Table of Contents

- Will Student Loan Interest Rates Go Up? Core Economic Drivers

- Will Student Loan Interest Rates Go Up? Recent Legislative Signals

- Historical Context: How Rates Have Shifted Over Time

- Implications for Borrowers: Planning for Potential Increases

- Understanding Capitalized Interest and Its Role

- Projected Outlook for 2024‑2025

- Strategic Recommendations for Different Borrower Profiles

- Recent Graduates Entering the Workforce

- Graduate Students Pursuing Advanced Degrees

- Parents Co‑Signing Loans for Their Children

- Conclusion

Every fall, as students line up to register for classes, a familiar question circulates through campus cafés and online forums: will student loan interest rates go up? The answer is never simple, because rates are tied to a web of economic indicators, policy decisions, and legislative actions. Understanding the forces at play helps borrowers anticipate changes and plan their finances more responsibly.

Historically, student loan interest rates have mirrored the broader movements of the federal funds rate, which the Federal Reserve adjusts to manage inflation and employment. When the economy heats up, the Fed often raises rates; when growth stalls, it tends to lower them. This relationship means that any shift in monetary policy can ripple directly to the cost of borrowing for education.

In the past few years, the conversation around will student loan interest rates go up has intensified. Inflation surged, prompting the Fed to adopt a series of aggressive hikes. At the same time, policymakers debated reforms to the student loan system, adding another layer of uncertainty. The following sections break down the key drivers, recent data, and practical implications for borrowers.

Will Student Loan Interest Rates Go Up? Core Economic Drivers

To answer the central question—will student loan interest rates go up—we must first examine the macroeconomic environment. Three primary factors shape the trajectory of rates:

- Federal Reserve policy: The Fed’s target for the federal funds rate directly influences the interest rates set on new federal student loans. When the Fed raises its benchmark, loan rates typically follow suit.

- Inflation trends: Persistent inflation erodes purchasing power, compelling lenders to demand higher returns on loans to preserve real earnings.

- Legislative action: Congress has the authority to fix or adjust the maximum rates for federal student loans, regardless of market conditions.

Each of these elements can move independently, but they often intersect. For instance, a surge in inflation may trigger a Fed rate hike, which in turn creates pressure on lawmakers to reconsider the statutory caps on student loan interest.

Will Student Loan Interest Rates Go Up? Recent Legislative Signals

In the Senate, several proposals have surfaced to either freeze or lower rates for the next loan cycle. However, these bills have encountered partisan roadblocks, and none have secured final approval. The uncertainty surrounding will student loan interest rates go up remains high because the legislative calendar is crowded with competing priorities, from infrastructure spending to social safety‑net reforms.

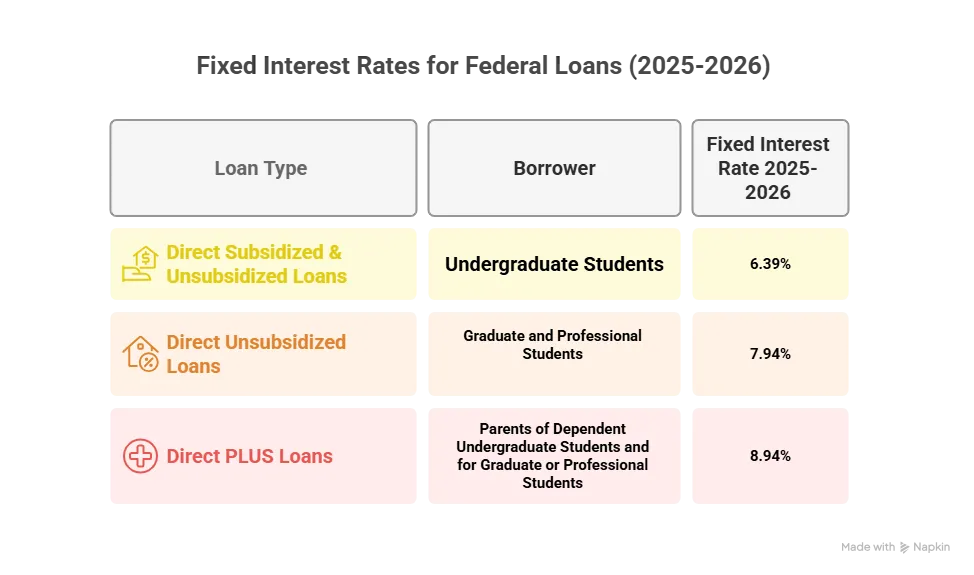

Meanwhile, the Department of Education continues to publish annual rate tables based on the 10‑year Treasury note, as mandated by law. The latest data show a modest increase compared with the previous year, suggesting that, at least in the short term, borrowers may see higher rates on newly issued loans.

Historical Context: How Rates Have Shifted Over Time

Looking back over the past two decades provides perspective on the volatility of student loan costs. In the early 2000s, rates hovered around 4–5% for undergraduate loans, reflecting a period of relatively low inflation and stable Fed policy. The 2008 financial crisis prompted a temporary dip, but the subsequent recovery and the Federal Reserve’s quantitative easing program kept rates low for several years.

After 2015, the Fed began a gradual tightening cycle, and by 2022, rates had risen to the high‑single digits. This upward trend coincided with a sharp increase in enrollment and borrowing, amplifying concerns about affordability. The pattern underscores the importance of monitoring both macro‑economic signals and policy debates when asking will student loan interest rates go up.

Implications for Borrowers: Planning for Potential Increases

Even if the exact direction of rates remains uncertain, borrowers can take concrete steps to mitigate risk. Below are practical strategies that align with the question will student loan interest rates go up and help safeguard personal finances.

- Lock in fixed‑rate loans now: Federal Direct Loans are already fixed, but private lenders often offer variable‑rate products. If you anticipate a rise, consider refinancing into a fixed rate.

- Accelerate payments: Paying more than the minimum reduces the principal balance, lowering the total interest paid even if rates increase later.

- Utilize income‑driven repayment plans: These plans adjust monthly payments based on earnings, providing a buffer against higher interest costs.

- Stay informed about policy changes: Follow updates from the Department of Education and reputable news outlets. For a deeper dive into recent trends, see Did Student Loan Interest Rates Go Up? Current Trends and Implications.

Borrowers who also run a small business should be aware that rising student loan rates can affect cash flow and credit availability. In such cases, exploring alternatives like a working capital loan for small business might be a prudent move to maintain liquidity while managing personal debt.

Understanding Capitalized Interest and Its Role

Another piece of the puzzle when evaluating will student loan interest rates go up is capitalized interest. When interest accrues on a deferred loan and later gets added to the principal balance, the overall cost of the loan rises. This mechanism can amplify the impact of any rate increase.

For a comprehensive explanation, readers may refer to What Is Capitalized Interest on Student Loans – Complete Guide. Knowing how and when interest capitalizes empowers borrowers to avoid surprise spikes in their loan balances.

Projected Outlook for 2024‑2025

Economic forecasts from major institutions suggest a cautious path ahead. The Federal Reserve’s “dot‑plot” indicates that policymakers expect at least one more rate hike by mid‑2024, followed by a potential pause. If this scenario unfolds, the 10‑year Treasury yield could edge higher, nudging the statutory student loan rates upward.

Consequently, the short‑answer to will student loan interest rates go up leans toward “yes, but modestly.” The increase is unlikely to be dramatic unless inflation resurges or a major legislative shift occurs. Borrowers should therefore prepare for a modest rise while staying vigilant for any abrupt policy changes.

Strategic Recommendations for Different Borrower Profiles

Not all borrowers face the same risk profile. Below are tailored suggestions based on typical situations.

Recent Graduates Entering the Workforce

New entrants to the labor market often have limited cash flow. To buffer against a possible increase in rates, they should prioritize establishing an emergency fund and consider making extra payments on any existing student loans, even if the loan is under an income‑driven plan.

Graduate Students Pursuing Advanced Degrees

Graduate borrowers usually take larger loans, making them more sensitive to rate changes. Refinancing after graduation, when a stable income is secured, can lock in a lower fixed rate and protect against future hikes. Monitoring the will student loan interest rates go up discussion in financial news helps time the refinance effectively.

Parents Co‑Signing Loans for Their Children

Co‑signers share liability for the debt and should be aware that a rate increase could affect their credit utilization. It is advisable to discuss repayment strategies early and explore options like co‑signer release programs once the primary borrower meets certain criteria.

Conclusion

The question of will student loan interest rates go up cannot be answered with a single, definitive “yes” or “no.” It rests on a blend of Federal Reserve actions, inflation dynamics, and legislative outcomes. Recent data suggest a modest upward trend, but the magnitude will depend on how quickly inflation eases and whether Congress enacts any rate‑freeze legislation.

For borrowers, the prudent path is to stay informed, consider locking in fixed rates where possible, and manage repayment proactively. By understanding the economic forces at play and employing sound financial habits, students and graduates can navigate potential rate changes with confidence.

Continued education on related topics, such as how capitalized interest works or where to make loan payments, will further empower borrowers to make decisions that align with their long‑term financial goals.