Table of Contents

- Understanding the Disney Premier Visa Card

- Eligibility and Credit Score Requirements

- How the Card Impacts Your Credit Profile

- Credit Score Mechanics Behind the Disney Premier Visa

- Score Ranges and Approval Odds

- The Role of Credit Utilization and History

- Strategies to Improve Your Score Before Applying

- Paying Down Balances

- Building a Positive Payment History

- Diversifying Credit Types

- Limit New Inquiries

- Utilize Credit‑Building Tools

- What Happens After You Get the Card

- Reporting to Credit Bureaus

- Rewards and Their Effect on Credit Utilization

- Annual Fee and Its Impact

- Common Misconceptions and FAQs

The Disney Premier Visa Card offers fans a magical way to earn rewards while enjoying Disney experiences, but its allure comes with a practical gatekeeper: the credit score. Understanding the disney premier visa card credit score relationship is essential for anyone considering this card, whether you are a seasoned Disney enthusiast or a first‑time applicant. This article walks you through the mechanics behind the card’s approval process, how it affects your credit profile, and proven strategies to improve your score before you apply.

Imagine stepping into a Disney park with a special card that instantly translates your purchases into exclusive perks, from complimentary MagicBands to discounts on merchandise. While the fantasy is enticing, the reality is grounded in the numbers that lenders use to gauge risk. Your credit score—an aggregated snapshot of your borrowing habits—determines not only whether you receive the card but also the terms you receive.

In the following sections, we will explore the card’s eligibility criteria, the nuances of credit reporting, and practical steps to align your financial habits with Disney’s expectations. By the end, you’ll have a clear roadmap to navigate the Disney Premier Visa Card’s credit requirements without relying on guesswork.

Understanding the Disney Premier Visa Card

Eligibility and Credit Score Requirements

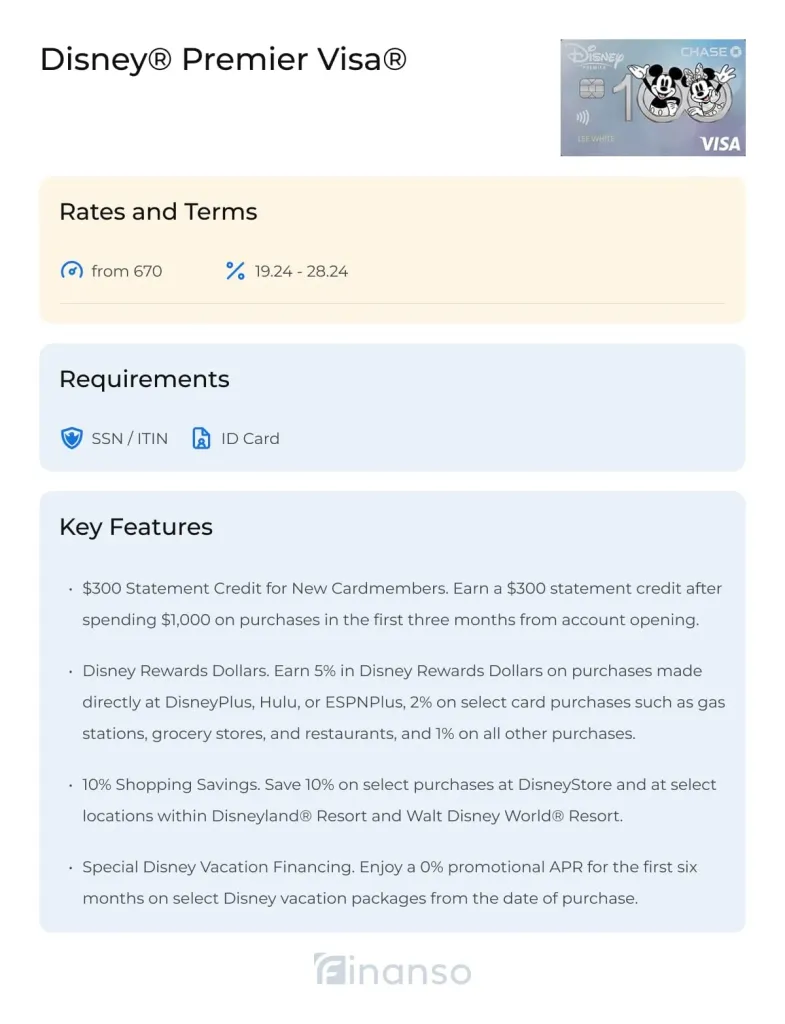

The Disney Premier Visa Card, issued by Chase, is positioned as a premium rewards card targeting consumers with strong credit histories. While Chase does not publicly disclose an exact score threshold, industry data suggests that successful applicants typically possess a FICO score of 700 or higher. This range places you in the “good” to “excellent” category, indicating reliable repayment behavior and low default risk.

Beyond the numeric score, Chase evaluates additional factors:

- Credit utilization: The ratio of your revolving balances to total credit limits. Keeping this below 30 % signals prudent credit management.

- Payment history: A record of on‑time payments across all credit accounts, with particular emphasis on the past 12‑month window.

- Length of credit history: Longer histories provide more data points for risk assessment.

- Recent inquiries: Multiple hard inquiries within a short period may raise concerns about credit shopping.

How the Card Impacts Your Credit Profile

Obtaining the Disney Premier Visa Card initiates a hard inquiry on your credit report, which can temporarily lower your score by a few points. However, the long‑term impact depends on how you manage the account:

- Maintaining low utilization on the card contributes positively to your overall credit utilization ratio.

- Consistently paying the balance in full each month reinforces a strong payment history.

- Increasing total available credit, while keeping balances low, can improve the average age of accounts over time.

These factors collectively shape the narrative that credit bureaus present to future lenders, making responsible usage a key component of your financial story.

Credit Score Mechanics Behind the Disney Premier Visa

Score Ranges and Approval Odds

Credit scoring models, such as FICO and VantageScore, assign points based on five primary categories. For the Disney Premier Visa Card, the most influential categories are payment history (35 %) and credit utilization (30 %). Below is a rough mapping of score ranges to approval probability:

- 720‑850 (Excellent): 85‑95 % chance of approval.

- 690‑719 (Good): 60‑80 % chance, often contingent on other strong factors.

- 660‑689 (Fair): 30‑55 % chance; applicants may need additional assets or a co‑signer.

- Below 660 (Poor): Unlikely to be approved without substantial compensating factors.

The Role of Credit Utilization and History

Utilization is calculated per revolving account and across all accounts combined. For instance, if you have a total credit limit of $10,000 and a balance of $2,800, your overall utilization stands at 28 %, comfortably below the 30 % benchmark.

Moreover, the age of your oldest account contributes to the “length of credit history” factor. Even if you have a high score, a very recent credit file (e.g., less than two years) may reduce approval odds because the model has fewer data points to verify consistency.

Strategies to Improve Your Score Before Applying

Paying Down Balances

Reducing existing revolving balances is the quickest way to lower your utilization ratio. Focus first on high‑interest credit cards, as paying them off not only improves your score but also reduces overall debt costs.

Building a Positive Payment History

Set up automatic payments for at least the minimum due date on all accounts. Even a single missed payment can drop your score by 100 points or more, especially if the delinquency exceeds 30 days.

Diversifying Credit Types

Credit mix accounts for 10 % of a FICO score. If your portfolio consists solely of credit cards, consider adding a small installment loan (e.g., an auto loan or a personal loan) and managing it responsibly. This diversification demonstrates your ability to handle varied credit products.

Limit New Inquiries

Each hard inquiry stays on your report for two years, but its impact diminishes after six months. Plan your applications strategically: avoid multiple credit checks within a short window, and space out major applications (e.g., mortgage, auto loan) from your Disney Premier Visa Card request.

Utilize Credit‑Building Tools

Services like Discover network can help you monitor your credit in real time, providing alerts for changes that could affect your score. Staying informed enables you to act swiftly on any negative entries.

What Happens After You Get the Card

Reporting to Credit Bureaus

Chase reports your account activity to the three major bureaus—Equifax, Experian, and TransUnion—once per month, typically on the statement closing date. This regular reporting means any changes in utilization or balance are reflected promptly in your credit file.

Rewards and Their Effect on Credit Utilization

The Disney Premier Visa Card offers points on Disney purchases, dining, and travel. While rewards are appealing, it’s crucial not to let the lure of points drive you to overspend. Higher balances increase utilization, which can negate the benefits of earned points by harming your credit score.

Annual Fee and Its Impact

The card carries an annual fee (as of 2026, $95). Paying this fee on time does not affect your score directly, but neglecting to pay it could lead to missed payments, triggering negative marks. Treat the fee like any other recurring bill and incorporate it into your budget.

Common Misconceptions and FAQs

- “I need a perfect 850 score to qualify.” Not true. While higher scores improve odds, a well‑managed credit profile with a score in the 700‑730 range is often sufficient.

- “Opening the card will instantly boost my score.” The initial hard inquiry may cause a slight dip. Long‑term benefits arise only from responsible usage.

- “My Disney spending alone can raise my score.” Spending at Disney locations earns points, but the score is driven by payment behavior and utilization, not merchant categories.

- “I can cancel the card if my score drops.” You can close the account, but closing a revolving account may increase overall utilization, potentially lowering your score further.

For businesses and high‑risk merchants navigating credit card processing, understanding how credit scores influence card acceptance can be pivotal. A deeper dive into such topics is explored in Credit Card Processing for High‑Risk Merchants: Choosing the Right Partner and Reducing Fees, which provides insight into risk management strategies that parallel personal credit considerations.

In summary, securing the Disney Premier Visa Card is less about a single numeric threshold and more about presenting a holistic picture of credit responsibility. By managing existing debts, maintaining timely payments, and approaching new credit with strategic intent, you can position yourself favorably for approval and enjoy the magical perks the card offers without compromising your financial health.