Table of Contents

- Can I Refinance My Private Student Loans? Core Considerations

- Eligibility Checklist for Refinancing Private Student Loans

- Understanding the Financial Impact

- Key Metrics to Evaluate

- Step‑by‑Step Guide to Refinancing Private Student Loans

- Common Pitfalls and How to Avoid Them

- Potential Drawbacks of Refinancing Private Student Loans

- When Refinancing May Not Be the Best Choice

- Final Thoughts on Refinancing Your Private Student Debt

Graduating from college often feels like stepping onto a new stage, yet for many the applause is quickly muted by the echo of private student loan payments. Those loans can carry higher interest rates than their federal counterparts, and the monthly obligations can stretch budgets thin. The natural question that arises is whether you can refinance your private student loans to secure a lower rate or a more manageable repayment term.

Refinancing is not a brand‑new concept in the world of personal finance, but applying it to private student debt adds layers of nuance. Lenders evaluate creditworthiness, income stability, and even the original loan terms before offering a new agreement. Understanding these variables helps borrowers decide if refinancing is a prudent move or if staying with the original loan makes more sense.

In this article we will walk through the fundamentals of private student loan refinancing, outline the steps to assess eligibility, compare potential savings, and highlight common pitfalls. By the end, you’ll have a clear roadmap to answer the question: can i refinance my private student loans with confidence.

Can I Refinance My Private Student Loans? Core Considerations

The short answer is yes—most borrowers can refinance their private student loans, provided they meet certain criteria. However, “yes” does not guarantee “good deal.” Lenders look for a combination of strong credit scores, steady income, and a favorable debt‑to‑income (DTI) ratio. Below we break down the essential factors that influence approval.

Eligibility Checklist for Refinancing Private Student Loans

- Credit Score: A score of 700 or higher typically opens the door to the most competitive rates. Some lenders may consider borrowers with scores in the mid‑600s but will likely offer higher interest.

- Income Verification: Consistent employment or self‑employment income demonstrates repayment ability. Lenders often request recent pay stubs, tax returns, or bank statements.

- Debt‑to‑Income Ratio: Keeping your DTI below 35 % is ideal. This ratio compares your monthly debt obligations to your gross monthly income.

- Loan Amount and Term: Most lenders require a minimum balance (often $5,000) and may set maximum term lengths, usually up to 20 years.

- Co‑Signer Option: If your credit profile is borderline, adding a credit‑worthy co‑signer can improve your rate prospects.

Meeting these thresholds does not automatically secure the best rate, but it does make you a viable candidate. If you wonder whether your situation aligns with these standards, the Can I Refinance My Private Student Loan? A Complete Guide provides an interactive eligibility calculator that can give you a quick snapshot.

Understanding the Financial Impact

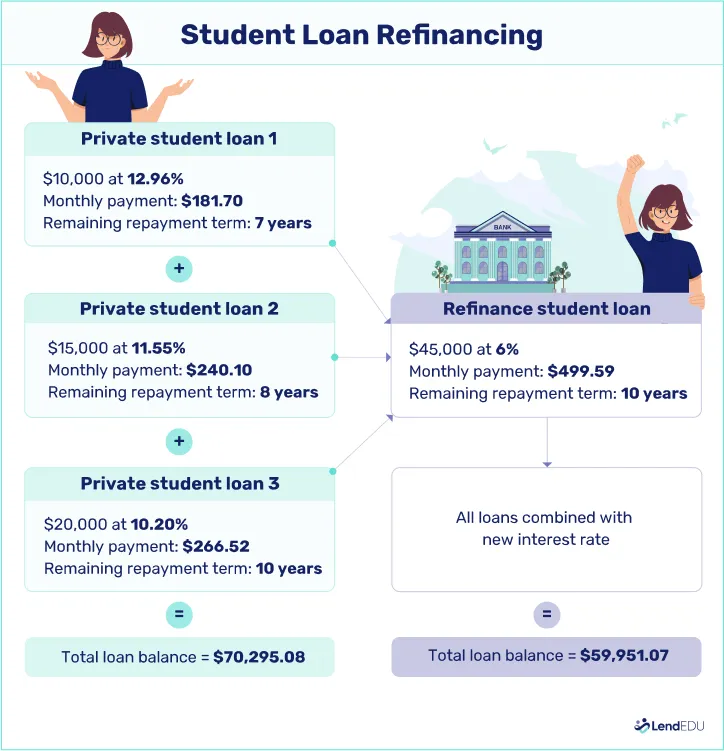

Before you decide to move forward, calculate the true cost of refinancing. While a lower nominal interest rate is appealing, the total interest paid over the life of the loan can increase if you extend the repayment period. Conversely, a shorter term can save thousands in interest but raise monthly payments.

Key Metrics to Evaluate

- Annual Percentage Rate (APR): This includes the interest rate plus any fees, offering a complete picture of the loan’s cost.

- Monthly Payment Change: Compare your current payment to the projected payment after refinancing.

- Total Interest Savings: Use an amortization schedule to see how much interest you’ll avoid over the loan’s lifespan.

- Closing Costs and Fees: Some lenders charge origination fees (typically 1‑3 % of the loan amount). Factor these into your net savings.

For many borrowers, a modest reduction in APR—say from 9.5 % to 6.8 %—combined with a slightly longer term can lower monthly obligations without sacrificing long‑term savings. However, each scenario is unique, and a thorough side‑by‑side comparison is essential.

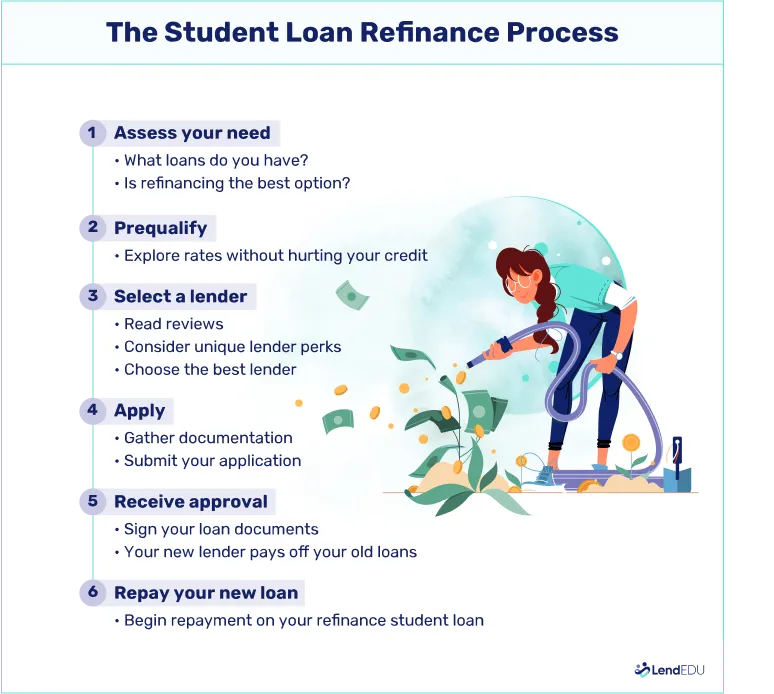

Step‑by‑Step Guide to Refinancing Private Student Loans

Now that you understand the eligibility and financial considerations, follow this structured process to determine if you can refinance your private student loans effectively.

- Gather Your Current Loan Details: List each private loan’s balance, interest rate, remaining term, and monthly payment.

- Check Your Credit Report: Obtain a free copy from AnnualCreditReport.com, dispute any errors, and note your score.

- Research Lenders: Compare at least three reputable lenders. Look for transparent rate quotes, fee structures, and borrower reviews.

- Use Pre‑Qualification Tools: Many lenders offer soft‑pull pre‑qualification that won’t affect your credit score. This gives you an idea of the rates you might qualify for.

- Calculate Potential Savings: Input the pre‑qualified rates into an online refinancing calculator, adjusting term length to see the impact on monthly payment and total interest.

- Prepare Documentation: Gather tax returns, recent pay stubs, proof of residence, and identification for the formal application.

- Submit Your Application: Complete the online form, upload documents, and authorize a hard credit inquiry if required.

- Review the Offer: Scrutinize the loan agreement for any hidden fees, prepayment penalties, or rate lock periods.

- Close the Loan: Sign the agreement, and the new lender will typically pay off your existing private loans directly.

- Set Up Automatic Payments: Many lenders provide an additional rate discount for autopay; this also helps avoid missed payments.

During step three, you might also explore other financing options that could complement or replace refinancing. For instance, a home equity loan can sometimes provide a lower rate if you own property, as detailed in our How to Apply for Home Equity Loan Online – A Complete Guide. However, remember that a home equity loan converts unsecured student debt into secured debt, introducing new risks.

Common Pitfalls and How to Avoid Them

Even well‑intentioned borrowers can stumble into traps that erode the benefits of refinancing. Awareness is the first line of defense.

Potential Drawbacks of Refinancing Private Student Loans

- Losing Federal Benefits: If you have any federal loans, refinancing them into a private loan forfeits income‑driven repayment plans, deferment, forbearance, and forgiveness options.

- Variable vs. Fixed Rates: A variable rate might start lower but can rise sharply if market conditions change. Fixed rates offer stability but may be slightly higher initially.

- Extended Repayment Terms: Lengthening the loan term reduces monthly payments but can increase total interest paid, offsetting the rate reduction.

- Hidden Fees: Origination fees, prepayment penalties, or early‑termination charges can diminish savings.

- Credit Impact: Multiple hard inquiries within a short period can temporarily lower your credit score, affecting future borrowing.

To mitigate these risks, keep a spreadsheet of all costs, read the fine print, and consider whether the trade‑off between lower monthly payments and higher total interest aligns with your financial goals. If you’re uncertain, a conversation with a certified financial planner can provide personalized insight.

When Refinancing May Not Be the Best Choice

Refinancing is a powerful tool, but it isn’t universally advantageous. Situations where you might choose to retain your existing private loans include:

- You anticipate a substantial increase in income soon (e.g., a promotion) and can handle current payments without strain.

- Your current loan has a fixed low rate that is already competitive with market offers.

- You rely on federal loan benefits for potential future hardship, and converting to private debt would remove those safety nets.

- You have a short remaining term, meaning the interest savings from refinancing would be marginal.

In these cases, focusing on accelerated principal payments or consolidating only the highest‑interest private loans might be more effective than a full refinance.

Final Thoughts on Refinancing Your Private Student Debt

The decision to refinance private student loans hinges on a blend of personal financial health, market conditions, and long‑term objectives. By carefully reviewing eligibility, calculating true costs, and weighing the pros and cons, you can answer the question “can i refinance my private student loans” with a data‑driven strategy rather than a gut feeling.

Whether you proceed with a new private loan, explore alternative financing like a home equity line, or decide to maintain your current repayment plan, the key is to stay informed and proactive. Regularly monitoring your credit, reassessing your budget, and staying aware of rate changes will ensure that you remain in control of your student debt journey.

If you found this guide useful, you might also enjoy reading Is Paying Off Student Loans Worth It? A Deep Dive, which examines the broader financial implications of eliminating student debt altogether.

Remember, refinancing is not a one‑size‑fits‑all solution, but with the right preparation it can be a valuable step toward a more manageable financial future.