Table of Contents

- Quicken Loans Home Equity Loan Rates: Core Components

- How Quicken Loans Calculates Home Equity Loan Rates

- Current Quicken Loans Home Equity Loan Rates: What to Expect

- Comparing Home Equity Loan Rates with Home Equity Line of Credit (HELOC) Rates

- Eligibility Requirements for Quicken Loans Home Equity Loans

- Common Documentation Needed

- Cost Factors Beyond the Interest Rate

- Tips for Reducing the Effective Rate

- Application Process: From Quote to Funding

- Related Resources

- Future Outlook: How Market Trends May Influence Rates

- Key Takeaways for Prospective Borrowers

When homeowners consider tapping into the equity built up in their property, the first question usually centers on cost. Understanding the current Quicken Loans home equity loan rates can be the difference between a manageable monthly payment and a financial strain. This article walks through the mechanics of those rates, the factors that influence them, and practical steps borrowers can take to secure the most favorable terms.

Unlike a traditional refinance, a home equity loan provides a lump‑sum disbursement that is repaid over a fixed term with a fixed interest rate. Quicken Loans, now operating under the Rocket Mortgage brand, offers several options that cater to varying credit profiles and equity levels. By dissecting the rate structure, readers can better gauge whether a home equity loan aligns with their financial goals.

Below, we examine the key components that shape Quicken Loans home equity loan rates, compare them with alternative products, and outline a roadmap for applicants seeking to lock in the best possible rate.

Quicken Loans Home Equity Loan Rates: Core Components

Quicken Loans home equity loan rates are not set in stone; they fluctuate based on macro‑economic indicators, borrower qualifications, and loan specifics. The following elements play the most significant roles:

- Prime Rate and Treasury Yields: As with most variable‑rate products, the base index—often the U.S. Prime Rate—acts as a floor. When the Federal Reserve adjusts rates, lenders typically follow suit within a few weeks.

- Credit Score: Borrowers with scores above 740 generally receive the most competitive rates, while those in the 620‑680 range may see a modest premium.

- Loan‑to‑Value (LTV) Ratio: A lower LTV (i.e., borrowing a smaller percentage of the home’s appraised value) signals reduced risk, often resulting in lower rates.

- Loan Amount and Term: Larger loans or longer repayment periods can carry slightly higher rates due to increased exposure for the lender.

- Geographic Market: Regional cost‑of‑living differences and local real‑estate trends sometimes lead to minor rate variations across states.

How Quicken Loans Calculates Home Equity Loan Rates

Quicken Loans employs a proprietary algorithm that blends the above factors into a single APR figure presented to the borrower. The process typically follows these steps:

- Collect applicant data (credit report, income verification, property appraisal).

- Determine the eligible LTV based on existing mortgage balance and home value.

- Match the applicant’s credit tier to a base rate tier derived from current market indices.

- Apply risk adjustments for LTV, loan size, and term length.

- Present the final rate along with any applicable fees, such as origination or appraisal charges.

The resulting figure is what appears on the loan estimate as the “interest rate.” It is important to note that the APR may be slightly higher, reflecting bundled fees.

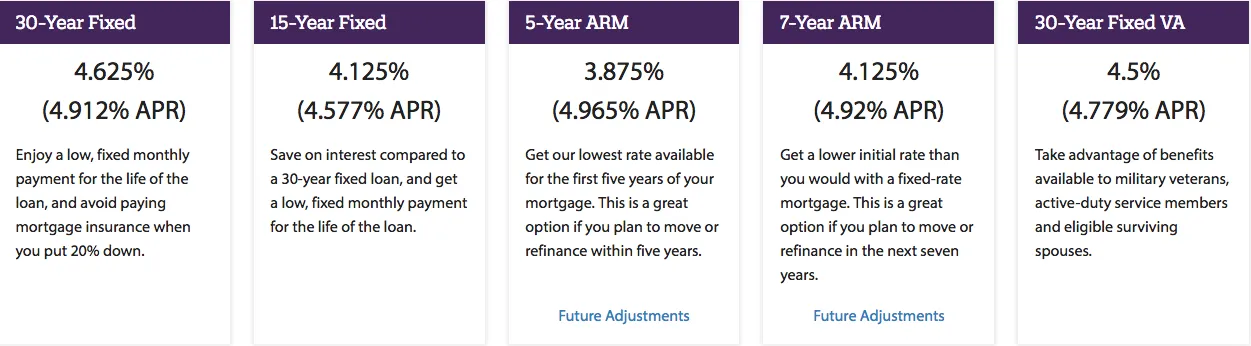

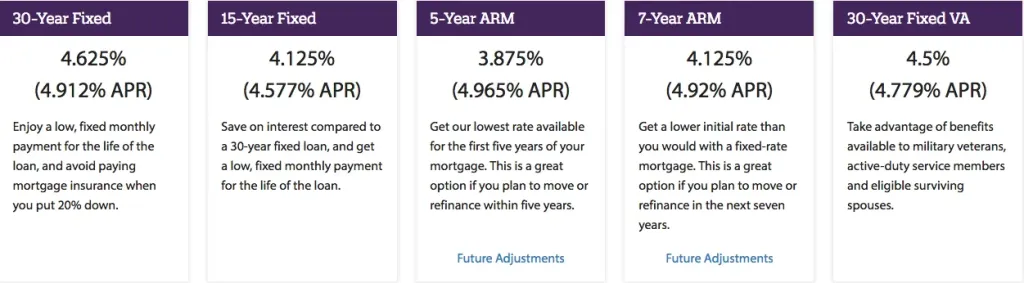

Current Quicken Loans Home Equity Loan Rates: What to Expect

As of the latest market data (Q4 2025), Quicken Loans home equity loan rates typically range from 5.25% to 7.75% APR for qualified borrowers. Below is a simplified snapshot:

- Excellent Credit (740+), LTV ≤ 70%: 5.25% – 5.75% APR

- Good Credit (700‑739), LTV ≤ 80%: 5.75% – 6.25% APR

- Fair Credit (660‑699), LTV ≤ 85%: 6.25% – 7.00% APR

- Below Average (620‑659), LTV ≤ 90%: 7.00% – 7.75% APR

These numbers are illustrative; actual rates will depend on the precise combination of the factors discussed earlier. Prospective borrowers should request a personalized quote to obtain an accurate figure.

Comparing Home Equity Loan Rates with Home Equity Line of Credit (HELOC) Rates

Many homeowners wonder whether a fixed‑rate home equity loan or a variable‑rate Home Equity Line of Credit (HELOC) better serves their needs. Quicken Loans offers both products, and while the interest rates for HELOCs are generally tied to the Prime Rate plus a margin, the fixed rates for home equity loans tend to be slightly higher but provide payment certainty.

For example, a borrower with an 800 credit score might see a HELOC rate of Prime + 0.5% (approximately 5.5% in the current environment), whereas the same borrower’s fixed home equity loan rate could sit at 5.6% APR. The choice often hinges on cash‑flow preferences: fixed rates lock in a steady payment schedule, whereas HELOCs allow flexible borrowing but expose the borrower to rate fluctuations.

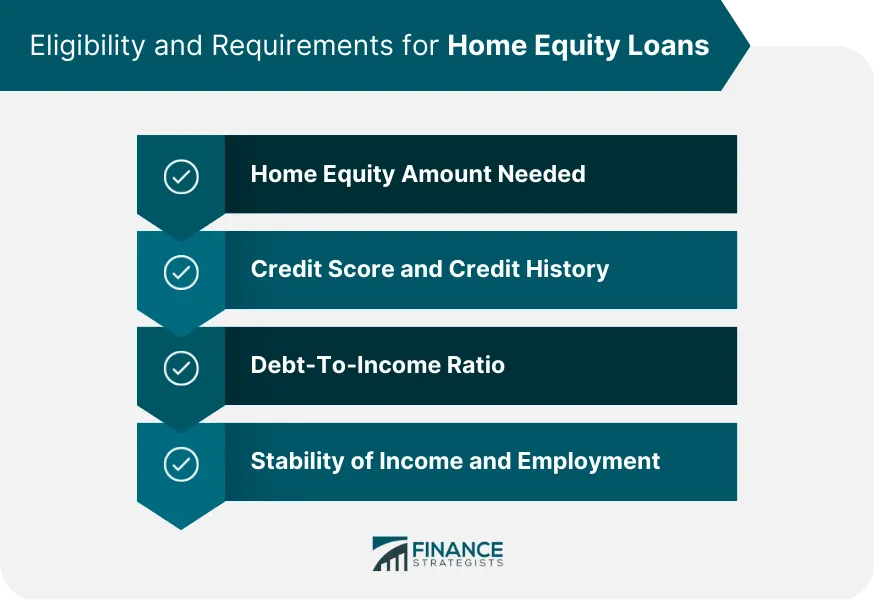

Eligibility Requirements for Quicken Loans Home Equity Loans

Before delving into the rate discussion, it is essential to understand who qualifies for a Quicken Loans home equity loan. The primary eligibility criteria include:

- Minimum Equity: Typically at least 15% equity after accounting for the new loan amount.

- Credit Score Threshold: Minimum 620 for most applicants; higher scores improve rate offers.

- Debt‑to‑Income (DTI) Ratio: Generally below 43%, though exceptions exist for higher credit scores.

- Primary Residence: The property must be the borrower’s primary home; investment properties are usually excluded.

- Stable Income: Proof of employment or consistent alternative income sources.

Meeting these baseline standards positions borrowers to receive a competitive quote within the Quicken Loans home equity loan rates spectrum.

Common Documentation Needed

Applicants should be prepared to submit the following documents during the application process:

- Recent pay stubs or tax returns (for self‑employed borrowers).

- Current mortgage statement.

- Property appraisal report (often ordered by the lender).

- Proof of homeowner’s insurance.

- Identification (driver’s license, passport, etc.).

Having these items ready can accelerate the underwriting timeline, potentially locking in a favorable rate before market shifts occur.

Cost Factors Beyond the Interest Rate

While the headline figure—Quicken Loans home equity loan rates—receives most attention, borrowers should also account for ancillary costs that affect the overall expense of the loan. These include:

- Origination Fee: Typically 0.5%‑1% of the loan amount, charged at closing.

- Appraisal Fee: Ranges from $300 to $600, depending on property size and location.

- Title Search and Recording Fees: Vary by state, generally $200‑$500.

- Prepayment Penalty: Some loans include a penalty for early payoff; however, Quicken Loans often waives this for home equity loans.

- Insurance Requirement: Lenders may require an increase in homeowners insurance coverage, adding to monthly costs.

When evaluating an offer, calculate the total cost of borrowing by adding these fees to the interest expense, thereby arriving at the true annual percentage rate (APR).

Tips for Reducing the Effective Rate

Borrowers seeking to lower the effective cost of their home equity loan can consider the following strategies:

- Improve credit score by paying down existing debts before applying.

- Increase the home’s equity through a recent appreciation or by making a larger down payment on the new loan.

- Choose a shorter loan term; although monthly payments rise, the interest rate may be lower and total interest paid decreases.

- Shop around for the best rate quote, even within the same lender, as Quicken Loans may offer multiple rate tiers based on timing and market conditions.

- Consider bundling the home equity loan with other Rocket Mortgage products to qualify for loyalty discounts.

Application Process: From Quote to Funding

The journey from obtaining a rate quote to receiving the funds typically follows these milestones:

- Online Pre‑Qualification: Using the Rocket Mortgage portal, borrowers input basic information to receive an estimated rate range.

- Full Application Submission: After reviewing the pre‑qualification, the applicant submits detailed financial data and authorizes a credit pull.

- Appraisal Scheduling: An approved appraiser visits the property to confirm its market value.

- Underwriting Review: The lender evaluates all documentation, confirms LTV, and finalizes the interest rate.

- Closing Disclosure: Borrower receives a detailed statement of loan terms, fees, and the exact interest rate.

- Funding: Once the borrower signs the closing documents, funds are disbursed—typically within 7‑10 business days.

Speed and transparency are hallmarks of the Quicken Loans platform, allowing borrowers to track each step via the online dashboard.

Related Resources

For readers interested in broader financing options, the Quicken Loans home equity line of credit – What You Need to Know article provides a parallel look at variable‑rate products, while the Quicken Loans Equity Line of Credit – A Complete Overview offers an in‑depth comparison of features and costs.

Future Outlook: How Market Trends May Influence Rates

Interest rates are inherently tied to economic cycles. As the Federal Reserve signals policy shifts, the Prime Rate—and consequently Quicken Loans home equity loan rates—may rise or fall. Analysts project modest increases in the coming year due to inflationary pressures, suggesting that borrowers who can secure a rate now might benefit from lower long‑term costs.

Conversely, a sudden economic downturn could prompt rate reductions, making it advantageous for borrowers to monitor the market and consider refinancing their home equity loan if rates drop significantly.

Key Takeaways for Prospective Borrowers

- Quicken Loans home equity loan rates currently sit between 5.25% and 7.75% APR, depending on credit and LTV.

- Eligibility hinges on sufficient equity, a minimum credit score of 620, and a healthy DTI ratio.

- Beyond the headline rate, factor in origination, appraisal, and other closing costs to gauge true expense.

- Improving credit, reducing LTV, and selecting a shorter term can all help secure a lower effective rate.

- Stay informed about macro‑economic trends, as they directly affect the future cost of borrowing.

By understanding the components that drive Quicken Loans home equity loan rates and approaching the application process with a clear strategy, homeowners can make informed decisions that align with their financial objectives. Whether the goal is home improvement, debt consolidation, or covering unexpected expenses, a well‑structured home equity loan offers a reliable avenue to unlock the value built into a property.