Table of Contents

- Insurance Quotes for Home and Auto: Why Bundling Matters

- Insurance Quotes for Home and Auto: Key Factors That Influence Your Premium

- Step‑by‑Step Process to Get Accurate Insurance Quotes for Home and Auto

- 1. Gather Essential Information

- 2. Use Reputable Quote Comparison Tools

- 3. Review Coverage Details, Not Just Prices

- 4. Ask About Discounts and Eligibility

- 5. Evaluate the Insurer’s Reputation and Claims Process

- Tips to Maximize Savings on Insurance Quotes for Home and Auto

- Increase Your Deductible Wisely

- Maintain a Good Credit Score

- Take Advantage of Home Improvements

- Bundle With the Same Insurer

- Review Annually and Adjust Coverage

- Common Misconceptions About Insurance Quotes for Home and Auto

- Myth 1: The Lowest Quote Is Always the Best Deal

- Myth 2: My Current Insurer Offers the Best Price

- Myth 3: Homeowners Insurance Covers Everything in My Home

- Myth 4: My Car’s Age Doesn’t Affect the Quote

- How Technology Is Changing the Way We Get Insurance Quotes for Home and Auto

- Practical Example: Comparing Three Quotes

- Final Thoughts on Securing the Right Insurance Quotes for Home and Auto

Finding reliable insurance quotes for home and auto can feel like navigating a maze of numbers, policies, and fine print. Most homeowners and drivers start their search hoping for a quick online estimate, only to encounter confusing jargon and unexpected exclusions. This article walks you through the essential steps to obtain accurate quotes, compare them intelligently, and ultimately choose coverage that fits both your lifestyle and budget.

Whether you are a first‑time buyer, a long‑time policyholder looking to refinance, or simply someone curious about how rates are calculated, understanding the mechanics behind insurance quotes for home and auto is crucial. By demystifying the process, you gain the confidence to ask the right questions, spot hidden costs, and leverage discounts that many consumers overlook.

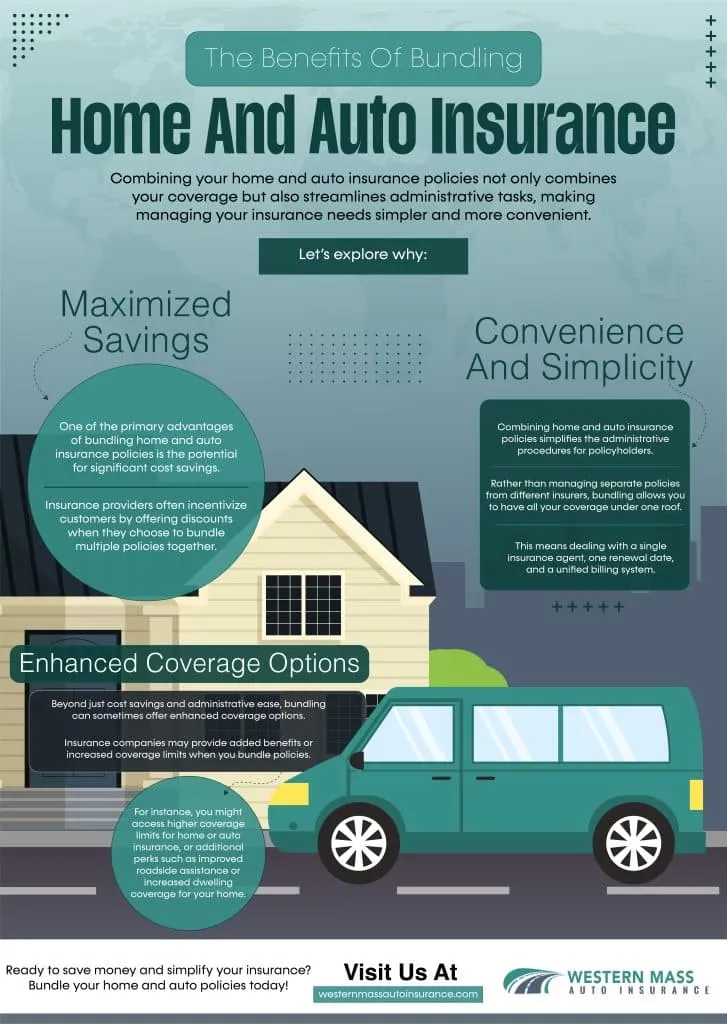

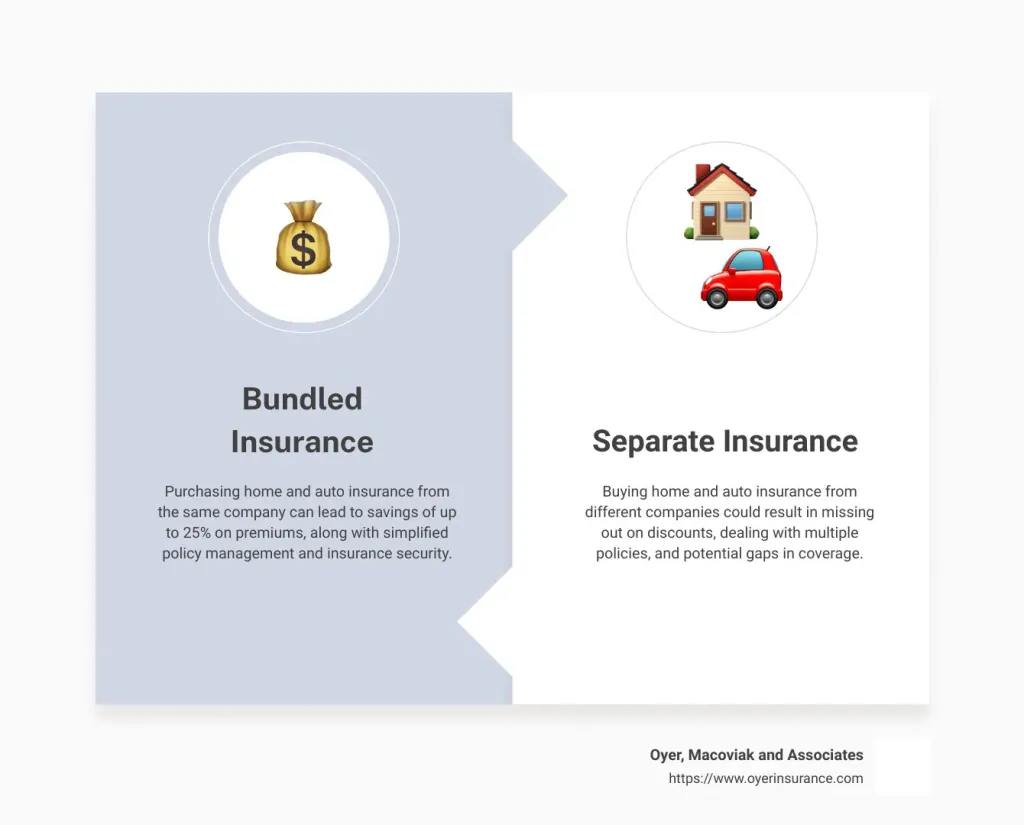

Insurance Quotes for Home and Auto: Why Bundling Matters

One of the most effective strategies for reducing premiums is bundling your home and auto policies with the same insurer. Insurers often reward customers who place multiple policies under one roof with multi‑policy discounts, sometimes ranging from 5 % to 25 % off the total premium. Bundling also simplifies the management of your policies, as you deal with a single point of contact for claims, renewals, and updates.

However, bundling isn’t a universal silver bullet. The degree of savings depends on the insurer’s pricing model, the coverage limits you need, and the risk profile of your home and vehicle. Therefore, it remains essential to obtain several insurance quotes for home and auto before deciding whether a bundle truly offers the best value.

Insurance Quotes for Home and Auto: Key Factors That Influence Your Premium

- Location and Property Characteristics – The zip code, proximity to fire stations, and crime rates directly affect home insurance rates.

- Driving Record and Vehicle Details – A clean driving record, low mileage, and safety features can lower auto premiums.

- Coverage Limits and Deductibles – Higher limits provide broader protection but raise the cost; larger deductibles have the opposite effect.

- Credit Score – Many insurers use credit-based insurance scores to gauge risk, influencing both home and auto quotes.

- Claims History – Frequent past claims signal higher risk, leading to higher quotes.

Understanding these variables helps you tailor the information you provide when requesting insurance quotes for home and auto, ensuring the estimates you receive are as accurate as possible.

Step‑by‑Step Process to Get Accurate Insurance Quotes for Home and Auto

Below is a systematic approach you can follow to gather and compare insurance quotes for home and auto efficiently.

1. Gather Essential Information

Before you start filling out online forms, compile the following data:

- Home address, year built, square footage, construction type, and any recent renovations.

- Current home insurance policy details, including coverage limits and deductible amounts.

- Vehicle identification number (VIN), make, model, year, mileage, and any aftermarket accessories.

- Driving history for the past three years, including tickets, accidents, and the number of licensed drivers in the household.

- Personal details such as age, marital status, and credit score (if you are comfortable sharing).

Having this information at hand reduces the chance of errors and speeds up the quoting process.

2. Use Reputable Quote Comparison Tools

Many insurers provide instant quotes on their websites, but you can also leverage independent comparison platforms that aggregate offers from multiple carriers. These tools let you input the same data once and receive a side‑by‑side view of premiums, coverage options, and discounts.

For a practical example, check out the article Insurance Quotes for Auto and Home – How to Find the Best Rates, which outlines the best online tools and how to interpret their results.

3. Review Coverage Details, Not Just Prices

While the headline premium is important, the true value lies in the coverage specifics. Examine:

- Dwelling coverage (home) and liability limits (auto).

- Replacement cost vs. actual cash value for home contents.

- Uninsured/underinsured motorist protection and medical payments for auto.

- Optional endorsements such as flood insurance, identity theft protection, or roadside assistance.

Comparing these elements helps you avoid low‑cost policies that may leave gaps in protection.

4. Ask About Discounts and Eligibility

Many insurers offer discounts that are not automatically applied. Common savings include:

- Multi‑policy (home + auto) discount.

- Good driver or safe driver discount.

- Home security system, smoke detectors, or fire alarms.

- Anti‑theft devices and vehicle safety features.

- Loyalty or long‑term customer discounts.

When you request insurance quotes for home and auto, explicitly inquire about each of these. A quick phone call can sometimes shave off an additional 10 % or more from your premium.

5. Evaluate the Insurer’s Reputation and Claims Process

Price alone should not dictate your decision. Investigate the insurer’s claim settlement record, customer service ratings, and financial stability. Resources such as J.D. Power, Consumer Reports, and AM Best provide independent assessments.

Reading real‑world experiences, such as those found in Insurance Quote for Home and Auto – How to Get the Best Coverage, can give you insight into how insurers handle claims after a loss.

Tips to Maximize Savings on Insurance Quotes for Home and Auto

Even after you have gathered several quotes, there are strategic moves you can make to lower your final cost.

Increase Your Deductible Wisely

Choosing a higher deductible reduces the premium for both home and auto policies. However, ensure the deductible amount is affordable enough to cover out‑of‑pocket expenses in case of a claim. A common practice is to set a deductible that you could comfortably pay within a few weeks.

Maintain a Good Credit Score

Since many insurers use credit‑based insurance scores, improving your credit rating can directly lower your insurance quotes for home and auto. Pay down existing debt, keep credit card balances low, and correct any errors on your credit report.

Take Advantage of Home Improvements

Upgrading to fire‑resistant roofing, installing a security system, or reinforcing windows can qualify you for additional discounts. Document these improvements and provide proof when requesting new insurance quotes for home and auto.

Bundle With the Same Insurer

As highlighted earlier, bundling can produce significant savings. Yet, don’t bundle automatically; compare the bundled quote with the sum of separate policies to verify the true benefit.

Review Annually and Adjust Coverage

Life changes—marriage, a new car, a home renovation—affect your risk profile. Conduct a yearly review of your insurance quotes for home and auto, adjusting coverage limits and deductibles to reflect your current needs.

Common Misconceptions About Insurance Quotes for Home and Auto

Many consumers hold beliefs that can lead to overpaying or under‑insuring. Below are a few myths clarified.

Myth 1: The Lowest Quote Is Always the Best Deal

Low premiums often accompany reduced coverage, higher deductibles, or exclusions. Always read the policy details before deciding.

Myth 2: My Current Insurer Offers the Best Price

Even loyal customers can benefit from market competition. Obtaining fresh insurance quotes for home and auto each renewal period can uncover better rates.

Myth 3: Homeowners Insurance Covers Everything in My Home

Standard policies typically exclude flood, earthquake, and certain high‑value items. Separate endorsements or policies may be necessary for full protection.

Myth 4: My Car’s Age Doesn’t Affect the Quote

Older vehicles generally have lower liability premiums but may cost more for comprehensive coverage due to higher repair costs for rare parts. Adjust coverage accordingly.

How Technology Is Changing the Way We Get Insurance Quotes for Home and Auto

Advancements in data analytics, telematics, and artificial intelligence have streamlined the quoting process. Insurers now use:

- Smart home devices to monitor risk factors such as fire or water leaks, potentially lowering home premiums.

- Telematics apps that track driving behavior, rewarding safe drivers with lower auto rates.

- AI‑driven chatbots that gather information 24/7 and produce instant insurance quotes for home and auto.

These tools not only speed up the acquisition of insurance quotes for home and auto but also personalize pricing based on actual risk rather than broad demographics.

Practical Example: Comparing Three Quotes

Imagine you own a 2,000‑sq‑ft home built in 1995 and drive a 2020 sedan with a clean record. After using a comparison website, you receive the following annual premiums (bundled):

- Insurer A: $1,200 – Includes flood endorsement, $1,000 deductible.

- Insurer B: $1,080 – No flood coverage, $500 deductible, 15 % multi‑policy discount.

- Insurer C: $1,150 – Includes roadside assistance for auto, $750 deductible, 10 % discount for security system.

To decide, weigh the added value of the flood endorsement against the lower price of Insurer B, consider your willingness to pay a higher deductible, and evaluate the reputation of each insurer. This structured comparison illustrates why looking beyond the headline figure is essential when reviewing insurance quotes for home and auto.

Final Thoughts on Securing the Right Insurance Quotes for Home and Auto

Obtaining accurate insurance quotes for home and auto is a multi‑step journey that blends data collection, strategic comparison, and an awareness of personal risk factors. By following the systematic approach outlined above—gathering comprehensive information, using reliable comparison tools, scrutinizing coverage details, and negotiating discounts—you position yourself to secure coverage that protects your assets without breaking the bank.

Remember, the market evolves, and so do your personal circumstances. Regularly revisiting your policies, staying informed about new discount opportunities, and leveraging technological advances will keep your insurance portfolio both cost‑effective and robust.

For more detailed guidance, explore additional resources such as Car Insurance and Homeowners Insurance Quotes: A Complete Guide and Compare Home and Auto Insurance Quotes Online – A Complete Guide, which delve deeper into specific scenarios and offer step‑by‑step instructions.