Table of Contents

- Quicken Loans Equity Line of Credit: How It Works

- Key Features of the Quicken Loans Equity Line of Credit

- Eligibility and Application Process

- Cost Structure and Fees

- Strategic Uses of a Quicken Loans Equity Line of Credit

- Home Improvement Projects

- Debt Consolidation

- Emergency Funding

- Investment Opportunities

- Comparison with Traditional Loans and Other HELOC Providers

- Risks and Mitigation Strategies

- Variable Rate Exposure

- Over‑Borrowing

- Impact on Credit Score

- Managing Your Quicken Loans Equity Line of Credit Effectively

- Future Outlook and Industry Trends

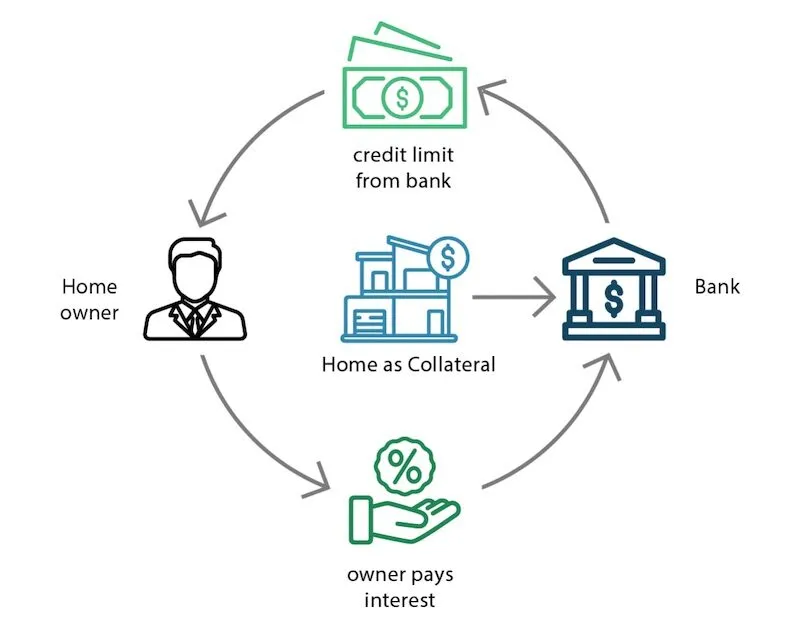

When homeowners look for flexible financing, the term “home equity line of credit” (HELOC) often surfaces as a viable alternative to traditional loans. Among the many lenders offering this product, Quicken Loans has built a reputation for digital convenience and transparent terms. Understanding the nuances of a Quicken Loans equity line of credit can help borrowers decide whether this revolving credit tool aligns with their financial goals.

The appeal of a revolving credit line lies in its flexibility: borrowers can draw funds as needed, repay them, and draw again without reapplying for a new loan each time. This characteristic makes the Quicken Loans equity line of credit especially attractive for home renovations, debt consolidation, or unexpected expenses. Yet, the very flexibility that makes it useful also demands a clear grasp of interest calculations, repayment structures, and potential pitfalls.

In the sections that follow, we will unpack the structure of the Quicken Loans equity line of credit, examine eligibility requirements, compare it with other credit products, and outline best‑practice strategies for managing the line responsibly. By the end, readers should have a factual, story‑driven picture of how this specific HELOC works in the broader lending landscape.

Quicken Loans Equity Line of Credit: How It Works

A Quicken Loans equity line of credit is a revolving credit facility secured by the equity you have built in your primary residence. Once approved, the lender assigns a maximum credit limit, often ranging from 15% to 30% of the home’s appraised value after subtracting any outstanding mortgage balances. Borrowers can then access funds through an online portal, a mobile app, or a linked debit card, pulling only what they need.

The interest rate on a Quicken Loans equity line of credit is typically variable, tied to a benchmark such as the prime rate plus a margin that reflects the borrower’s credit profile. Because the balance fluctuates with each draw and repayment, the interest charge is calculated daily on the outstanding principal, resulting in a payment that can vary month to month.

Key Features of the Quicken Loans Equity Line of Credit

- Variable Interest Rate: Adjusts with market conditions; rates are disclosed up front along with the margin.

- Draw Period: Usually 5 to 10 years, during which borrowers may withdraw funds and make interest‑only payments if they choose.

- Repayment Period: After the draw period ends, the line enters a repayment phase, typically lasting 10 to 20 years, during which only principal and interest payments are required.

- No Closing Costs (in many cases): Quicken Loans often waives origination fees for qualified applicants, though some states may impose recording fees.

- Online Management: A digital dashboard provides real‑time balance updates, transaction history, and the ability to transfer funds directly to a checking account.

These features mirror the broader HELOC market but are packaged with Quicken Loans’ online‑first approach, which can reduce paperwork and speed up approvals.

Eligibility and Application Process

To qualify for a Quicken Loans equity line of credit, applicants must meet several baseline criteria:

- Homeownership Status: The property must be your primary residence; second homes or investment properties are generally excluded.

- Equity Threshold: Lenders typically require at least 15% to 20% equity after accounting for the new line of credit.

- Credit Score: A minimum FICO score of 620 is common, though a score above 720 often secures the most favorable rates.

- Debt‑to‑Income Ratio (DTI): Most lenders prefer a DTI below 43%, though exceptions exist for high‑income borrowers.

- Stable Income: Documentation of steady employment or consistent self‑employment income is required.

The application itself is streamlined. Prospective borrowers begin by completing an online questionnaire, uploading documents such as a recent pay stub, tax return, and a property appraisal request. Once the lender verifies the information, a digital commitment letter is issued, and the credit line becomes active within a few days.

For borrowers who have previously faced payment difficulties, understanding loan forbearance may be relevant. If you’re curious about how forbearance works, the article Why Are My Loans in Forbearance? A Complete Guide provides a thorough explanation.

Cost Structure and Fees

While Quicken Loans markets many HELOCs with “no closing costs,” borrowers should still be aware of the following potential charges:

- Annual Fees: Some lines impose a modest yearly fee, usually ranging from $25 to $50.

- Early Termination Fee: If you close the line within the first two years, a fee equal to a percentage of the outstanding balance may apply.

- Appraisal Fees: A professional home appraisal is often required, costing $300–$500, though some lenders may waive this for high‑value properties.

- Minimum Draw Amount: Certain lines set a minimum draw, typically $500, which can affect borrowers who only need a small amount.

Interest expenses dominate the cost profile. Because the rate is variable, borrowers should monitor the prime rate and anticipate possible adjustments. The daily compounding method means that even a short increase in the balance can raise the next month’s payment.

Strategic Uses of a Quicken Loans Equity Line of Credit

Homeowners deploy the Quicken Loans equity line of credit for a range of financial strategies. Below are some of the most common applications:

Home Improvement Projects

Renovations that increase property value—such as kitchen remodels, bathroom upgrades, or adding a deck—are classic uses. By borrowing against equity, homeowners can fund these projects without tapping high‑interest credit cards.

Debt Consolidation

Because HELOC rates are often lower than credit‑card or personal loan rates, consolidating high‑interest debt into a Quicken Loans equity line of credit can reduce overall interest costs. However, borrowers must remain disciplined to avoid re‑accumulating debt.

Emergency Funding

A sudden medical expense or unexpected repair can be covered quickly through the revolving nature of the line. Since the credit is pre‑approved, funds are available without a new loan application.

Investment Opportunities

Some sophisticated borrowers use home equity to finance investment purchases, such as rental properties or a small business. This approach carries risk; the borrower’s home serves as collateral, so any default could jeopardize ownership.

When considering any of these uses, it’s prudent to review the tax implications. Although the 2017 Tax Cuts and Jobs Act limited the deductibility of HELOC interest, interest on a line used for home improvements may still qualify. For a deeper dive into deduction limits, see Student Loan Interest Deduction Income Limits: Full Guide.

Comparison with Traditional Loans and Other HELOC Providers

To gauge whether the Quicken Loans equity line of credit is the right fit, compare it against two common alternatives: a conventional home equity loan and a competitor’s HELOC.

| Feature | Quicken Loans Equity Line of Credit | Traditional Home Equity Loan | Competitor HELOC (e.g., Bank of America) |

|---|---|---|---|

| Repayment Structure | Revolving, draw period + repayment phase | Fixed‑amount, fixed term | Similar revolving model |

| Interest Rate Type | Variable (prime + margin) | Fixed or variable, often higher | Variable, may include rate caps |

| Application Speed | Online, 3–5 days | In‑person, 2–3 weeks | Online, 5–7 days |

| Closing Costs | Often waived | Typical lender fees | May charge origination fee |

| Maximum Credit Limit | 15%–30% of home equity | Up to 80% of home equity | Similar range |

The table illustrates that the Quicken Loans equity line of credit emphasizes speed and convenience, while traditional loans may provide higher borrowing limits but at the cost of longer processing times and potentially higher fees.

Risks and Mitigation Strategies

Every revolving credit product carries inherent risks. Below are the most salient concerns associated with the Quicken Loans equity line of credit and actionable steps to mitigate them.

Variable Rate Exposure

Since the interest rate can rise, borrowers should budget for a possible increase of 1%–2% over the life of the line. Setting a “stress‑test” budget—calculating payments at the highest projected rate—helps ensure affordability.

Over‑Borrowing

The ease of access can lead to unnecessary spending. Implementing a personal cap, such as limiting draws to a specific project budget, reduces the temptation to use the line for non‑essential purchases.

Impact on Credit Score

Utilizing a large portion of the available credit can raise your credit utilization ratio, potentially lowering your score. Keeping the balance below 30% of the limit is a widely recommended practice.

For readers who wonder whether paying off debt, including student loans, can affect credit, the article Does Paying Off Student Loans Hurt Credit? What You Need to Know provides useful insights.

Managing Your Quicken Loans Equity Line of Credit Effectively

Successful management hinges on disciplined borrowing, regular monitoring, and strategic repayment. Below are practical tips that align with the line’s flexibility while protecting your financial health.

- Set Automatic Alerts: Use the online portal to receive notifications when balances approach a predefined threshold.

- Make Principal Payments Early: Reducing the principal during the draw period can lower overall interest costs, even if the loan permits interest‑only payments.

- Review Rate Changes Quarterly: Stay informed about movements in the prime rate and adjust your repayment plan accordingly.

- Maintain an Emergency Reserve: Keep a separate savings buffer so you don’t rely on the HELOC for routine expenses.

- Plan for the Repayment Phase: As the draw period ends, transition from interest‑only to principal‑plus‑interest payments gradually to avoid a payment shock.

Future Outlook and Industry Trends

The HELOC market continues to evolve with technology integration and regulatory adjustments. Digital lenders like Quicken Loans are leading the shift toward fully online underwriting, which reduces reliance on physical documentation and accelerates funding.

Emerging trends that could affect future iterations of the Quicken Loans equity line of credit include:

- Dynamic Pricing Models: Real‑time risk assessment may result in personalized rates that adjust more frequently than the traditional prime‑plus‑margin structure.

- Hybrid Products: Some lenders are blending fixed‑rate portions with variable ones, offering borrowers a degree of predictability.

- Enhanced Consumer Education: Interactive tools embedded in the lender’s app can simulate payment scenarios, helping borrowers visualize long‑term costs.

These innovations aim to make HELOCs more transparent and adaptable, reinforcing the relevance of the Quicken Loans equity line of credit in a competitive lending landscape.

In summary, the Quicken Loans equity line of credit provides a versatile, digitally driven financing option for homeowners seeking to tap their home’s equity without the rigidity of a traditional loan. By understanding its structure, costs, and best‑practice management techniques, borrowers can harness the line’s flexibility while safeguarding against common pitfalls. Whether you’re planning a renovation, consolidating debt, or simply building a financial safety net, a well‑managed equity line of credit can serve as a valuable component of a broader wealth‑building strategy.