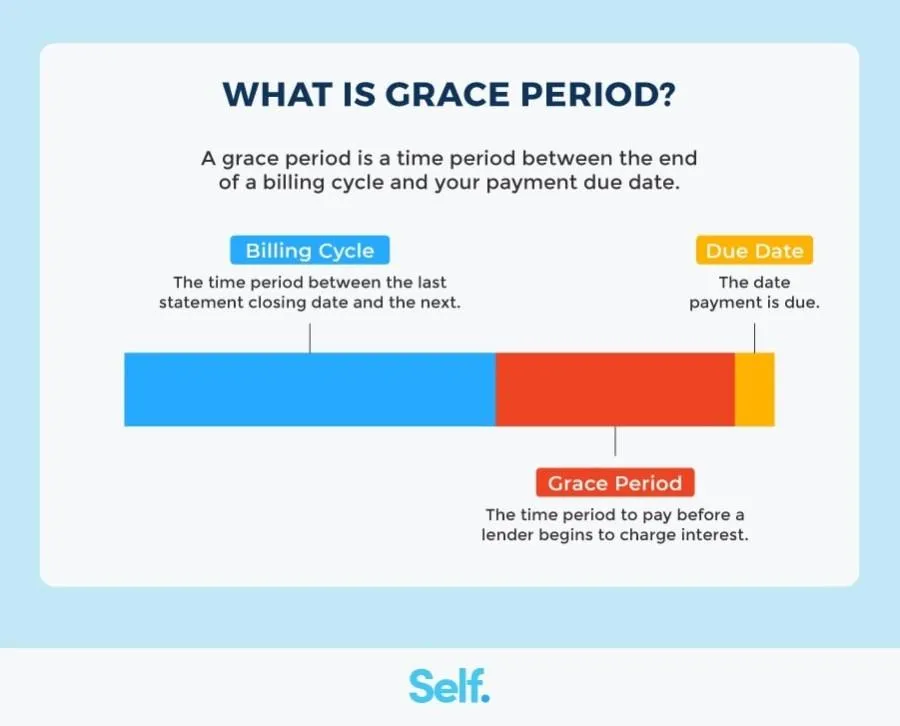

The phrase what is grace period student loans refers to the span of time after a borrower leaves school—or after the official disbursement of a loan—during which no payments are required and interest may not accrue (depending on the loan type). For most federal Direct Subsidized Loans, the grace period lasts six months, while unsubsidized loans typically begin accruing interest immediately, even during the grace period.

This pause serves several purposes. First, it gives borrowers time to locate a job, adjust to a new budget, and set up a repayment plan. Second, it prevents the immediate accumulation of large interest balances that could make the loan more expensive over time. Finally, it aligns the repayment schedule with the borrower’s cash flow, reducing the likelihood of default in the early months.

What Is Grace Period Student Loans: Key Features to Remember

- Length varies by loan type. Most federal loans grant six months; some private lenders may offer shorter or longer periods.

- Interest treatment differs. Subsidized loans stop interest during the grace period; unsubsidized loans continue to accrue interest.

- Eligibility requirements. Borrowers must be in good standing—no default or delinquency—to receive the grace period.

- Impact on repayment options. The grace period is the ideal time to choose a repayment plan that matches your income and goals.

Eligibility and How the Grace Period Starts

The grace period does not begin the moment you graduate. Instead, it starts after the loan’s “first disbursement date” or the date the school reports that you have met the “return‑to‑school” criteria. For most students, this aligns closely with graduation, but it can also begin when you drop below half‑time enrollment or transfer to another institution.

To qualify for the grace period, you must:

- Maintain at least half‑time enrollment until the end of the term.

- Not be in default on any federal student loan.

- Provide the lender with a current address and contact information.

If you fail to meet these conditions, the lender may suspend the grace period, and you could be required to start making payments immediately.

Interest Accrual During the Grace Period

One of the most common questions when readers ask what is grace period student loans is whether interest builds up. The answer depends on the loan category:

- Direct Subsidized Loans: The government pays the interest while you are in school at least half‑time, during the grace period, and during any periods of deferment.

- Direct Unsubsidized Loans: Interest accrues from the moment the loan is disbursed and continues throughout the grace period. If you do not pay the interest as it accrues, it will be capitalized—added to the principal balance—once repayment begins.

- Private Loans: Policies vary widely. Some private lenders waive interest during the grace period; others charge interest from day one. Always read the loan agreement carefully.

Capitalized interest can increase the total amount you owe and affect your monthly payment. If you can afford to pay the interest on an unsubsidized loan during the grace period, doing so can save you money in the long run.

Choosing a Repayment Plan During the Grace Period

The grace period is not only a pause; it is also a planning window. Federal borrowers have multiple repayment plans to consider, each with its own benefits:

- Standard Repayment: Fixed payments over ten years, typically the highest monthly amount but the lowest total interest.

- Graduated Repayment: Payments start low and increase every two years, useful if you anticipate income growth.

- Income‑Driven Repayment (IDR): Payments are based on a percentage of discretionary income, and any remaining balance may be forgiven after 20–25 years.

Because the grace period ends before any payments are due, you have enough time to log into the Federal Student Aid portal and compare plans. If you are unsure which option fits your situation, the Income Limit Student Loan Interest Deduction – What You Need to Know article explains how income thresholds can affect your eligibility for certain tax benefits, which may influence your repayment choice.

Strategic Use of the Grace Period

While the primary purpose of the grace period is to give borrowers breathing room, it can also be leveraged strategically:

- Set up automatic payments. Many lenders offer a 0.25% interest rate reduction for autopay, which can be arranged during the grace period.

- Pay down accrued interest. For unsubsidized loans, paying the interest before it capitalizes reduces the principal and future interest charges.

- Build an emergency fund. Instead of using all available cash to pay down the loan early, allocate part of it to a savings buffer. This can protect you from unforeseen expenses that might otherwise force you into forbearance.

- Explore refinancing options. If you have a strong credit profile, the grace period is a good time to research whether refinancing could lower your rate. The article Should I Refinance My Private Student Loans? A Practical Guide offers a step‑by‑step approach.

When the Grace Period Ends: Transition to Repayment or Forbearance

At the end of the grace period, payments become due. If you miss the first payment, the loan typically moves into a delinquent status, which can quickly lead to default if not addressed. However, if you encounter a temporary hardship, you may be eligible for forbearance options that temporarily suspend or reduce payments. Keep in mind that forbearance generally does not stop interest accrual on unsubsidized loans, and any accrued interest may be capitalized later.

It is crucial to communicate with your loan servicer before the grace period ends. They can confirm the exact date your first payment is due, provide the payment amount based on the chosen plan, and discuss any available relief programs.

Impact on Credit and Future Borrowing

How you handle the transition from grace period to repayment can affect your credit score. Timely payments for at least 12 months are reported to the credit bureaus and can improve your credit profile. Conversely, missed or late payments will be reported as delinquencies, potentially lowering your score and making future borrowing more expensive.

Maintaining a positive repayment history during the first year also opens doors to other financial products, such as mortgages or auto loans, that rely on a solid credit foundation. This is another reason why understanding what is grace period student loans is not just about avoiding immediate payments but also about setting a long‑term financial trajectory.

Special Cases: Graduate Students, Professional Programs, and Military Service

Graduate and professional students often face higher tuition costs and larger loan balances. Many of these borrowers receive a six‑month grace period similar to undergraduates, but some loan programs—especially those tied to specific schools or private lenders—may offer extended or reduced grace periods. Always verify the terms with your lender.

Members of the armed forces may qualify for the Servicemembers Civil Relief Act (SCRA), which can cap interest rates at 6% during active duty and provide additional deferment options. These benefits effectively extend the grace period for eligible borrowers.

Common Misconceptions About the Grace Period

Many borrowers misunderstand the grace period, leading to costly mistakes. Below are a few myths and the facts that correct them:

- My loan won’t accrue any interest during the grace period. This is true only for subsidized federal loans; unsubsidized and most private loans continue to accrue interest.

- I can ignore my loan until the grace period ends. While payments are not required, you must still keep the loan in good standing, respond to communications, and set up repayment preferences.

- All lenders offer the same grace period length. Private lenders set their own terms, which can be shorter or longer than the standard six months.

- Grace period automatically renews if I enroll in another term. The period restarts only when you return to at least half‑time enrollment after a break; otherwise, repayment may continue uninterrupted.

Tools and Resources to Manage the Grace Period

Effective management of the grace period often relies on using the right tools. Here are some resources to consider:

- Federal Student Aid website: Provides a personalized repayment estimator and allows you to enroll in repayment plans.

- Loan servicer portal: Most servicers have dashboards where you can set up autopay, view interest accrual, and request forbearance or deferment.

- Budgeting apps: Apps like Mint or YNAB can help you allocate funds for upcoming payments while maintaining an emergency fund.

- Financial counseling: Non‑profit credit counseling agencies can offer free advice on repayment strategies.

By combining these tools with a clear understanding of what is grace period student loans, you can avoid surprise expenses and keep your financial plan on track.

In summary, the grace period is a temporary but important phase that bridges education and repayment. Knowing exactly how long the period lasts, how interest behaves, and what actions you can take will empower you to transition smoothly into the repayment stage, protect your credit, and possibly reduce the total cost of your loans.