Table of Contents

- Why This Loan Is Not in Active Repayment: Common Triggers

- Forbearance and Deferment

- Administrative Holds or Errors

- Completion of Repayment

- Conversion to a New Repayment Plan

- Financial Implications of a Non‑Active Repayment Status

- Interest Accrual and Capitalization

- Credit Reporting

- Budget Planning

- Steps to Resolve the “Not in Active Repayment” Status

- Verify the Reason Behind the Status

- Confirm Interest Accrual Details

- Plan for Reactivation

- Address Administrative Holds Promptly

- Monitor Credit Reports

- Special Considerations for Different Types of Loans

- Student Loans

- Small‑Business Working Capital Loans

- Mortgage and Auto Loans

- Frequently Asked Questions About the Status

- What should I do if I see “this loan is not in active repayment” but haven’t requested a pause?

- Will my credit score improve because I’m not making payments?

- Can I voluntarily place my loan in a “not active repayment” status?

- Will the loan be forgiven if it stays “not in active repayment” for an extended period?

- How can I avoid unexpected interest capitalization?

When a borrower logs into their loan portal and sees the message “this loan is not in active repayment,” a cascade of questions often follows. Is the loan frozen? Has the borrower missed a payment? Or is the loan simply in a different phase of its lifecycle? Understanding the precise meaning of this status is essential for anyone navigating student loans, small‑business financing, or any other type of credit that involves periodic payments.

In many cases, the phrase appears alongside other notifications such as “in forbearance,” “deferred,” or “paused.” While each term has its own legal definition, they share a common thread: the borrower is not currently required to make a scheduled payment. The distinction matters because it influences interest accrual, credit reporting, and the borrower’s ability to plan financially.

This article walks through the mechanics behind the status “this loan is not in active repayment,” explains why it happens, outlines the implications for interest and credit, and offers practical steps borrowers can take to move forward. The discussion is grounded in factual information and avoids speculation, providing a reliable reference for anyone encountering this loan status.

Why This Loan Is Not in Active Repayment: Common Triggers

The status “this loan is not in active repayment” can arise from several legitimate scenarios. Recognizing the underlying cause helps borrowers respond appropriately.

Forbearance and Deferment

One of the most frequent reasons a loan is labeled as “not in active repayment” is that it has entered a period of forbearance or deferment. In these phases, the lender temporarily suspends the borrower’s payment obligations. While payments are paused, interest may continue to accrue, especially on unsubsidized federal loans. This distinction is critical because accrued interest can later be capitalized, increasing the principal balance.

For a deeper look at how forbearance affects student loans, see the article Why Is My Student Loans In Forbearance? Explained. Understanding the nuances of each type of pause can prevent unexpected balance growth.

Administrative Holds or Errors

Sometimes the status appears due to an administrative hold placed on the account. This could result from missing documentation, a recent change in the borrower’s address, or a discrepancy in the payment method. In such cases, the loan is technically “not in active repayment” until the issue is resolved.

Completion of Repayment

When a borrower makes the final payment on a loan, the account may temporarily show “this loan is not in active repayment” while the lender processes the closure. During this window, no further payments are required, but the borrower should verify that the loan is officially marked as “paid in full.”

Conversion to a New Repayment Plan

Borrowers who switch to income‑driven repayment plans, extended terms, or consolidation may see the status change during the transition. The original loan stops being “active” while the new terms are applied, resulting in a brief period where “this loan is not in active repayment” is displayed.

Financial Implications of a Non‑Active Repayment Status

Understanding the financial consequences of this loan status is crucial for effective money management. The most significant areas of impact are interest accrual, credit reporting, and future budgeting.

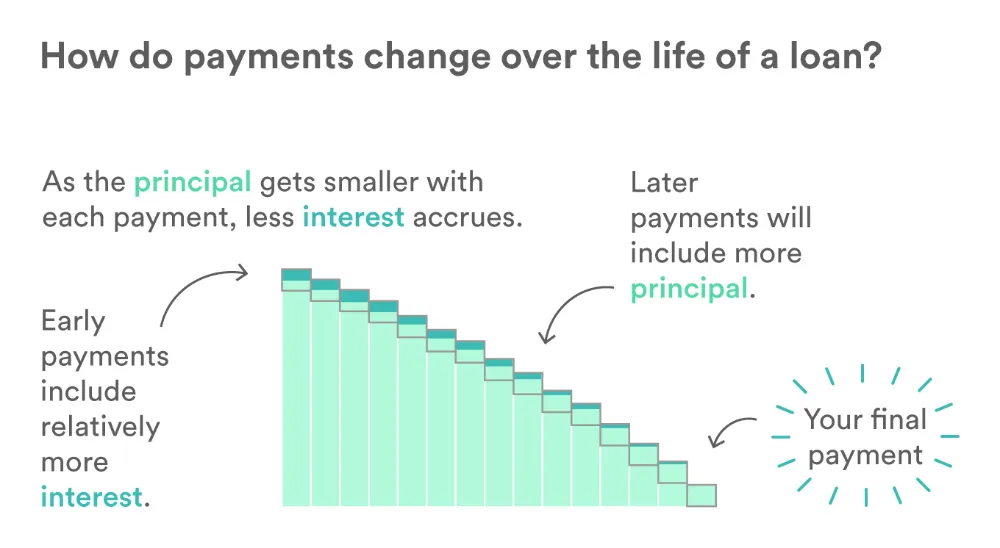

Interest Accrual and Capitalization

Even when a loan is not in active repayment, interest may continue to accumulate. For federal student loans, unsubsidized balances accrue interest daily, and the accrued amount can be capitalized—added to the principal—once the loan re‑enters an active repayment phase. This process raises the overall balance and can extend the repayment timeline.

Readers seeking a comprehensive explanation of capitalized interest may consult What Is Capitalized Interest on Student Loans – Complete Guide. Knowing when and how interest capitalizes helps borrowers anticipate changes in their payment schedule.

Credit Reporting

Lenders typically report the loan’s status to credit bureaus. When “this loan is not in active repayment,” the account may be reported as “deferred” or “in forbearance,” which does not negatively affect the credit score as long as the borrower remains compliant with the terms of the pause. However, prolonged periods without active repayment can signal financial stress to lenders reviewing credit reports for future borrowing.

Budget Planning

From a budgeting perspective, a loan that is not in active repayment temporarily frees up cash flow. Borrowers can allocate those funds toward emergency savings, debt reduction, or investment opportunities. Yet, it is prudent to set aside money for when the loan resumes active repayment, especially if interest capitalization is expected.

Steps to Resolve the “Not in Active Repayment” Status

Encountering the phrase “this loan is not in active repayment” does not automatically mean a problem, but proactive steps ensure the borrower remains in control.

Verify the Reason Behind the Status

- Log into the loan servicer’s portal and review any notifications or messages.

- Check for emails from the lender that might explain a recent forbearance approval, deferment, or administrative hold.

- If the reason is unclear, contact the lender’s customer service department for clarification.

Confirm Interest Accrual Details

Ask the servicer whether interest continues to accrue during the non‑active period. For federal loans, the Department of Education provides tools to calculate accrued interest, which can be useful for future budgeting.

Plan for Reactivation

Once the pause ends, the loan will return to an active repayment schedule. Prepare by:

- Setting aside a portion of the freed‑up cash each month to rebuild a payment cushion.

- Reviewing the new payment amount, especially if interest has capitalized.

- Exploring alternative repayment plans if the new payment exceeds your budget.

Address Administrative Holds Promptly

If the status results from missing documentation or a payment method issue, provide the required information as soon as possible. Most lenders resolve administrative holds within a few business days, allowing the loan to return to active repayment.

Monitor Credit Reports

Regularly obtain free credit reports from the major bureaus. Verify that the loan’s status is accurately reflected and that no erroneous late‑payment entries appear.

Special Considerations for Different Types of Loans

While the phrase “this loan is not in active repayment” is most commonly associated with student loans, it can appear on other credit products, such as small‑business working capital loans. Each loan category may have unique rules governing pauses.

Student Loans

Federal student loans offer numerous forbearance and deferment options, each with specific eligibility criteria. Private student loans may provide limited forbearance based on the lender’s policies. Borrowers should compare options to avoid unnecessary interest buildup.

Small‑Business Working Capital Loans

For small businesses, a “not in active repayment” status may indicate a temporary payment holiday granted during economic downturns or unforeseen cash‑flow challenges. While the loan may not require payments during this period, interest usually continues to accrue, affecting the overall cost of financing.

A detailed guide on managing such financing can be found in Working Capital Loans for Small Business: A Complete Guide. Understanding the terms helps business owners plan for the resumption of payments.

Mortgage and Auto Loans

Mortgage forbearance programs, like those introduced during the COVID‑19 pandemic, also result in a “not in active repayment” status. However, the impact on interest capitalization and long‑term repayment can differ significantly from student loans, making it essential to review loan agreements carefully.

Frequently Asked Questions About the Status

What should I do if I see “this loan is not in active repayment” but haven’t requested a pause?

Contact your loan servicer immediately. It could be a clerical error, and early resolution prevents potential issues with interest accrual or credit reporting.

Will my credit score improve because I’m not making payments?

Not directly. Credit scores reflect payment history, balances, and credit utilization. While a paused loan does not generate a missed‑payment record, the overall credit mix and outstanding balances remain unchanged.

Can I voluntarily place my loan in a “not active repayment” status?

Yes, many lenders allow borrowers to request forbearance or deferment under qualifying circumstances, such as economic hardship or enrollment in school. Review eligibility criteria before applying.

Will the loan be forgiven if it stays “not in active repayment” for an extended period?

Only specific programs, like Public Service Loan Forgiveness (PSLF) for federal student loans, provide forgiveness after a certain number of qualifying payments. Simply remaining in a non‑active status does not guarantee forgiveness.

How can I avoid unexpected interest capitalization?

Track the end date of the pause and ask the servicer whether accrued interest will be capitalized. If possible, make voluntary payments toward interest during the pause to limit balance growth.

Understanding why “this loan is not in active repayment” appears on your statement is the first step toward maintaining financial health. By verifying the cause, monitoring interest, and preparing for reactivation, borrowers can mitigate surprises and keep their repayment journey on track.

Whether you are a recent graduate, a small‑business owner, or a homeowner navigating temporary payment relief, the principles outlined here apply across loan types. Stay informed, keep open communication with your lender, and treat the pause as an opportunity to strengthen your overall financial strategy.