Table of Contents

- Understanding the Capital One Approval Process

- Key Stages of the Process

- Typical Approval Timeframes

- Factors That Influence Approval Speed

- Credit Score and History

- Debt‑to‑Income Ratio (DTI)

- Recent Credit Activity

- Employment Verification

- Geographic Location

- Application Accuracy

- How to Accelerate Your Capital One Credit Card Approval

- Prepare Your Information in Advance

- Maintain a Clean Credit Profile

- Use the Capital One Mobile App for Real‑Time Updates

- Consider Applying for a Secured Card First

- Leverage Existing Relationships

- What Happens After You’re Approved

- Common Questions About Capital One Approval Times

- Can I Get an Instant Decision Without a Hard Pull?

- What If My Application Is Declined?

- Do Premium Cards Have Longer Approval Times?

- How Does the Approval Time Compare to Other Issuers?

Capital One credit card approval time is a question that many prospective cardholders ask before they even start the application. Knowing the typical waiting period helps you plan purchases, manage expectations, and avoid unnecessary stress. In this article we walk through the entire journey—from the moment you submit your online form to the instant you receive your new card—while highlighting the key variables that can shorten or lengthen the process.

Whether you are applying for a rewards card, a travel‑focused premium product, or a secured card to rebuild credit, the underlying mechanisms that determine approval speed remain largely the same. The difference lies in how your personal financial profile aligns with Capital One’s underwriting criteria. By understanding those criteria, you can make informed decisions that improve your odds of a quick approval.

Understanding the Capital One Approval Process

Capital One, like most major issuers, relies on an automated decision engine backed by a team of human reviewers for borderline cases. The system evaluates a mix of data points that are instantly accessible, such as the credit score pulled from the major bureaus, and information that may require additional verification, like employment history or recent address changes.

The first step is the soft or hard credit inquiry, which occurs the moment you click “Submit.” If the inquiry is soft, it won’t affect your credit score, but most Capital One applications trigger a hard pull. The engine then compares your data against internal risk models. If the model finds a clear match—high credit score, low debt‑to‑income ratio, stable employment—the decision is rendered in seconds. Otherwise, the application may be flagged for manual review, extending the timeline.

Key Stages of the Process

- Data Capture: Your personal details, income, and social security number are collected.

- Credit Pull: A hard inquiry is made to obtain your FICO® score and credit report.

- Automated Scoring: The algorithm checks your profile against preset thresholds.

- Manual Review (if needed): A specialist may verify documents or request additional information.

- Decision Delivery: Approval or denial is communicated via email, SMS, or in‑app notification.

- Card Issuance: Approved applicants receive a temporary digital card instantly; the physical card arrives by mail.

Typical Approval Timeframes

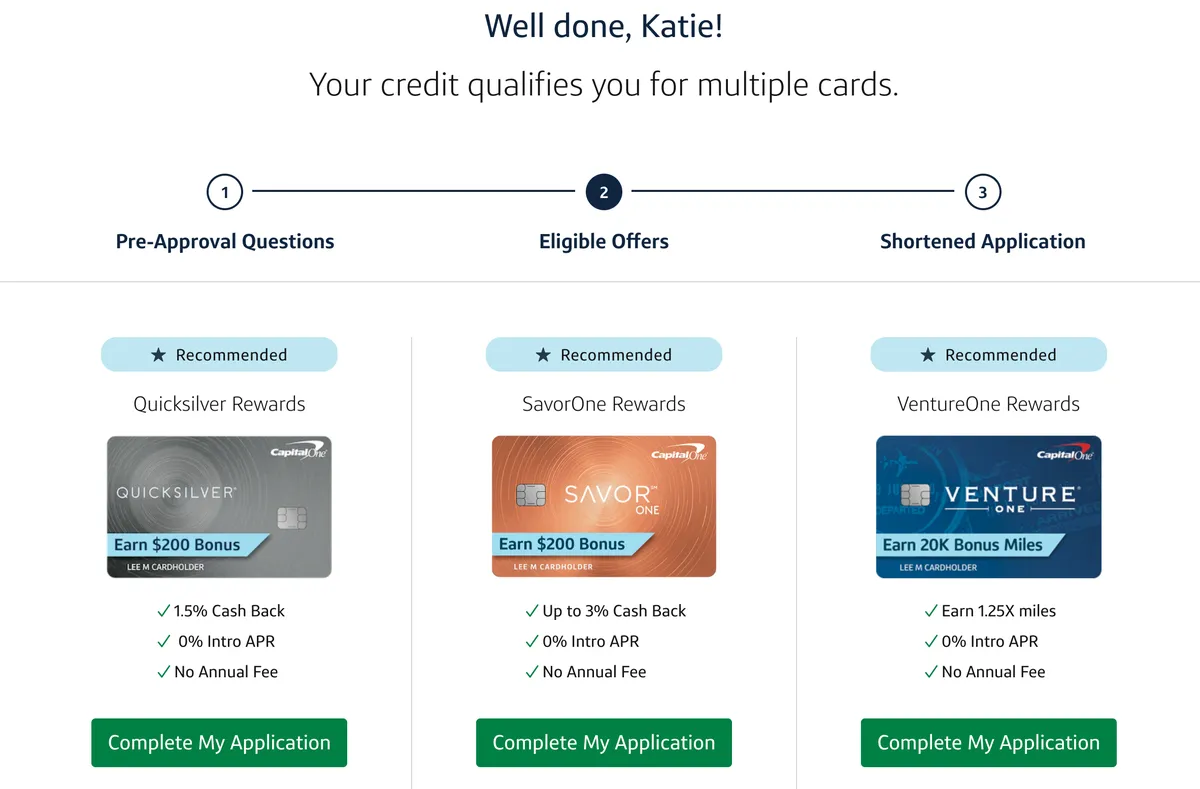

The most common experience for a straightforward application is an immediate decision—often within a few seconds to a couple of minutes after submission. In these cases, Capital One issues an instant virtual card number that can be used for online purchases while you wait for the physical card, which typically arrives within 7‑10 business days.

For applications that trigger a manual review, the timeline expands. According to Capital One’s public disclosures and user reports, the average manual review takes between 24 hours and 5 business days. In rare cases—such as when additional documentation is required from the applicant—the process can extend to two weeks.

It is also worth noting that certain premium cards, like the Capital One Venture X, may have a slightly longer evaluation period due to higher credit limits and more complex reward structures. Nonetheless, the difference is usually measured in hours rather than days.

Factors That Influence Approval Speed

Several variables directly affect how quickly you receive a decision. Understanding these can help you avoid delays.

Credit Score and History

A high credit score (typically 720 or above) signals low risk, allowing the automated system to approve instantly. Conversely, a score below 650 may prompt a manual review, especially if the report shows recent delinquencies.

Debt‑to‑Income Ratio (DTI)

Capital One examines how much of your monthly income is already allocated to debt payments. A low DTI (< 30 %) indicates better repayment capacity and speeds up approval.

Recent Credit Activity

Frequent recent applications or a surge in new accounts can raise red flags. The system may pause to verify that the recent activity is legitimate, adding a few extra hours to the process.

Employment Verification

Applicants who provide a stable employer and a clear income source are less likely to be held for verification. Self‑employed individuals may need to upload tax documents, which can lengthen the timeline.

Geographic Location

Some regions have higher incidences of fraud, prompting extra security checks. This is why applicants from certain zip codes sometimes experience a brief hold.

Application Accuracy

Simple errors—misspelled names, incorrect Social Security numbers, or mismatched addresses—force the system to request clarification, delaying the decision.

How to Accelerate Your Capital One Credit Card Approval

While you cannot control the internal algorithms, you can take proactive steps to streamline the experience.

Prepare Your Information in Advance

- Verify your Social Security number and ensure it matches the one on file with the credit bureaus.

- Gather recent pay stubs or tax returns if you are self‑employed.

- Check that your address is up‑to‑date on all official documents.

Maintain a Clean Credit Profile

Pay down outstanding balances and avoid opening multiple new accounts within a short period. A lower credit utilization ratio (ideally under 30 %) signals responsible credit management.

Use the Capital One Mobile App for Real‑Time Updates

The app provides instant notifications about the status of your application. If a manual review is required, you’ll often receive a prompt to upload any missing documents directly through the app, reducing back‑and‑forth email delays.

Consider Applying for a Secured Card First

If you are building credit, a secured card such as the Capital One Secured Mastercard may receive a quicker decision because the risk is mitigated by the security deposit.

Leverage Existing Relationships

Current Capital One customers who already hold a checking or savings account may experience faster approvals due to the bank’s ability to cross‑verify income and identity.

What Happens After You’re Approved

Once the decision is positive, Capital One immediately generates a digital card number that you can add to your mobile wallet or use for online purchases. This virtual card is fully functional and carries the same credit limit and rewards structure as the physical card.

The physical card is printed and mailed to the address you provided. Capital One typically uses a tracked delivery service for premium cards, offering a delivery window of 7‑10 business days. You can also opt for expedited shipping in some cases, which adds an extra fee but reduces the wait to 2‑3 days.

After receiving the card, you should activate it via the mobile app or the phone line indicated on the card’s sticker. The activation process also serves as a final verification step, confirming that the card has reached the intended recipient.

Common Questions About Capital One Approval Times

Can I Get an Instant Decision Without a Hard Pull?

Capital One offers a soft‑pull pre‑qualification tool that shows whether you are likely to be approved. However, the final decision still requires a hard inquiry.

What If My Application Is Declined?

Capital One will provide a general reason for the decline, such as “insufficient credit history” or “high debt‑to‑income ratio.” You can request a free copy of your credit report to understand the underlying issues.

Do Premium Cards Have Longer Approval Times?

Premium cards may involve a brief additional review to confirm income and spending patterns, but most qualified applicants still receive an instant or same‑day decision.

How Does the Approval Time Compare to Other Issuers?

Capital One’s automated engine is comparable to other major banks like Chase or Citi. In most cases, the speed is similar, with instant approvals for strong profiles and a few days for more complex cases.

For readers interested in the broader context of credit card processing, exploring topics such as high‑risk credit card processing can provide insight into why some issuers take longer to approve certain applications. Likewise, understanding networks like the Discover Network helps illustrate how different payment ecosystems affect card issuance timelines.

In summary, Capital One credit card approval time is largely a function of your credit health and the completeness of your application. By maintaining a strong credit profile, double‑checking your data, and using the mobile app for quick document uploads, you can position yourself for an instant or same‑day approval. Even when a manual review is required, the process rarely exceeds a few business days, allowing you to start enjoying the benefits of your new card without prolonged waiting.