Table of Contents

- why are my loans in forbearance? Understanding the Basics

- why are my loans in forbearance – Common Triggers

- Eligibility Requirements and Application Process

- Steps to Verify the Forbearance Status

- Financial Impact of Forbearance

- Interest Accrual and Balance Growth

- Effect on Credit Score and Future Borrowing

- Related Reading: Does Paying Off Student Loans Hurt Credit? What You Need to Know

- Strategic Use of Forbearance

- How to Exit Forbearance and Resume Payments

- Related Guide: Student Loan Interest Deduction Income Limits: Full Guide

- Frequently Asked Questions

- Can I request multiple forbearances?

- Is forbearance the same as deferment?

- Will I lose eligibility for tax deductions during forbearance?

- What happens if I default while in forbearance?

Many borrowers find themselves staring at a statement that simply reads “forbearance” and wonder, why are my loans in forbearance? The answer is rarely a single event; rather, it is a combination of personal circumstances, lender policies, and broader economic conditions. Understanding the mechanics behind a forbearance status can help you take informed actions, protect your credit, and plan a smoother path back to regular payments.

Forbearance is often presented as a temporary reprieve—a pause or reduction in payments that can last from a few months to a year or more. While the term sounds neutral, the implications are far‑reaching, affecting interest accrual, future payment amounts, and even eligibility for certain tax deductions. In this article we walk through the most common reasons borrowers end up in forbearance, what the status means for your financial health, and practical steps to either exit the period or use it strategically.

Below we answer the core question: why are my loans in forbearance? By breaking down the triggers, eligibility criteria, and consequences, you’ll gain a clearer picture of how to manage your loans during challenging times.

why are my loans in forbearance? Understanding the Basics

At its core, forbearance is an agreement between a borrower and a lender that temporarily suspends or reduces loan payments. Unlike deferment, which may pause interest on certain loan types, most forbearance periods allow interest to continue accruing, which can increase the total balance you owe.

why are my loans in forbearance – Common Triggers

- Financial Hardship: A sudden loss of income, unexpected medical expenses, or other cash‑flow disruptions are the most frequent reasons lenders grant forbearance.

- Natural Disasters or Pandemic‑Related Impacts: Events such as hurricanes, wildfires, or public health emergencies often trigger government‑mandated forbearance programs.

- Enrollment in Education or Training Programs: Some borrowers who return to school or enroll in vocational training may qualify for forbearance while they focus on studies.

- Administrative Errors: Occasionally, a missed payment is incorrectly recorded, prompting lenders to place a loan in forbearance while they investigate.

- Eligibility for Income‑Driven Repayment (IDR) Review: While the IDR application is processed, lenders may place the loan in forbearance to avoid default.

When you ask yourself why are my loans in forbearance, look first at these trigger points. If any align with your recent circumstances, you likely have a clear explanation for the status.

Eligibility Requirements and Application Process

Understanding the eligibility criteria can help you determine whether a forbearance request was granted automatically or required your active involvement. Most lenders require you to provide documentation that substantiates the hardship or qualifying event.

Typical documentation includes recent pay stubs, tax returns, unemployment benefit statements, or medical bills. Some lenders also allow a simple online request, especially during nationwide crises when blanket forbearance policies are enacted.

Steps to Verify the Forbearance Status

- Log into your loan servicer’s portal and locate the “Payment History” or “Account Status” section.

- Check for any recent notices about forbearance, including start and end dates.

- Contact customer service to confirm the reason for the forbearance and whether it is discretionary or mandatory.

- Ask about interest accrual rules—some federal student loans suspend interest during certain forbearance types, while private loans usually do not.

Financial Impact of Forbearance

One of the most critical aspects of the question why are my loans in forbearance is understanding the cost of that decision. While the temporary relief can be essential, the interest that continues to accrue can significantly increase the total amount you will repay.

Interest Accrual and Balance Growth

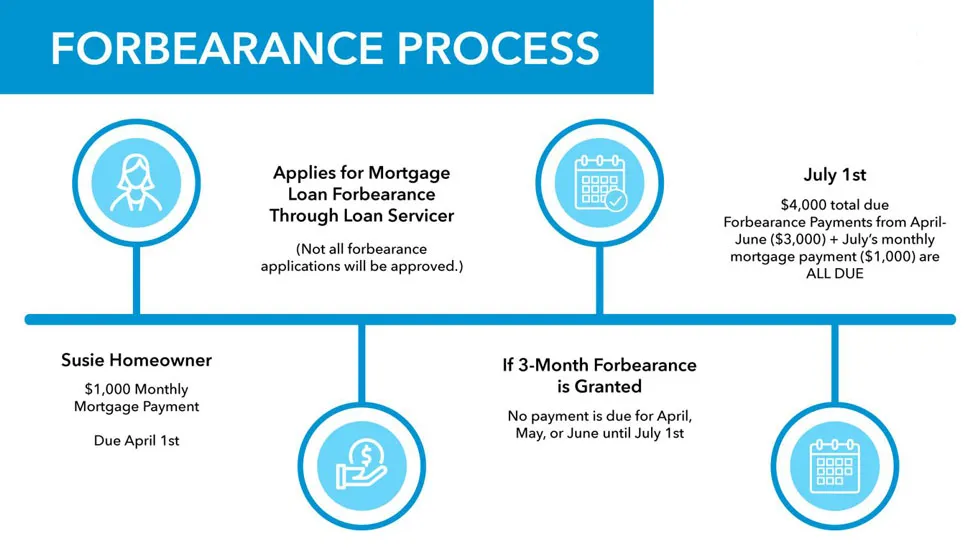

Consider a $20,000 loan at a 5% annual interest rate. If placed in a six‑month forbearance, interest will add roughly $500 to the principal. Over multiple forbearance periods, this compounding effect can add thousands to the final balance.

If you are a federal loan borrower, you might be eligible for a “pay‑as‑you‑go” option, where you make interest‑only payments during forbearance to prevent balance growth. Private lenders typically lack such flexible options, so paying at least the accrued interest is advisable.

Effect on Credit Score and Future Borrowing

While a forbearance itself does not directly damage your credit score, the indirect effects can. If you miss a payment before the forbearance is approved, that missed payment may be reported as delinquent, harming your credit.

Moreover, the higher balance caused by accrued interest can affect credit utilization ratios, especially for revolving credit lines. It is crucial to keep track of any missed or late payments and to confirm that the forbearance status is accurately reflected in your credit report.

Related Reading: Does Paying Off Student Loans Hurt Credit? What You Need to Know

Strategic Use of Forbearance

Forbearance should not be viewed as a long‑term solution, but it can be used strategically in certain scenarios:

- Saving for a Down Payment: Pausing payments while you accumulate funds for a house can be sensible if you can afford the accruing interest.

- Transitioning Between Jobs: A short forbearance during a career change can give you breathing room while you secure a new income source.

- Medical Recovery: If health issues prevent you from working, a forbearance can prevent default while you focus on recovery.

In each case, weigh the cost of additional interest against the benefit of temporary cash flow relief.

How to Exit Forbearance and Resume Payments

When the forbearance period ends, lenders typically send a reminder notice outlining the new payment schedule. To avoid surprise, take the following steps:

- Review the updated balance, including accrued interest.

- Adjust your budget to accommodate the resumed payment amount.

- Consider refinancing or switching to an income‑driven repayment plan if the payment feels unaffordable.

- Set up automatic payments to reduce the risk of missed installments.

If you anticipate difficulty resuming payments, contact your servicer before the end date. They may offer an extension, a switch to a different repayment program, or a new forbearance if another hardship arises.

Related Guide: Student Loan Interest Deduction Income Limits: Full Guide

Frequently Asked Questions

Can I request multiple forbearances?

Yes, most lenders allow successive forbearance periods, but each request may require new documentation. Be aware that repeated forbearances can significantly increase the total interest owed.

Is forbearance the same as deferment?

Not exactly. Deferment often pauses both payments and interest (especially on subsidized federal loans), whereas forbearance generally allows interest to continue accruing.

Will I lose eligibility for tax deductions during forbearance?

If interest accrues, you may still be eligible to claim the student loan interest deduction on your taxes, provided you meet the income thresholds. For details, see the Student Loan Interest Deduction Income Limit – A Complete Guide.

What happens if I default while in forbearance?

Default is unlikely during an approved forbearance, because the lender has formally paused collection activity. However, missing a payment before the forbearance is confirmed can trigger default proceedings.

Understanding why are my loans in forbearance is the first step toward managing the situation effectively. By recognizing the triggers, evaluating the financial impact, and planning an exit strategy, you can mitigate long‑term costs and keep your credit health intact. Use the information provided here to review your loan statements, communicate proactively with your servicer, and make choices that align with your broader financial goals.