Table of Contents

- How to Get Accurate auto and home insurance quotes online

- Benefits of auto and home insurance quotes online

- Key Factors That Influence Your Quote

- Location and Weather Risks

- Vehicle Type and Usage

- Policy Limits and Deductibles

- Bundling Discounts

- Step‑by‑Step Process to Compare Quotes

- Common Mistakes to Avoid When Using Online Quote Tools

- Skipping the “Exact Address” Field

- Ignoring Policy Exclusions

- Relying Solely on the Lowest Quote

- Forgetting to Update Personal Changes

- How Technology Enhances the Quote Experience

- Future Trends for auto and home insurance quotes online

In today’s digital era, buying insurance has moved from the phone book to the click of a mouse. Whether you are a first‑time driver or a seasoned homeowner, the ability to request auto and home insurance quotes online opens a world of options that were once limited to local agents and paper forms. This shift not only accelerates the shopping process but also brings transparency, allowing consumers to see side‑by‑side comparisons of price, coverage limits, and policy features.

The convenience of online platforms does not mean you should skip the homework. Understanding the nuances of each policy, the factors that influence premiums, and the ways to personalize coverage is essential for making an informed decision. In this article, we walk through the entire journey—from preparing your personal information to evaluating the final offer—so you can confidently navigate the landscape of auto and home insurance quotes online.

By the end of this guide, you will know how to avoid common pitfalls, leverage digital tools for maximum savings, and pinpoint the exact coverage you need for both your vehicle and your dwelling. Let’s start by demystifying the basic components that insurers examine before they generate a quote.

How to Get Accurate auto and home insurance quotes online

When you request auto and home insurance quotes online, insurers typically ask for a series of data points that help them assess risk. The more precise the information you provide, the more accurate the quote will be. Below are the core categories of data you should expect to input:

- Personal details: Name, date of birth, marital status, and address. These affect both auto and home rates because insurers consider demographic trends.

- Vehicle information: Make, model, year, VIN, mileage, and primary usage. Even the color of the car can influence the premium in some markets.

- Home characteristics: Square footage, construction type, year built, roof material, and presence of safety devices such as smoke detectors or security systems.

- Driving and claims history: Any accidents, tickets, or prior insurance claims in the past three to five years.

- Credit score (where permitted): Many insurers use credit-based insurance scores to predict risk, though rules vary by state.

Once this data is entered, the insurer’s algorithm calculates a provisional premium. Most platforms allow you to adjust deductible levels or add optional endorsements, instantly showing how those changes affect the final price.

Benefits of auto and home insurance quotes online

Obtaining auto and home insurance quotes online offers several tangible advantages over traditional methods:

- Speed: A full comparison can be completed in under ten minutes, versus days or weeks spent calling agents.

- Transparency: You can see exactly what each component of the premium covers, making it easier to spot unnecessary add‑ons.

- Cost savings: Competitive digital marketplaces drive down prices. For example, a driver in Florida who searched for the lowest cost auto insurance in Florida often found discounts of 10‑15% compared to quoted rates from local offices.

- Customization: Online tools let you experiment with bundle discounts—combining auto and home policies on the same carrier frequently yields a further reduction.

- Record keeping: Digital quotes are stored in your account, allowing you to revisit them later and track price changes over time.

Key Factors That Influence Your Quote

Even though the process is automated, the underlying risk assessment follows the same actuarial principles insurers have used for decades. Understanding these factors helps you control the variables you can influence.

Location and Weather Risks

Where you live is a major determinant. Coastal homes are more prone to hurricanes, while certain zip codes experience higher rates of vehicle theft. Insurers incorporate these regional hazards into the premium calculation. If you own a home in an area with frequent severe weather, consider adding windstorm coverage or a separate flood policy to avoid gaps.

Vehicle Type and Usage

High‑performance cars, luxury SUVs, or vehicles with advanced safety features each affect pricing differently. A sports car typically carries a higher premium because of repair costs and accident severity, while a vehicle equipped with anti‑lock brakes and airbags may qualify for a discount.

Policy Limits and Deductibles

Choosing higher coverage limits raises the premium, but it also protects you from larger out‑of‑pocket expenses after a claim. Conversely, a higher deductible reduces the monthly cost but means you’ll pay more before insurance kicks in. Online quote tools usually display a slider that lets you see the cost impact in real time.

Bundling Discounts

Many insurers reward customers who purchase both auto and home insurance from the same company. Bundling can shave anywhere from 5% to 25% off each policy, depending on the carrier. When you request auto and home insurance quotes online, look for a “bundle” option that automatically recalculates the combined price.

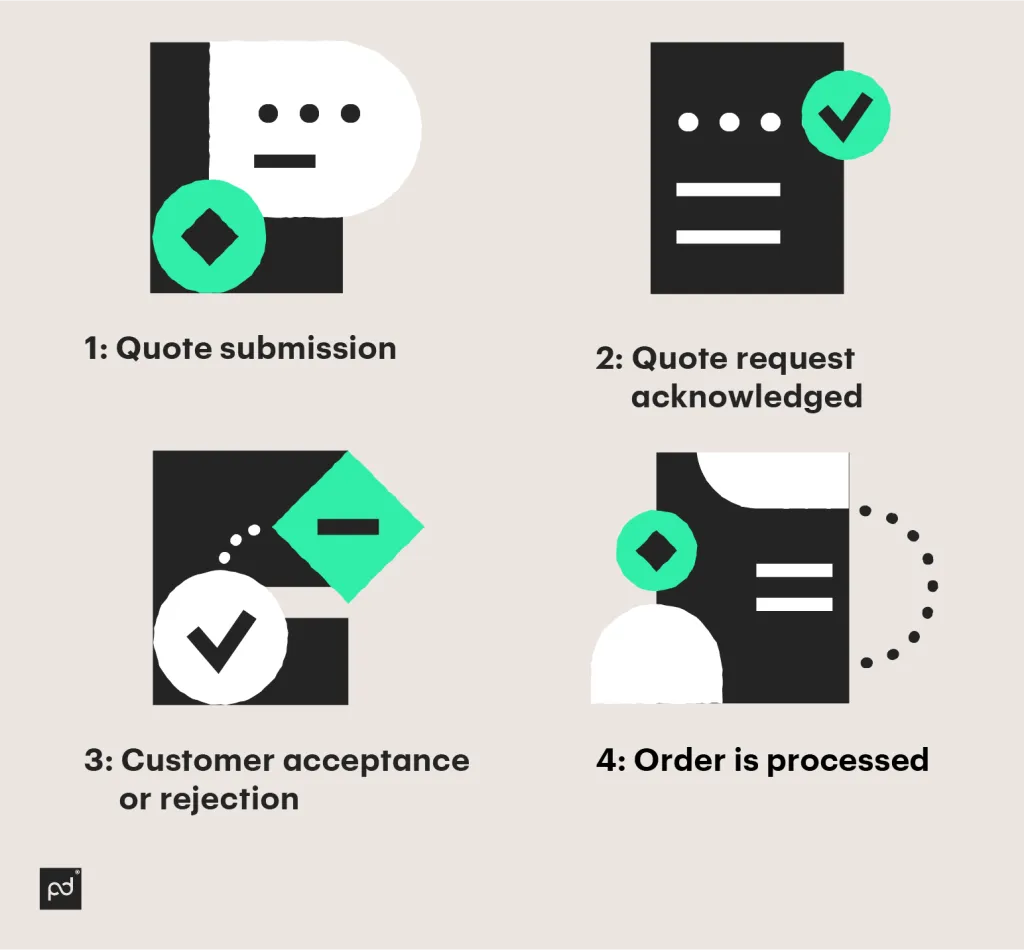

Step‑by‑Step Process to Compare Quotes

Below is a practical roadmap you can follow the next time you sit down at your computer to shop for coverage.

- Gather documentation: Have your driver’s license, vehicle registration, VIN, mortgage statement, and a recent home appraisal ready.

- Visit multiple quote portals: Use at least three reputable sites—company websites, independent aggregators, and comparison engines.

- Enter identical information: Consistency ensures that differences in price stem from the insurer’s underwriting, not data entry errors.

- Adjust coverage options: Play with deductible levels, liability limits, and optional add‑ons like roadside assistance or personal property coverage.

- Review discounts: Look for safe‑driver discounts, multi‑policy bundles, loyalty credits, or affiliations (e.g., alumni groups).

- Read the fine print: Check exclusions, claim‑handling procedures, and renewal terms before you decide.

- Contact a representative if needed: Some questions—like coverage for a home‑based business—may require a follow‑up call.

- Make a decision and purchase: Once satisfied, you can often complete the transaction online, upload required documents, and receive proof of insurance instantly.

Following this methodical approach maximizes your chance of finding a balanced policy that fits both your budget and your protection needs.

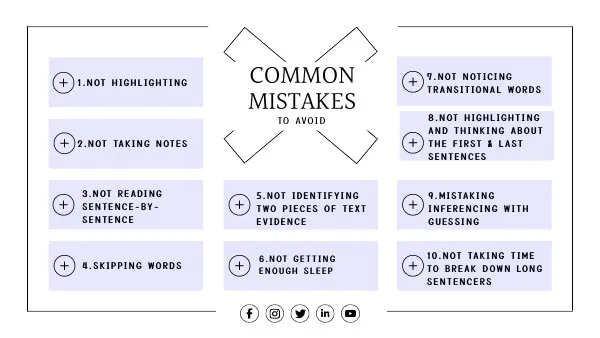

Common Mistakes to Avoid When Using Online Quote Tools

Even seasoned shoppers can fall into traps that inflate the cost or weaken coverage. Here are the most frequent errors and how to prevent them.

Skipping the “Exact Address” Field

Some platforms allow you to enter a zip code only. While quicker, this can produce an inaccurate estimate because insurance rates vary block by block. Always input the precise street address for both your home and the primary location where the car is parked.

Ignoring Policy Exclusions

A low premium may hide significant exclusions. For instance, a homeowner’s policy that does not cover water damage from a burst pipe could leave you exposed. Read the exclusion list carefully, or use the internal link does home insurance cover structural problems? to learn what typical gaps look like.

Relying Solely on the Lowest Quote

The cheapest option is not always the best. A minimal premium often reflects reduced limits or fewer endorsements. Compare the value of each policy, not just the price tag.

Forgetting to Update Personal Changes

Life events—marriage, moving, adding a teen driver—should trigger a fresh set of quotes. An outdated profile can lead to overpayment or under‑coverage.

How Technology Enhances the Quote Experience

Artificial intelligence, big data, and mobile apps have transformed how insurers assess risk and present offers. Predictive models analyze traffic patterns, weather forecasts, and even social media activity to fine‑tune premiums. Some insurers now provide a “virtual inspection” of your home using smartphone photos, cutting down the need for an in‑person adjuster.

Moreover, telematics devices—often called “smart car” gadgets—track driving behavior such as speed, hard braking, and mileage. By sharing this data through an app, drivers can earn usage‑based discounts, which are reflected instantly in the online quote.

Future Trends for auto and home insurance quotes online

Expect further integration of blockchain for secure policy storage, AI chatbots for 24/7 claim assistance, and hyper‑personalized bundles that adjust coverage in real time based on lifestyle changes. As these technologies mature, the gap between online convenience and personalized service will continue to shrink.

In the meantime, the best strategy remains simple: stay informed, compare diligently, and use the digital tools at your disposal to secure the most appropriate protection for your vehicle and your home.

By following the steps and considerations outlined above, you can confidently navigate the world of auto and home insurance quotes online, ensuring that you get the coverage you need at a price that makes sense. Remember, the goal is not just to find the cheapest option but the most comprehensive one that aligns with your unique circumstances. Happy shopping, and drive and live safely!