Table of Contents

- How to Get Prequalified for a VA Loan: Core Steps

- 1. Verify Your Eligibility to Get Prequalified for a VA Loan

- 2. Gather Financial Documents to Get Prequalified for a VA Loan

- 3. Choose a Lender and Submit a Pre‑Qualification Request

- 4. Review the Lender’s Pre‑Qualification Letter

- 5. Understand the Difference Between Pre‑Qualification and Pre‑Approval

- Key Factors That Influence Your Ability to Get Prequalified for a VA Loan

- Credit Score

- Debt‑to‑Income Ratio (DTI)

- Service History and COE Status

- Employment Stability

- Common Mistakes to Avoid When You Try to Get Prequalified for a VA Loan

- Tips to Strengthen Your Pre‑Qualification Profile

- What Happens After You Get Prequalified for a VA Loan?

- Frequently Asked Questions About Getting Prequalified for a VA Loan

- Can I get pre‑qualified for a VA loan without a credit check?

- Do I need a down payment to get pre‑qualified?

- How long does a pre‑qualification letter remain valid?

- Is the VA appraisal more stringent than a conventional appraisal?

- Can I use a VA loan to purchase a condo?

For many veterans, the promise of a VA loan represents a pathway to homeownership that is both affordable and secure. Yet before any contract is signed, the first practical step is to get prequalified for a VA loan. Pre‑qualification is not a guarantee of approval, but it does give borrowers a realistic picture of the loan amount they might qualify for and signals seriousness to sellers.

Understanding the pre‑qualification process helps you avoid surprises later, positions you better in a competitive market, and can even shave weeks off the overall timeline. This article walks you through the entire journey—from gathering the right paperwork to interpreting the lender’s pre‑qualification letter—so you can move forward with confidence.

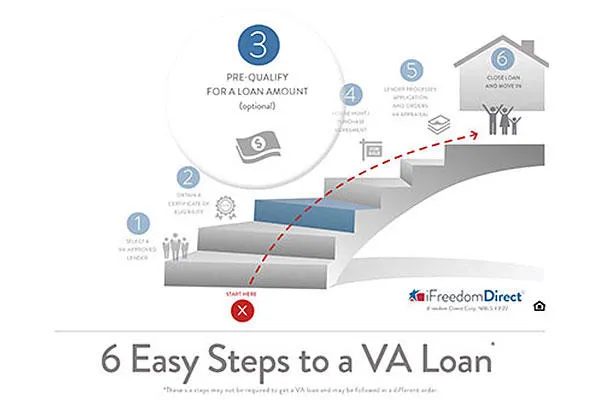

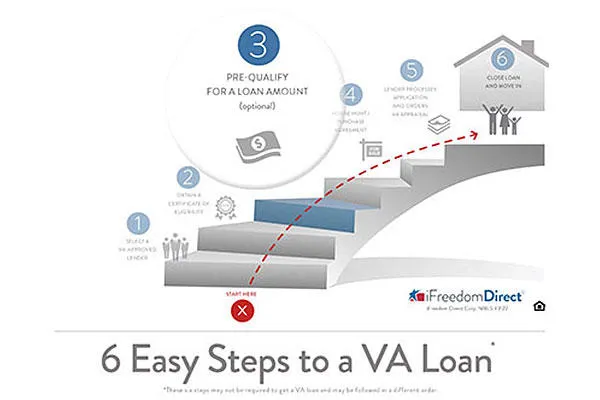

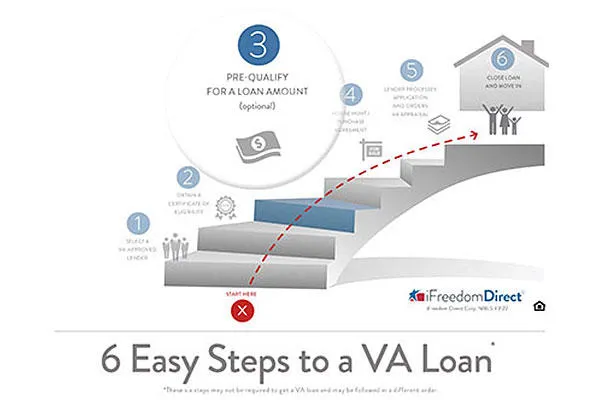

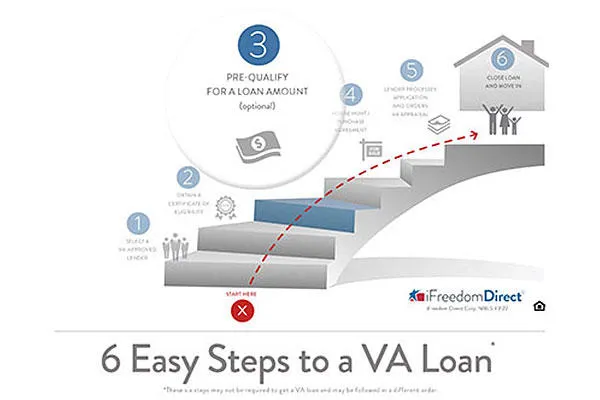

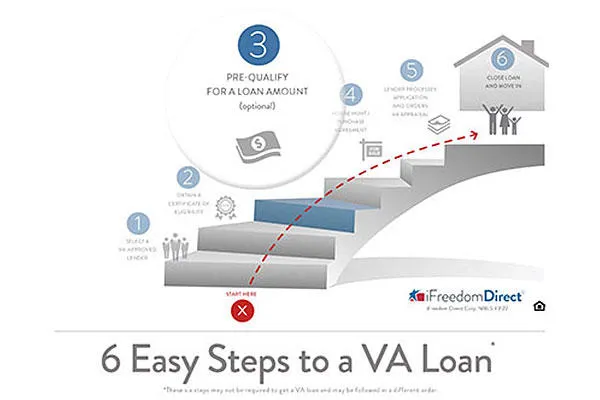

How to Get Prequalified for a VA Loan: Core Steps

The phrase “get prequalified for a VA loan” may sound bureaucratic, but the actual steps are straightforward. Below is a step‑by‑step breakdown that mirrors the process used by most lenders.

1. Verify Your Eligibility to Get Prequalified for a VA Loan

Before you approach any lender, confirm that you meet the basic VA eligibility criteria. Generally, you must be one of the following:

- Active‑duty service member who has served at least 90 consecutive days.

- Veteran with a minimum of 90 days of service and an honorable discharge.

- Spouse of a service member who died in the line of duty or as a result of a service‑connected disability.

Eligibility can be verified quickly through the VA’s online portal or by requesting a Certificate of Eligibility (COE). Without a COE, the lender cannot proceed with the pre‑qualification.

2. Gather Financial Documents to Get Prequalified for a VA Loan

Lenders need a snapshot of your financial health. The most common documents include:

- Recent pay stubs (last 30 days).

- Two years of federal tax returns.

- Bank statements for the last two months.

- Details of any existing debt, such as credit card balances, auto loans, or student loans.

Having these items ready not only speeds up the pre‑qualification but also shows lenders that you’re organized—a subtle yet valuable signal.

3. Choose a Lender and Submit a Pre‑Qualification Request

Not all lenders treat VA loans the same way. Some specialize in veteran financing and may offer lower fees or faster turnaround. Use resources like the step‑by‑step guide to VA loan prequalification to compare rates, reputation, and customer service.

When you fill out the pre‑qualification form, you’ll be asked to provide the documents listed above, along with basic personal information (address, social security number, etc.). Most lenders now allow you to upload these files securely through an online portal.

4. Review the Lender’s Pre‑Qualification Letter

Once the lender evaluates your information, they will issue a pre‑qualification letter. This document typically includes:

- The estimated loan amount you may qualify for.

- The interest rate range based on current market conditions.

- Any conditions that must be met before moving to full pre‑approval (e.g., additional documentation, a higher credit score).

Keep this letter handy when you start house hunting; it can be attached to offers to demonstrate buying power.

5. Understand the Difference Between Pre‑Qualification and Pre‑Approval

While many people use the terms interchangeably, there is a distinct difference. Pre‑qualification is a soft inquiry based on self‑reported data, whereas pre‑approval involves a hard credit check and a more thorough verification of income and assets. If you are ready to make an offer, consider moving from pre‑qualification to pre‑approval. For a deeper dive, see the article Pre Approval for a VA Home Loan – What You Need to Know.

Key Factors That Influence Your Ability to Get Prequalified for a VA Loan

The VA loan program offers generous benefits—no down payment, no private mortgage insurance, and competitive rates—but lenders still evaluate risk. Below are the primary factors that affect your pre‑qualification outcome.

Credit Score

Although the VA does not set a minimum credit score, most lenders prefer a score of 620 or higher. A higher score typically translates to better interest rates and larger loan amounts.

Debt‑to‑Income Ratio (DTI)

The DTI compares your monthly debt obligations to your gross monthly income. The VA recommends a DTI of 41% or less, but exceptions can be made if you have strong compensating factors (e.g., significant cash reserves).

Service History and COE Status

Even if you meet the basic eligibility, the type of discharge and length of service can affect the lender’s comfort level. Ensure your COE is up to date and reflects any recent changes in status.

Employment Stability

Lenders favor borrowers with at least two years of consistent employment in the same field. If you’ve recently changed jobs, be prepared to explain the transition and provide proof of continued income.

Common Mistakes to Avoid When You Try to Get Prequalified for a VA Loan

Even seasoned homebuyers can stumble during the pre‑qualification stage. Avoid these pitfalls to keep the process smooth.

- Skipping the COE request. Without a Certificate of Eligibility, the lender cannot move forward.

- Providing outdated or incomplete financial documents. This leads to delays and may result in a lower estimated loan amount.

- Ignoring credit report errors. A single erroneous late payment can lower your score and affect the pre‑qualification.

- Applying with multiple lenders simultaneously. Each hard pull can slightly reduce your credit score, making it harder to get favorable terms.

- Assuming pre‑qualification equals a guaranteed loan. Remember, it is an estimate, not a final commitment.

Tips to Strengthen Your Pre‑Qualification Profile

While you cannot control the VA’s eligibility rules, you can improve the lender’s assessment of your risk.

- Pay down high‑interest credit card balances to lower your DTI.

- Check your credit report for inaccuracies and dispute any errors.

- Save a modest emergency fund (even though VA loans don’t require PMI, lenders like to see reserves).

- Maintain steady employment for at least two years before applying.

- Consider a co‑borrower with strong credit if your own profile is borderline.

What Happens After You Get Prequalified for a VA Loan?

Once you have the pre‑qualification letter, you can begin house hunting with a realistic budget. Here’s the typical flow after that point:

- Find a property. Use the loan amount from your pre‑qualification as a guide.

- Make an offer. Attach your pre‑qualification letter to demonstrate buying power.

- Enter the formal pre‑approval stage. The lender will verify documentation, perform a hard credit pull, and issue a pre‑approval letter.

- Complete the VA appraisal. The VA must confirm that the property meets safety and value standards.

- Close the loan. After satisfying any remaining conditions, you’ll sign the mortgage documents and take ownership.

Throughout this journey, maintaining open communication with your loan officer is essential. Promptly respond to any requests for additional information, and keep your financial situation stable (avoid new large debts) until closing.

Frequently Asked Questions About Getting Prequalified for a VA Loan

Can I get pre‑qualified for a VA loan without a credit check?

Yes. Pre‑qualification typically involves a soft inquiry, which does not affect your credit score. A hard pull only occurs during the pre‑approval phase.

Do I need a down payment to get pre‑qualified?

No. One of the key benefits of the VA loan program is the ability to purchase a home with 0% down, assuming you meet the lender’s eligibility and income requirements.

How long does a pre‑qualification letter remain valid?

Most lenders issue a letter that is good for 60‑90 days. Market conditions and your financial profile can change, so you may need to refresh the pre‑qualification if you haven’t found a home within that window.

Is the VA appraisal more stringent than a conventional appraisal?

The VA appraisal focuses on both value and safety standards. It ensures the property is livable and meets minimum property requirements, which can be stricter than a standard appraisal.

Can I use a VA loan to purchase a condo?

Yes, but the condo must be VA‑approved. Check the VA’s online list of approved condominium projects before you start the buying process.

By following the steps outlined above and staying mindful of the factors that affect eligibility, you can successfully get prequalified for a VA loan and set the stage for a smooth home‑buying experience. The pre‑qualification letter is more than just a piece of paper; it’s a roadmap that helps you understand what you can afford, gives you credibility with sellers, and ultimately brings you closer to the goal of homeownership.