Table of Contents

- Understanding the Basics of Credit Card Processing

- Key Terms Every Online Merchant Should Know

- Key Components of an Online Payment Gateway

- Features to Prioritize

- Choosing the Right Processor for Your Business

- 1. Compatibility with Your E‑Commerce Platform

- 2. Pricing Structure

- 3. Customer Support & Dispute Management

- 4. International Acceptance

- Security and Compliance Considerations

- PCI DSS Levels

- Tokenization and Encryption

- Fraud Prevention Tools

- Managing Fees and Optimizing Costs

- Negotiate Interchange‑Plus Rates

- Batch Transactions Promptly

- Reduce Chargebacks

- Leverage Cash‑Back or Reward Programs

- Future Trends in Online Credit Card Processing

- Artificial Intelligence for Fraud Detection

- Buy‑Now‑Pay‑Later (BNPL) Integration

- Cryptocurrency and Stablecoin Payments

- Voice‑Activated Commerce

Credit card processing for online business is a critical backbone that turns casual browsers into paying customers. From the moment a shopper clicks “Buy Now,” a complex choreography of data exchange, security checks, and fund transfers begins. Understanding this workflow helps entrepreneurs avoid costly mistakes, stay compliant, and deliver a seamless checkout experience.

In today’s digital marketplace, consumers expect instant approval, transparent fees, and bullet‑proof security. Failing to meet these expectations can lead to abandoned carts, chargebacks, or even loss of trust. This guide walks you through every stage of the process, from selecting a payment gateway to mastering the nuances of interchange fees, while weaving in real‑world examples and actionable recommendations.

Understanding the Basics of Credit Card Processing

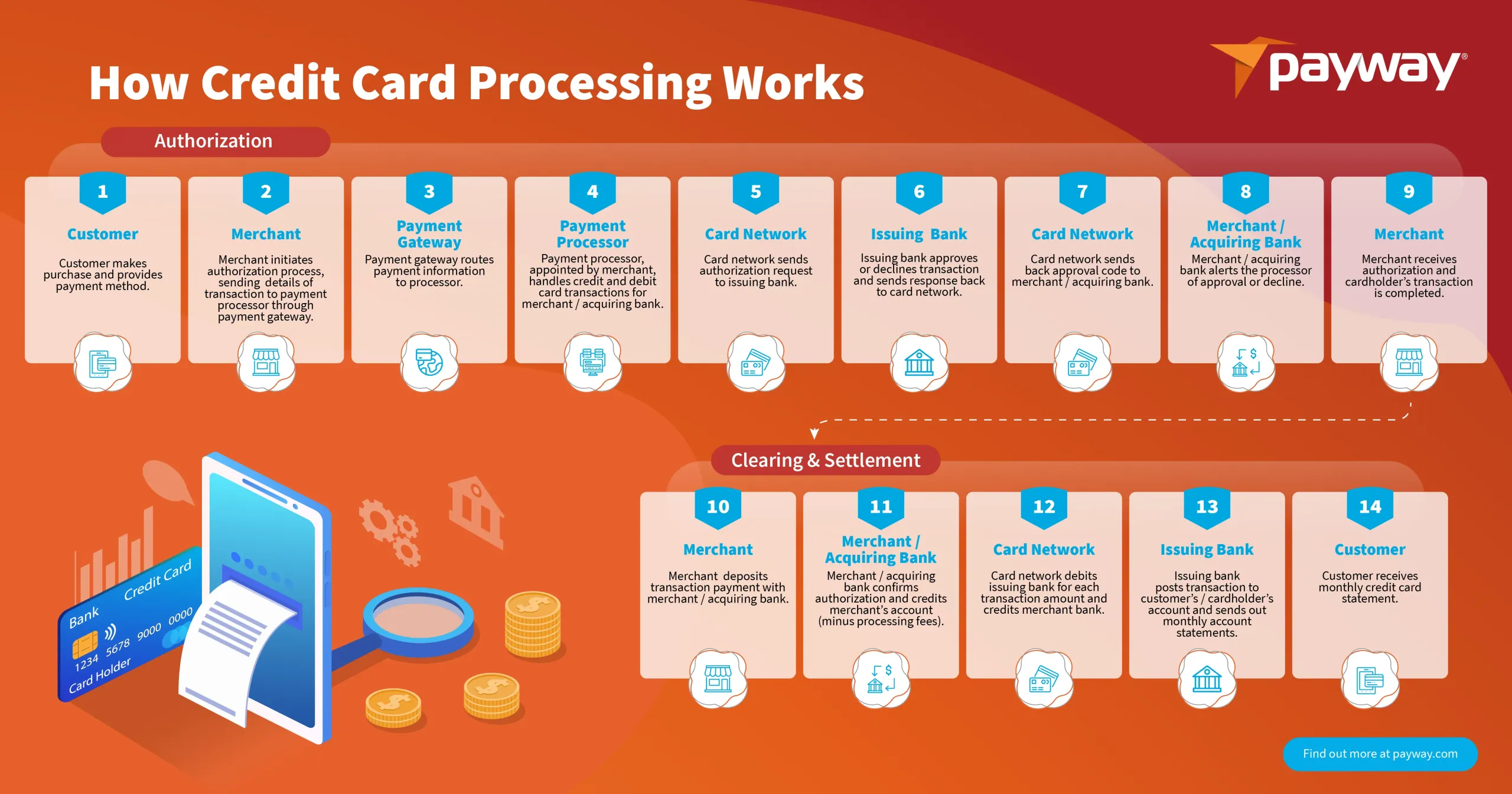

At its core, credit card processing for online business involves three main parties: the merchant (you), the acquiring bank (or merchant account provider), and the issuing bank (the cardholder’s bank). When a customer enters their card details, the information is encrypted and sent to the payment gateway, which then routes the transaction to the acquiring bank. The acquiring bank forwards the request to the card networks (Visa, MasterCard, etc.), which finally contact the issuing bank for authorization.

Once the issuing bank approves, an authorization code is returned, and the transaction is marked as “settled” during the next batch run. Funds are then transferred from the issuing bank to the acquiring bank, and eventually deposited into your merchant account, usually within 1–3 business days.

Key Terms Every Online Merchant Should Know

- Authorization: The temporary hold placed on a cardholder’s funds to ensure availability.

- Capture: The action of moving the authorized amount from the hold to a completed sale.

- Settlement: The final transfer of funds from the issuing bank to the acquiring bank.

- Interchange Fee: A variable fee set by the card networks, paid to the issuing bank.

- Merchant Discount Rate (MDR): The total fee charged to the merchant, typically a blend of interchange, assessment, and processor markup.

Key Components of an Online Payment Gateway

The payment gateway acts as the digital equivalent of a point‑of‑sale terminal. It must securely capture card data, encrypt it, and communicate with the processor. Modern gateways also offer features like recurring billing, fraud detection, and multi‑currency support.

Features to Prioritize

- PCI‑DSS Compliance: Ensures the gateway adheres to the Payment Card Industry Data Security Standard, reducing liability.

- Tokenization: Replaces sensitive card details with a non‑reversible token, allowing safe storage for future transactions.

- 3‑D Secure (3DS): Adds an extra authentication layer, lowering chargeback risk.

- Developer‑Friendly APIs: Enables seamless integration with e‑commerce platforms, shopping carts, and custom sites.

- Transparent Pricing: Flat‑rate, interchange‑plus, or tiered models—choose the one that aligns with your sales volume.

For a deeper dive into merchant relationships and how they influence gateway choices, see our article Understanding Credit Card Merchants.

Choosing the Right Processor for Your Business

Selecting a processor is more than a cost decision; it shapes your customer experience, fraud exposure, and scalability. Below are the primary criteria to evaluate.

1. Compatibility with Your E‑Commerce Platform

Whether you run Shopify, WooCommerce, Magento, or a custom solution, the processor should offer native plugins or robust SDKs. Seamless integration reduces development time and minimizes checkout friction.

2. Pricing Structure

Processors typically present three pricing models:

- Flat‑Rate: A single percentage + fixed fee per transaction (e.g., 2.9% + $0.30). Simple but can be expensive for high‑ticket sales.

- Interchange‑Plus: Actual interchange fee plus a fixed markup (e.g., 0.15% + $0.10). Transparent and often cheaper for larger volumes.

- Tiered: Rates vary based on transaction volume or card type. Requires careful analysis to avoid hidden costs.

3. Customer Support & Dispute Management

A responsive support team can accelerate issue resolution, especially during chargeback disputes. Look for 24/7 live chat, dedicated account managers, and clear escalation paths.

4. International Acceptance

If you sell abroad, verify that the processor supports multi‑currency settlement, local payment methods (Alipay, iDEAL, etc.), and favorable cross‑border fees.

Security and Compliance Considerations

Security breaches not only jeopardize customer data but also expose merchants to hefty fines and reputational damage. Implementing a layered security strategy is non‑negotiable.

PCI DSS Levels

Merchants are categorized into four levels based on annual transaction volume. Even small businesses (Level 4) must complete a Self‑Assessment Questionnaire (SAQ) and maintain secure network configurations.

Tokenization and Encryption

Storing raw card numbers is a major risk. Tokenization replaces them with random strings, while end‑to‑end encryption protects data in transit. Both techniques are often built into modern gateways.

Fraud Prevention Tools

Real‑time risk engines evaluate velocity, IP reputation, and device fingerprinting. Enabling 3‑D Secure can also shift liability away from the merchant in case of fraudulent transactions.

For merchants operating in higher‑risk categories, understanding specific challenges is essential. Check out Understanding the Landscape of High‑Risk Credit Card Processing for specialized insights.

Managing Fees and Optimizing Costs

While processing fees are unavoidable, strategic actions can shrink them considerably.

Negotiate Interchange‑Plus Rates

If your monthly volume exceeds $10,000, many processors are willing to lower their markup. Present clear sales data and ask for a custom rate sheet.

Batch Transactions Promptly

Delaying batch settlements can attract higher assessment fees from card networks. Automate nightly batch runs to stay within the standard settlement window.

Reduce Chargebacks

Every chargeback typically costs $20‑$100 plus the original transaction amount. Clear refund policies, accurate product descriptions, and proactive customer service help keep disputes low.

Leverage Cash‑Back or Reward Programs

Some processors offer rebates based on transaction volume or specific card types. Evaluate whether these programs offset the base fees.

Future Trends in Online Credit Card Processing

The payment landscape evolves quickly, and staying ahead can give your online business a competitive edge.

Artificial Intelligence for Fraud Detection

Machine‑learning models now analyze thousands of data points per transaction, flagging anomalies with higher precision than rule‑based systems.

Buy‑Now‑Pay‑Later (BNPL) Integration

Consumers increasingly favor installment options. Processors that support BNPL providers (e.g., Klarna, Afterpay) can capture higher average order values.

Cryptocurrency and Stablecoin Payments

While still niche, some gateways enable direct crypto settlements, converting digital assets into fiat instantly to mitigate volatility.

Voice‑Activated Commerce

Smart speakers and virtual assistants are becoming checkout channels. Processors that offer APIs compatible with voice platforms will capture early adopters.

By aligning your payment infrastructure with these emerging trends, you not only future‑proof your operation but also open new revenue streams.

Implementing an effective credit card processing solution is a multi‑faceted project that blends technology, finance, and risk management. Start by mapping your sales volume, geographic reach, and security requirements. Then compare processors based on pricing transparency, integration ease, and support quality. Finally, continuously monitor fees, chargeback ratios, and emerging market shifts to keep your checkout experience fast, safe, and profitable.