Table of Contents

- does paying off student loans hurt credit: The Core Mechanics

- does paying off student loans hurt credit – Immediate Score Changes

- How Credit Scores Are Calculated and Why Student Loans Matter

- does paying off student loans hurt credit – Impact on Credit Mix

- Short‑Term vs. Long‑Term Effects

- Practical Tips to Safeguard Your Score After Payoff

- When Might Paying Off a Student Loan Actually Benefit Your Credit More Directly?

- Common Myths About Paying Off Student Loans and Credit Scores

For many borrowers, the moment they finally clear a student loan balance feels like a major life milestone. The sense of financial freedom is palpable, and the relief of no longer juggling monthly payments can be profound. Yet, amid the celebration, a common question surfaces: does paying off student loans hurt credit? The answer is not a simple yes or no; it depends on how credit scoring models interpret the change, the timing of the payoff, and the borrower’s overall credit profile.

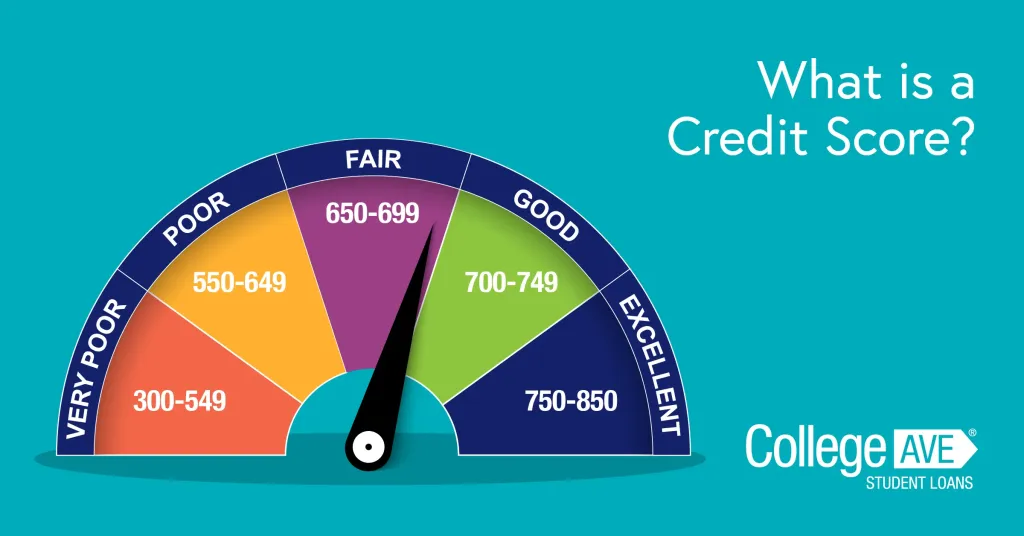

Understanding the mechanics behind credit scores helps demystify this concern. Credit scores are built on a blend of factors—payment history, amounts owed, length of credit history, new credit, and credit mix. Each factor reacts differently when a large installment loan is retired. By examining the data behind those five pillars, we can see whether the act of clearing a student loan is likely to cause a dip, a boost, or essentially no impact at all.

In the sections that follow, we will unpack the short‑term and long‑term effects, compare student loans to other types of debt, and offer practical steps to protect or improve your credit after the loan is paid in full. The goal is to provide a clear, factual roadmap for anyone wondering does paying off student loans hurt credit and what actions can be taken to keep a healthy credit score.

does paying off student loans hurt credit: The Core Mechanics

When a student loan is closed, the credit bureaus receive a status update indicating that the account is “paid in full.” This change triggers two immediate reactions in a credit report:

- Removal of the outstanding balance: The amount owed drops to zero, which can lower the “amounts owed” component of the score.

- Change in account status: The loan moves from “open” to “closed,” potentially shortening the average age of your revolving credit if the loan was one of your older accounts.

Both reactions are generally positive, but the scoring algorithms weigh them differently. For most FICO and VantageScore models, the “payment history” factor carries the most weight (35% for FICO). Since a paid‑in‑full loan adds a history of on‑time payments, the net effect is usually a modest increase. However, the “amounts owed” factor (30% for FICO) may see a slight dip because the total amount of revolving credit utilization is now calculated without the student loan’s contribution.

In practical terms, the question does paying off student loans hurt credit often resolves to a temporary, minor dip of a few points—if any—followed by a rebound as the credit report stabilizes.

does paying off student loans hurt credit – Immediate Score Changes

Credit scoring models update scores in batches, typically every 30 days after receiving new data from lenders. When the student loan servicer reports the payoff, the next scoring cycle may reflect:

- A reduction in the overall debt‑to‑income ratio, which can be favorable for lenders reviewing your application for new credit.

- A brief reduction in the “credit mix” score if the student loan was your only installment loan, because the mix of credit types becomes less diverse.

These adjustments are usually small—often under ten points—because the scoring formulas are designed to prevent drastic swings from a single event. Most borrowers who monitor their credit will notice a neutral or slightly positive change within a few months after the loan is closed.

How Credit Scores Are Calculated and Why Student Loans Matter

To fully answer does paying off student loans hurt credit, we need to revisit the five pillars of credit scoring:

- Payment History (35%): Timely payments are the strongest predictor of creditworthiness. A student loan that has been paid on schedule adds years of positive payment data.

- Amounts Owed (30%): This factor looks at credit utilization for revolving accounts and the total debt load for installment loans. Paying off a student loan reduces total debt, which is generally beneficial.

- Length of Credit History (15%): The age of your oldest account, average age of accounts, and age of specific account types matter. Closing an older loan can shave a few months off the average age, but the impact is marginal.

- Credit Mix (10%): Having both revolving (credit cards) and installment (auto, mortgage, student) accounts shows the ability to manage different debt types. Removing an installment loan could lower this component slightly if it was your sole installment account.

- New Credit (10%): Hard inquiries and recently opened accounts affect this pillar. Paying off a loan does not generate a hard inquiry, so it has no negative impact here.

Given this breakdown, the most significant positive influence of a paid‑off student loan is the enhancement of the payment history component. The only areas where does paying off student loans hurt credit could be true are the minor reductions in credit mix and length of credit history—both of which are outweighed by the gains in payment history and reduced debt.

does paying off student loans hurt credit – Impact on Credit Mix

If you have a robust portfolio of credit cards, an auto loan, and perhaps a mortgage, the loss of a student loan will have almost no perceptible effect on your credit mix. However, for borrowers whose only installment debt is a student loan, the closure can reduce the diversity score. In such cases, the dip is typically less than five points, and it can be mitigated by maintaining low utilization on credit cards and, if feasible, opening another installment account (such as a small personal loan) responsibly.

Short‑Term vs. Long‑Term Effects

Short‑term effects are often the focus when someone asks does paying off student loans hurt credit. In the first 30‑60 days after payoff, you might see a small fluctuation due to the credit mix and length adjustments mentioned earlier. After the next reporting cycle, the score usually stabilizes and often improves because the debt‑to‑income ratio has decreased and the payment history is now fully positive.

Long‑term effects are more favorable. Over a period of 12‑24 months, the benefits of having zero student loan debt become more pronounced:

- Lower debt‑to‑income ratio: Future lenders view you as less risky, which can lead to better loan terms.

- Continued positive payment history: The “paid in full” status remains on the credit report for up to ten years, continuously reinforcing your creditworthiness.

- Increased borrowing capacity: With the loan removed, you have more room to take on new credit without harming utilization percentages.

Thus, while the short‑term answer to does paying off student loans hurt credit may be “it can cause a tiny dip,” the long‑term outlook is clearly positive.

Practical Tips to Safeguard Your Score After Payoff

Even if the impact is minimal, taking proactive steps can ensure your credit continues to rise after the loan is paid. Below are actionable recommendations:

- Keep older credit cards open: The length of credit history benefits from accounts that have been active for many years.

- Maintain low credit‑card utilization: Aim for less than 30% of total available credit; ideally under 10% for the best score impact.

- Monitor your credit reports: Check all three major bureaus (Equifax, Experian, TransUnion) at least once a year to confirm the payoff is reported accurately.

- Consider a small, secured installment loan: If your credit mix suffers, a low‑balance secured loan (such as a credit‑builder loan) can restore mix without adding significant risk.

- Stay disciplined with new credit applications: Each hard inquiry can shave a few points, so only apply for credit when truly needed.

These steps align with the broader principle of responsible credit management, and they can be applied whether you’re pondering does paying off student loans hurt credit or navigating other financial decisions. For example, understanding how a USAA auto loan works can help you balance installment credit across different loan types. You can read more about it in the guide How Does USAA Auto Loan Work – Complete Guide, which offers insight into managing multiple credit obligations.

When Might Paying Off a Student Loan Actually Benefit Your Credit More Directly?

There are scenarios where clearing a student loan can be a strategic move to improve credit:

- High debt‑to‑income ratio: Lenders often set thresholds (e.g., 43%). Paying off the loan can bring you below that line, making you eligible for better mortgage or auto loan rates.

- Preparing for a major purchase: If you plan to buy a home, a lower overall debt load can improve the loan‑to‑value assessment.

- Transitioning to a new credit building strategy: Some borrowers intentionally close older installment accounts after a long period of positive payment history to reset the credit mix in anticipation of adding a mortgage.

In each of these cases, the question does paying off student loans hurt credit becomes secondary to the larger financial advantage of reduced debt and a stronger application profile.

Common Myths About Paying Off Student Loans and Credit Scores

Myth #1: “Paying off a loan will instantly raise your score.”

Reality: Scores adjust gradually as data flows to the bureaus. Immediate changes are typically modest.

Myth #2: “Closing any account always hurts credit.”

Reality: Closing an account can affect length of credit history and mix, but the overall impact depends on the account’s weight in your credit profile.

Myth #3: “Only revolving credit matters.”

Reality: Installment accounts, like student loans, contribute significantly to payment history and total debt calculations.

By separating fact from fiction, borrowers can answer the core question—does paying off student loans hurt credit—with confidence and make informed decisions.

In summary, the act of paying off a student loan is unlikely to cause a meaningful drop in your credit score. Any short‑term dip is outweighed by the long‑term benefits of reduced debt, a pristine payment record, and a healthier credit profile. By following the practical tips outlined above and keeping an eye on your credit reports, you can ensure that the payoff becomes a stepping stone toward stronger financial health rather than a source of worry.

Remember, credit scores are dynamic, and they reflect the totality of your financial behavior over time. The decision to eliminate a student loan should be guided by your overall financial goals, not by a fear that the payoff will damage your credit.