Table of Contents

- does usaa renters insurance cover storage units

- does usaa renters insurance cover storage units – key policy details

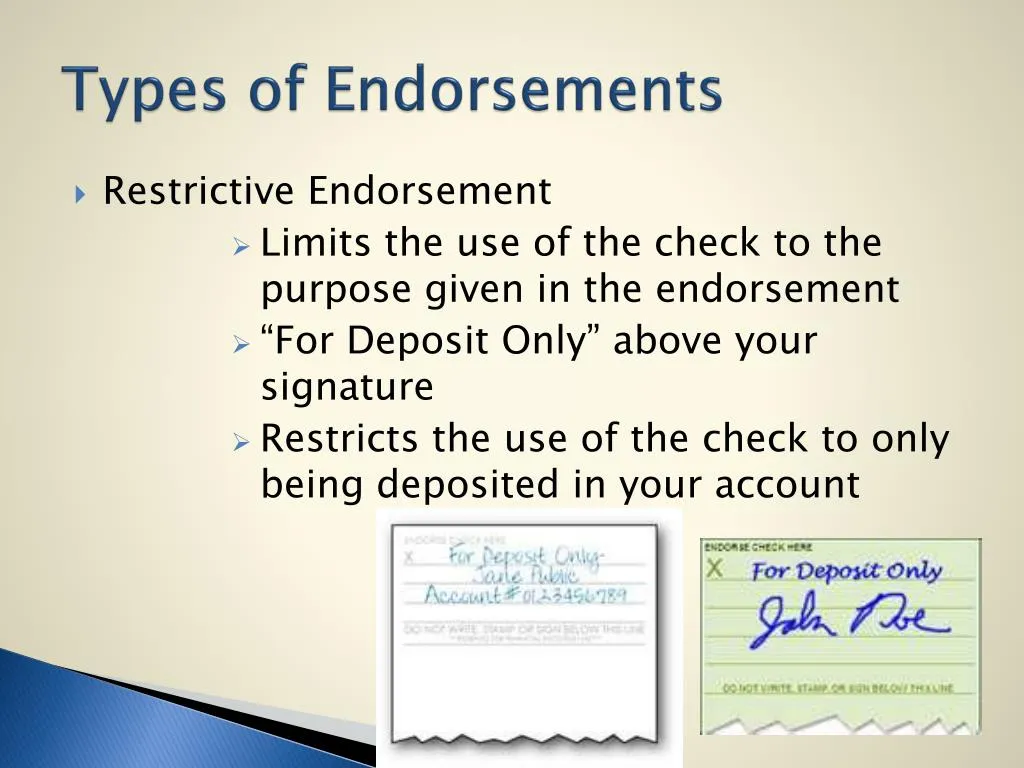

- Understanding the Role of Endorsements

- Practical Tips for Protecting Your Stored Belongings

- Document Your Inventory

- Choose a Secure Facility

- Lock It Right

- Review the Facility’s Insurance

- Update Your Policy When Needed

- When a Claim Happens: Step‑by‑Step Process

- Comparing USAA to Other Renters Insurance Options

When you’re a renter, the thought of protecting the items you keep in a storage unit can feel like a puzzle missing several pieces. Many renters assume that their standard policy automatically extends to off‑site storage, while others fear that any loss will leave them paying out of pocket. The real answer hinges on the specifics of the policy you hold and the language used by the insurer. This article unpacks the question, “does USAA renters insurance cover storage units,” and guides you through the practical steps to secure adequate protection for the belongings you stash away.

USAA, known for serving military families and veterans, offers renters insurance that mirrors many industry standards but also includes unique provisions tied to the organization’s values. Understanding how those provisions translate to storage units requires a careful look at the policy’s personal property coverage, optional endorsements, and the definition of “off‑premises” items. By the end of this guide, you’ll know exactly where the coverage gaps are, what you can add, and how to decide whether to rely on USAA or seek supplemental protection.

Before diving into the details, remember that insurance policies are contracts—each clause matters. If you have a storage unit, you’ll want to confirm the coverage limits, deductible options, and any exclusions that could affect a claim. Let’s explore the core components of USAA renters insurance and see how they apply to storage units.

does usaa renters insurance cover storage units

The short answer is that USAA’s standard renters insurance does provide limited coverage for personal property stored off‑premises, but the extent of that coverage depends on several factors. Under the typical “Personal Property” section, USAA extends protection to items that are temporarily away from the insured residence, such as those in a car trunk or a friend’s house. However, when it comes to a dedicated storage unit, the policy treats the location as an “off‑premises” site, and the coverage is subject to specific limits and conditions.

USAA generally caps off‑premises personal property coverage at 10% of the total personal property limit. For example, if your overall personal property limit is $30,000, only $3,000 of that amount can be used to cover losses that occur in a storage unit. This ceiling applies regardless of the cause of loss—whether fire, theft, vandalism, or a natural disaster—unless you purchase an endorsement that raises the limit.

does usaa renters insurance cover storage units – key policy details

- Coverage Limit: By default, off‑premises items, including those in storage units, are covered up to 10% of the personal property limit. This limit can be increased with a “Scheduled Personal Property” endorsement, which allows you to name high‑value items and assign higher coverage amounts.

- Covered Perils: USAA’s renters policy typically follows a “named peril” model, covering risks such as fire, lightning, windstorm, hail, explosion, theft, and vandalism. If your storage unit suffers damage from a covered peril, the claim can be filed under the off‑premises provision.

- Exclusions: Common exclusions that affect storage units include water damage from flooding (unless you have a separate flood endorsement), mold, and wear‑and‑tear. Also, losses caused by neglect—like leaving a unit unlocked—may be denied.

- Deductibles: The deductible you select for your renters policy applies to off‑premises claims as well. Choose a deductible that balances affordability with the likelihood of filing a claim for stored items.

If you’re unsure whether your existing policy includes the necessary coverage, you can review the policy documents or contact USAA directly. Many members find it helpful to request a “Proof of Coverage” statement that outlines the exact off‑premises limit. This clarity prevents surprises when you need to file a claim.

Understanding the Role of Endorsements

Endorsements are optional add‑ons that customize a base policy to better fit your lifestyle. For renters who rely heavily on storage units, USAA offers a few relevant endorsements:

- Scheduled Personal Property Endorsement: Allows you to list specific items (e.g., a high‑endurance laptop, a collection of musical instruments, or antique furniture) and assign a value higher than the default 10% off‑premises limit. This is especially useful for items stored long‑term.

- Off‑Premises Personal Property Endorsement: Some insurers, though not always listed explicitly by USAA, provide a broader off‑premises coverage endorsement that can raise the percentage limit from 10% to up to 30% of the total personal property limit.

- Loss of Use Endorsement: Covers additional living expenses if a covered loss forces you to relocate temporarily. While not directly related to storage units, it can be relevant if the loss of stored items disrupts your daily life.

When you add an endorsement, the premium will increase proportionally to the added risk. It’s wise to request a quote that isolates the cost of each endorsement so you can weigh the expense against the potential benefit. For a detailed comparison of policy options, you might explore resources like the Online Car and Home Insurance Quotes – Your Complete Guide, which walks you through evaluating different insurers and endorsements side by side.

Practical Tips for Protecting Your Stored Belongings

Even with the right coverage, proactive steps can reduce the likelihood of a claim and may even lower your premiums. Below are practical measures to safeguard items stored in a unit.

Document Your Inventory

Create a detailed inventory of every item you place in the storage unit. Include photographs, purchase receipts, serial numbers, and estimated values. Store a digital copy of this inventory in a secure cloud service and keep a printed version in a separate location. In the event of loss, a well‑documented inventory speeds up the claims process and helps prove the value of the items.

Choose a Secure Facility

Not all storage units are equal. Look for facilities that provide gated access, 24‑hour video surveillance, on‑site personnel, and individual unit alarms. Some facilities even offer climate‑controlled units, which protect against moisture and temperature extremes—issues that standard renters policies may exclude.

Lock It Right

Use a high‑quality, tamper‑proof lock, such as a disc or cylinder lock, that meets the facility’s specifications. Avoid simple padlocks, as they can be easily cut. Keep the key in a safe place and consider a spare lock for emergencies.

Review the Facility’s Insurance

Many storage facilities carry a limited “facility insurance” that protects against certain perils for the building itself, but not for your personal belongings. Verify the extent of this coverage, and understand that it does not replace your own renters policy.

Update Your Policy When Needed

If you acquire new high‑value items or change the volume of goods stored, contact USAA to adjust your coverage. Adding a scheduled endorsement for a new item is usually a quick process, and it ensures that you’re not underinsured when a loss occurs.

When a Claim Happens: Step‑by‑Step Process

Filing a claim for items lost or damaged in a storage unit follows the same general procedure as a claim for on‑premises losses, but there are a few nuances to keep in mind.

- Secure the Scene: If the loss is due to theft or vandalism, contact law enforcement immediately and obtain a police report. This report will be a critical piece of documentation for your claim.

- Notify USAA Promptly: Most policies require timely notification. USAA’s online portal allows you to start a claim within 24 hours of discovering the loss.

- Submit Documentation: Provide the inventory list, photos, receipts, and the police report. If you have a scheduled endorsement, include the specific policy numbers for the items.

- Assessment: An adjuster may be assigned to evaluate the loss. In many cases, especially for smaller claims, USAA may waive an on‑site visit and rely on the documentation you provide.

- Settlement: Once approved, USAA will issue a payment up to the applicable limit, minus the deductible. If the loss exceeds your off‑premises limit, you’ll need to cover the difference out of pocket or seek additional coverage.

For a smoother claims experience, keep all communications in writing and retain copies of every document you submit. If you encounter any hurdles, USAA’s member service representatives are available to clarify policy language and help you understand the next steps.

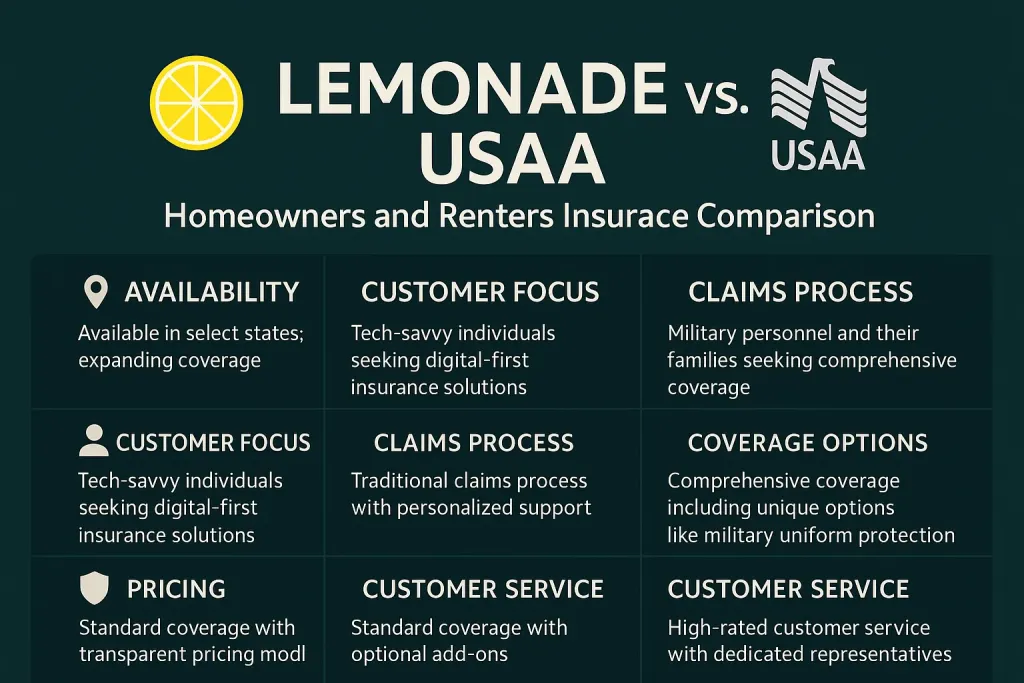

Comparing USAA to Other Renters Insurance Options

While USAA offers competitive rates and strong customer service for military families, other insurers may provide higher off‑premises limits or more flexible endorsements. When evaluating alternatives, consider the following criteria:

- Off‑Premises Percentage: Some insurers automatically cover up to 20% or 30% of the personal property limit for storage units.

- Endorsement Costs: The price of adding a scheduled endorsement can vary widely. Compare the incremental premium against the added coverage value.

- Claims Satisfaction: Look at independent reviews and claim settlement times. USAA consistently ranks high, but a higher coverage limit elsewhere might outweigh a slightly slower process.

- Bundling Discounts: If you also need auto insurance, bundling with the same carrier can lower overall costs.

For a broader perspective on how different policies stack up, the article Does Renters Insurance Cover Storage Units USAA? A Complete Guide provides a side‑by‑side comparison of major insurers and highlights the specific clauses that matter most for storage unit owners.

In summary, the question “does USAA renters insurance cover storage units” receives a nuanced answer. The standard policy does extend coverage to off‑premises belongings, but it caps the limit at 10% of your personal property coverage unless you add endorsements. Understanding the limits, purchasing appropriate add‑ons, and taking proactive steps to protect your items will ensure that your stored belongings are not left vulnerable.

By reviewing your current policy, documenting your inventory, and possibly enhancing coverage through scheduled endorsements, you can bridge the gap between what the policy automatically provides and what you truly need. Whether you stick with USAA or explore other insurers, the goal remains the same: peace of mind that your possessions, even those stored far from home, are financially protected.