Table of Contents

- Evaluating Whether It Is Worth Paying Student Loan Off

- Key Factors That Determine If It Is Worth Paying Student Loan Off

- Financial Modeling: When Paying Off Beats Investing

- Alternative Strategies to Full Repayment

- Impact on Major Life Milestones

- Psychological and Lifestyle Considerations

- Practical Steps to Decide

Student loan debt has become a defining financial burden for many graduates, shaping decisions about everything from home ownership to career changes. The question “is it worth paying student loan off” echoes across forums, financial blogs, and family dinner tables, reflecting a genuine need for clear, data‑driven guidance. While some borrowers rush to eliminate every dollar of debt, others prefer to channel cash into investments that may outpace interest rates. Understanding the trade‑offs requires a systematic look at interest costs, cash‑flow implications, and long‑term financial goals.

In this article we walk through the most relevant factors that influence the decision, present actionable tips, and compare the payoff route with common alternatives such as refinancing, investing, or leveraging loan forgiveness programs. By the end, readers will have a factual framework to answer the central question—is it worth paying student loan off—based on their own financial landscape rather than popular myths.

We also reference a comprehensive analysis of paying off student loans that delves deeper into statistical outcomes, providing a useful companion for anyone seeking more granular data.

Evaluating Whether It Is Worth Paying Student Loan Off

The first step is to calculate the true cost of the loan. This includes the nominal interest rate, the compounding frequency, and any fees attached to the loan. For example, a federal loan at 4.5% simple interest may seem modest, but when compounded monthly over a 20‑year term the effective cost can rise substantially. Compare that figure to the expected after‑tax return on alternative investments; if the loan’s effective rate exceeds the return you could realistically earn elsewhere, the answer leans toward paying it off.

Key Factors That Determine If It Is Worth Paying Student Loan Off

- Interest rate vs. investment return: Higher loan rates generally favor repayment.

- Tax considerations: Some student loan interest is tax‑deductible, lowering the net cost.

- Cash‑flow flexibility: Early repayment reduces monthly obligations, freeing cash for emergencies or other goals.

- Loan forgiveness eligibility: Public Service Loan Forgiveness (PSLF) can nullify large balances, making repayment less urgent.

- Psychological impact: Debt aversion can improve well‑being, though this is subjective.

Each factor carries weight, and the relative importance varies per individual. For a young professional with a stable high‑income trajectory, the opportunity cost of locking cash into loan payments may outweigh the interest saved. Conversely, a recent graduate with limited savings may prioritize eliminating debt to improve credit scores and reduce financial stress.

Financial Modeling: When Paying Off Beats Investing

Consider a scenario where a borrower has $30,000 in student loans at a 5% interest rate, and an after‑tax investment return of 6% from a diversified portfolio. On paper, investing seems more profitable. However, the model must incorporate risk tolerance, market volatility, and the fact that investment returns are not guaranteed. A conservative approach assumes a lower return—perhaps 3%—which would make the loan’s 5% cost more attractive to pay down.

Moreover, the timing of cash flows matters. Paying off a loan early reduces the principal faster, decreasing the amount of interest that accrues each month. This compounding effect can make a seemingly modest interest rate more burdensome over a long horizon.

Alternative Strategies to Full Repayment

Even if the analysis shows that paying the loan off is financially sensible, borrowers may still explore hybrid approaches:

- Refinancing: Securing a lower rate through a private lender can shrink the cost gap between loan interest and investment returns.

- Targeted extra payments: Directing additional cash toward the highest‑interest portion of a multi‑loan portfolio accelerates savings without sacrificing liquidity completely.

- Utilizing employer tuition assistance: Some companies offer loan repayment as a benefit, effectively providing an immediate return on any money applied to the loan.

These tactics allow borrowers to maintain a buffer for emergencies while still moving toward debt elimination. For those eligible for PSLF or other forgiveness programs, the optimal path may be to keep payments modest and focus on qualifying employment rather than aggressive payoff.

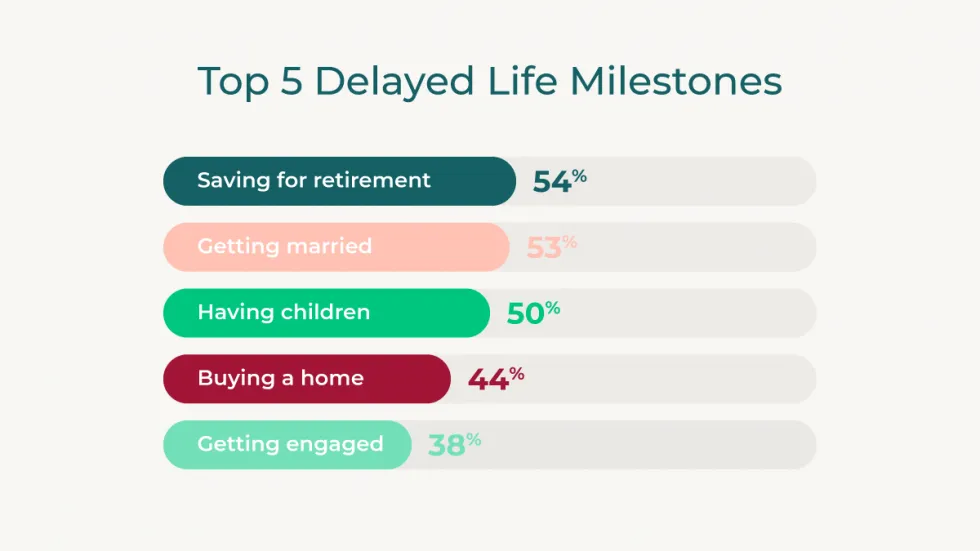

Impact on Major Life Milestones

Student loan balances often intersect with decisions about buying a home, starting a family, or launching a business. Mortgage lenders typically examine debt‑to‑income (DTI) ratios; a high DTI caused by student loan payments can limit borrowing capacity. In such cases, paying down the loan can improve eligibility for favorable mortgage rates. On the other hand, if a borrower is considering a small business venture, retaining cash for a down payment or working capital—perhaps guided by a working capital loan guide—might be more advantageous than eliminating debt outright.

Home‑ownership also introduces the possibility of leveraging home equity. A homeowner could refinance the mortgage to include student loan balances, potentially obtaining a lower combined rate. For those exploring this route, the Quicken Loans Home Equity Loan Rates – Detailed Overview provides current market data to inform the decision.

Psychological and Lifestyle Considerations

Beyond pure numbers, the question “is it worth paying student loan off” touches on personal comfort with debt. Some individuals experience significant stress while carrying any balance, affecting productivity and overall happiness. Others view debt as a tool that, if managed wisely, can free up cash for higher‑yield opportunities. While not quantifiable, these aspects should be weighed alongside financial calculations.

For those who prioritize mental peace, a systematic payment plan—such as the “snowball” method—can provide visible progress, reinforcing the belief that the loan is being conquered. This approach may be especially relevant for borrowers juggling multiple small loans with varying interest rates.

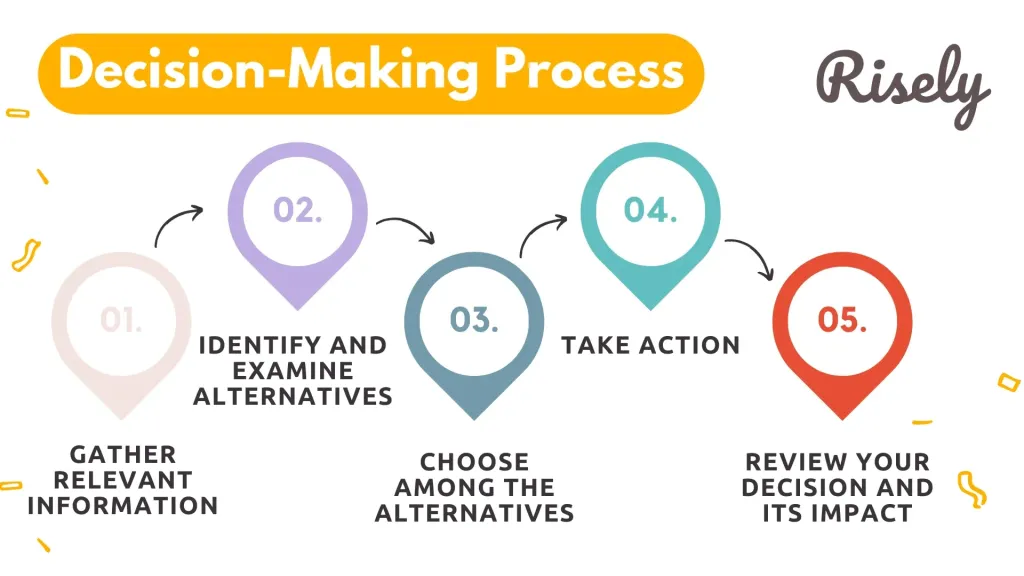

Practical Steps to Decide

To arrive at a personalized answer to “is it worth paying student loan off,” follow this step‑by‑step framework:

- Gather all loan statements and calculate the effective annual percentage rate (APR) for each.

- Estimate your after‑tax expected return on alternative investments over the same time horizon.

- Run a simple spreadsheet model comparing total interest paid versus potential investment gains, adjusting for risk.

- Consider tax deductions for student loan interest and any applicable forgiveness programs.

- Assess how loan payments affect your DTI ratio and upcoming major purchases.

- Factor in personal stress levels and financial goals, such as home ownership or entrepreneurship.

- Choose a strategy—full payoff, refinancing, targeted extra payments, or a hybrid—aligned with both numbers and lifestyle preferences.

This process transforms an abstract question into concrete data, making the final decision transparent and defensible.

In many cases, the answer to “is it worth paying student loan off” will differ from one borrower to the next. The key is to align the decision with realistic expectations about returns, risk tolerance, and life plans. By treating the loan as one component of an overall financial puzzle, rather than an isolated burden, borrowers can make choices that support long‑term stability and growth.

Whether you decide to accelerate repayment, refinance for a better rate, or invest the surplus cash, the most important outcome is a plan that you can sustain without compromising emergency savings or essential expenses. Consistency, awareness of changing market conditions, and periodic reassessment will ensure that the path you choose remains optimal as your financial situation evolves.

Ultimately, the nuanced answer to “is it worth paying student loan off” lies in the intersection of math, personal goals, and psychological comfort. By following the analytical steps outlined above and staying informed about loan options and market rates, you can confidently determine the strategy that best serves your unique circumstances.