Table of Contents

- Are Student Loan Interest Rates Annual? Key Facts Explained

- Are Student Loan Interest Rates Annual? How Calculations Work

- Federal vs. Private Student Loan Interest Structures

- Impact of Annual Interest on Repayment Strategies

- Variable vs. Fixed Annual Rates: What to Expect

- Common Misconceptions About Annual Interest

- How to Verify Your Loan’s Annual Rate

- Refinancing: Reducing the Annual Rate

- Impact of Interest Capitalization

- Special Cases: Graduate and Professional Loans

When you take out a student loan, one of the first numbers you see is the interest rate. That figure can feel abstract, especially when you’re juggling tuition, books, and living expenses. A common question that surfaces in every loan discussion is: are student loan interest rates annual? Understanding the answer is essential because it determines how much you will ultimately pay and how you should plan your repayment strategy.

Interest rates are the cost of borrowing money, expressed as a percentage of the principal balance. For student loans, this rate can be fixed for the life of the loan or variable, adjusting with market conditions. Knowing whether that percentage applies each year—or is calculated in some other way—helps borrowers anticipate the total cost of education financing.

In the following sections, we will explore the mechanics behind student loan interest, clarify the annual nature of the rates, compare federal and private loan structures, and provide practical guidance on managing interest over the life of your loan.

Are Student Loan Interest Rates Annual? Key Facts Explained

In the United States, both federal and private student loans typically quote interest rates on an annual basis. This means the percentage you see—say, 4.53%—represents the amount of interest that accrues over a full 12‑month period, assuming the principal balance remains unchanged. However, the way that interest is applied to your loan can differ between loan types.

For federal loans, the annual interest rate is set by the government each July and remains constant for the life of the loan. The rate is expressed as an annual percentage rate (APR), although the actual cost may be slightly higher once fees are accounted for. Private lenders also usually state an annual rate, but they may offer either fixed or variable options, and the APR can include origination fees and other charges.

Even though the rate is annual, interest is typically compounded more frequently—often daily. This means that each day, the lender calculates interest based on the current outstanding balance and adds it to the loan. The daily compounding effectively spreads the annual rate across 365 days, resulting in a slightly higher effective cost than the nominal annual rate would suggest if interest were only applied once per year.

Are Student Loan Interest Rates Annual? How Calculations Work

To illustrate, imagine a $20,000 loan with a 5% annual interest rate. The daily interest rate is calculated by dividing 5% by 365, yielding approximately 0.0137% per day. If the balance stays at $20,000 for an entire year, the total interest accrued would be close to $1,000, matching the 5% annual figure. However, if you make monthly payments, the principal decreases, and the interest accrued each subsequent day will be slightly lower.

Because interest compounds daily, the effective annual rate (EAR) is a bit higher than the nominal rate. The formula for EAR is (1 + r/n)n – 1, where r is the nominal annual rate and n is the number of compounding periods per year. Using the 5% example with daily compounding (n = 365), the EAR becomes roughly 5.0127%.

Understanding this nuance helps borrowers avoid underestimating the total cost of their loans. It also underscores the importance of making payments as early and as often as possible to reduce the principal on which daily interest accrues.

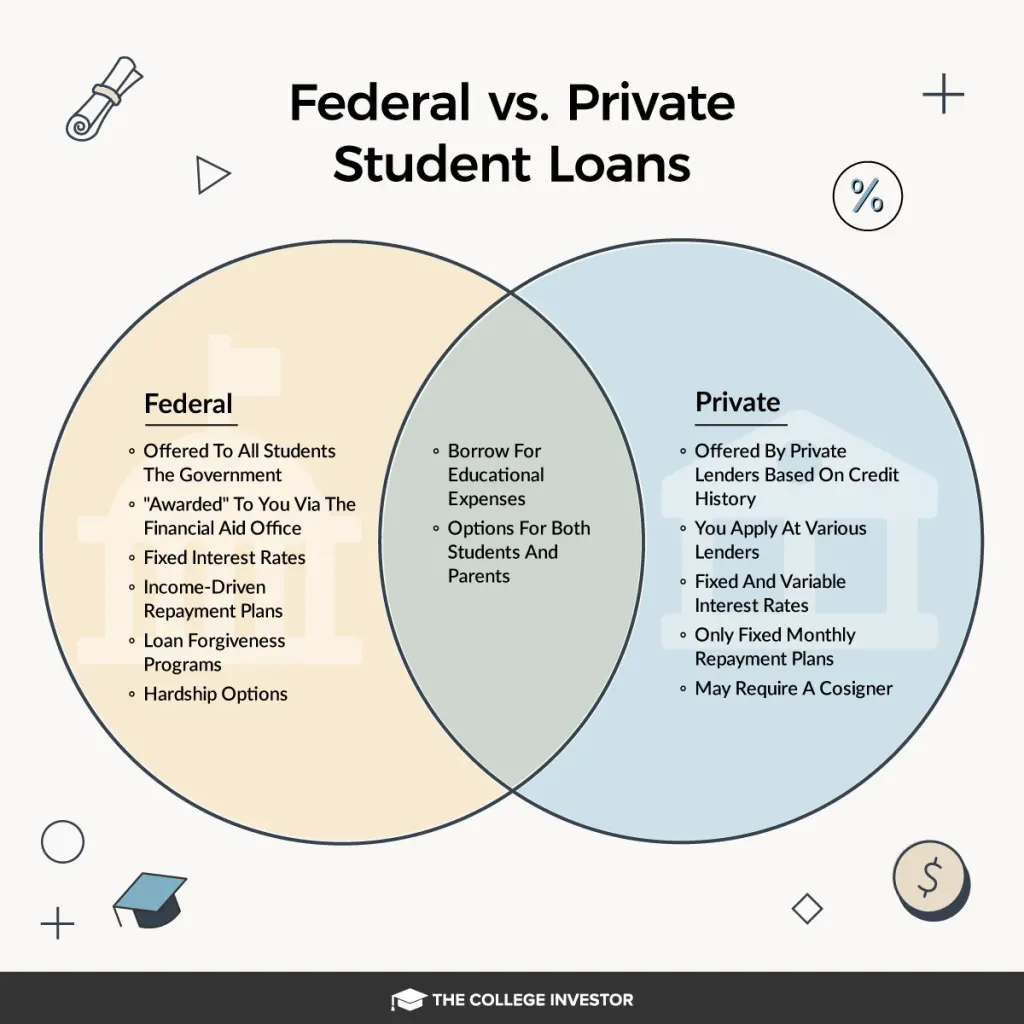

Federal vs. Private Student Loan Interest Structures

While the answer to are student loan interest rates annual is “yes” for both loan categories, the details vary.

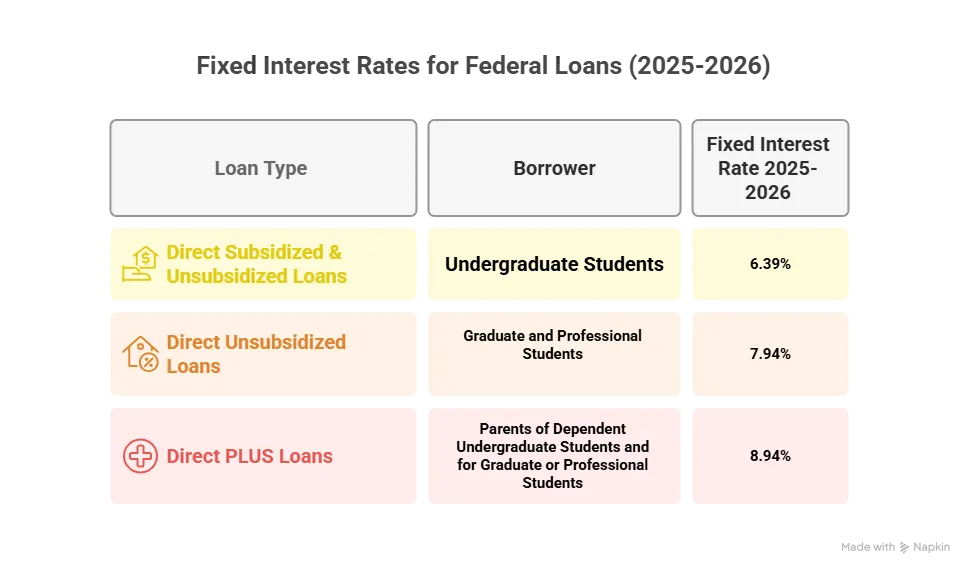

- Federal Direct Loans: Fixed annual rates set by Congress. No origination fees for most borrowers. Interest may be subsidized (the government pays it while you’re in school) or unsubsidized (you owe it from day one).

- Federal PLUS Loans: Fixed annual rates higher than Direct Loans, with a mandatory origination fee that is deducted from the disbursement.

- Private Loans: Lenders quote annual rates that can be fixed or variable. Private loans often include origination fees, and the APR may be higher than the stated rate due to these additional costs.

When evaluating a loan, look beyond the headline rate. Check the APR, fees, and whether the rate is locked for the loan’s life. This comprehensive view provides a clearer picture of the true cost.

Impact of Annual Interest on Repayment Strategies

Knowing that interest rates are annual influences how you structure repayment. Here are some strategies to minimize the interest you pay over the life of the loan:

- Pay More Than the Minimum: Extra payments directly reduce the principal, lowering the daily interest charge.

- Make Biweekly Payments: Splitting monthly payments into biweekly installments results in 26 half-payments per year—equivalent to one extra monthly payment, which speeds up principal reduction.

- Refinance When Rates Drop: If market rates fall, refinancing can lock in a lower annual rate. For guidance on timing, see How Often Can I Refinance Student Loans? A Comprehensive Guide.

- Utilize Income‑Driven Repayment (IDR): Federal borrowers can enroll in IDR plans that cap monthly payments based on income, potentially reducing the accrued interest during periods of lower earnings.

Each of these tactics leverages the fact that interest is calculated daily based on the annual rate, so any reduction in principal immediately cuts the amount of interest that can accrue.

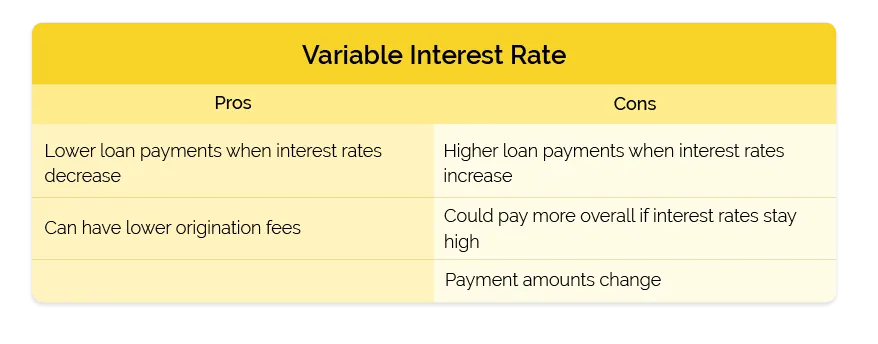

Variable vs. Fixed Annual Rates: What to Expect

Variable interest rates are tied to an index, such as the prime rate, and can fluctuate over the loan term. Although the quoted annual rate may start lower than a fixed rate, it can rise, increasing the effective annual cost. Fixed rates provide predictability; the annual percentage stays the same regardless of market changes.

Borrowers should assess their risk tolerance when deciding between variable and fixed rates. If you anticipate stable or declining market rates, a variable loan could save money. Conversely, if you prefer certainty, a fixed rate eliminates the chance of surprise increases.

Common Misconceptions About Annual Interest

Many borrowers mistakenly believe that the annual interest rate is the total amount they will pay each year, regardless of payments. In reality, the accrued interest depends on the outstanding balance and the frequency of payments. Paying off a loan early can significantly reduce the interest paid, even though the annual rate remains unchanged.

Another myth is that interest only begins after graduation. For unsubsidized federal loans and most private loans, interest accrues from the moment the funds are disbursed. If you do not pay the interest while in school, it may capitalize—meaning it is added to the principal—once repayment begins, increasing the overall cost.

How to Verify Your Loan’s Annual Rate

To confirm whether are student loan interest rates annual for your specific loan, review your loan documents or log into your loan servicer’s portal. Look for terms such as “interest rate,” “APR,” or “annual percentage rate.” If the documents list a percentage without specifying a period, it is generally understood to be annual.

For private loans, request a detailed amortization schedule that shows how interest is calculated and applied. This schedule will break down daily interest accrual and illustrate how each payment reduces the principal.

Refinancing: Reducing the Annual Rate

Refinancing can be an effective way to lower the annual interest rate on both federal and private loans, provided you qualify for a better rate. When you refinance, a new lender pays off your existing loans, and you take out a new loan with a new annual rate, often accompanied by a different term length.

Before refinancing, compare offers from multiple lenders. Pay attention not only to the advertised annual rate but also to any fees, the APR, and the loan’s repayment flexibility. For a deep dive into private loan refinancing, read Can I Refinance My Private Student Loans? A Detailed Exploration and Can I Refinance My Private Student Loan? A Complete Guide.

Impact of Interest Capitalization

Interest capitalization occurs when unpaid interest is added to the principal balance. This typically happens at the end of a grace period, during deferment, or when switching repayment plans. Once capitalized, the higher principal means that the same annual rate now generates more daily interest.

To avoid capitalization, consider paying at least the accrued interest during school or deferment periods. Even small payments can prevent the balance from growing and keep the total interest burden lower.

Special Cases: Graduate and Professional Loans

Graduate students often rely on Direct Unsubsidized Loans and PLUS Loans, both of which have higher annual rates than undergraduate loans. Additionally, professional schools (e.g., law, medicine) may require larger borrowing amounts, making the impact of the annual rate more pronounced.

Because the loan balances are larger, the daily interest accrual is significant. Graduates should explore repayment assistance programs, especially those tied to public service employment, which can offset the higher annual interest cost.

For those considering a different borrowing route, such as a home equity loan to consolidate education debt, review the article How to Apply for Home Equity Loan Online – A Complete Guide to understand how the interest rates compare.

In summary, the short answer to the central question is that student loan interest rates are indeed expressed on an annual basis. This annual figure is then broken down into daily or monthly components for actual accrual, and the way it is applied can differ between loan types, repayment plans, and lender policies. By grasping how the annual rate translates into daily interest, borrowers can make informed decisions about payment timing, refinancing, and overall loan management.

Armed with this knowledge, you can approach your student loans with a clear picture of how interest accumulates, what strategies can lower your costs, and when it might be advantageous to refinance or adjust your repayment plan. Ultimately, understanding that the interest rate is annual—and how it works in practice—empowers you to control the financial impact of your education debt.