Table of Contents

- Understanding High‑Risk Merchant Classification

- Key Challenges in High‑Risk Credit Card Processing

- Higher Chargeback Rates

- Regulatory Scrutiny

- Limited Banking Options

- Choosing the Right Processor

- Assessing Reputation and Experience

- Evaluating Fee Structures

- Looking for Specialized Support

- Essential Features for High‑Risk Processing

- Chargeback Management Tools

- Fraud Prevention Solutions

- Flexible Settlement Terms

- Best Practices to Reduce Risk

- Implement Robust KYC & AML Procedures

- Maintain Transparent Refund Policies

- Monitor Transaction Patterns

- Cost Structure and Pricing Models

- Flat‑Rate vs. Tiered Pricing

- Monthly Fees and Minimums

- Rolling Reserves

- Legal and Compliance Considerations

- PCI DSS Compliance

- State Licensing and Industry Regulations

- Industry‑Specific Rules

- Future Trends for High‑Risk Processing

- Tokenization and Encryption Advances

- AI‑Driven Fraud Detection

- Alternative Payment Methods

- Putting It All Together: A Practical Checklist

Credit card processing for high‑risk merchants has long been a complex puzzle, especially when the stakes involve higher chargeback rates and stricter regulations. In this article we follow the journey of a fictitious e‑commerce store that sells subscription‑based supplements—an industry often labeled high‑risk—and explore the decisions it makes to secure reliable payment processing.

From the moment the owner realizes that traditional banks are reluctant to provide a merchant account, the need for specialized solutions becomes clear. By breaking down the challenges, evaluating providers, and implementing best practices, the story illustrates how high‑risk businesses can thrive without sacrificing cash flow or customer trust.

Understanding High‑Risk Merchant Classification

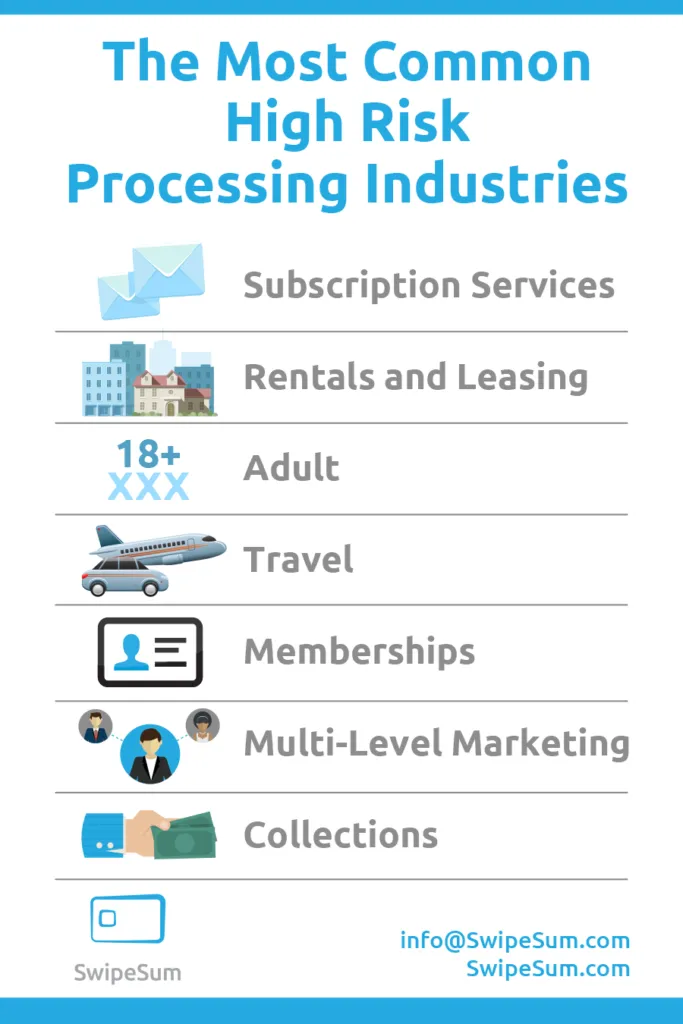

High‑risk merchants are defined by the likelihood of chargebacks, fraud, or regulatory scrutiny. Industries such as online gaming, travel, nutraceuticals, and adult entertainment frequently fall into this category. The classification is not a permanent label; it reflects risk factors that can be mitigated with proper controls.

In our example, the supplement store is flagged because of recurring billing and the potential for disputed health claims. This triggers a series of questions for the owner: Which processors accept this business model? What fees will be charged? And how can the store protect itself from future disputes?

Key Challenges in High‑Risk Credit Card Processing

Higher Chargeback Rates

- Chargebacks can exceed 1% of transactions, surpassing the thresholds most banks deem acceptable.

- Frequent disputes increase the risk of account termination.

- Processors often require merchants to maintain a chargeback reserve.

Regulatory Scrutiny

- Compliance with the PCI DSS is mandatory, but high‑risk merchants may also need additional licensing.

- State and federal agencies monitor industries prone to fraud, adding layers of documentation.

Limited Banking Options

- Traditional acquiring banks may refuse to underwrite high‑risk accounts.

- Alternative processors specialize in high‑risk verticals but often charge higher rates.

Choosing the Right Processor

Assessing Reputation and Experience

When the supplement store begins its search, it reviews providers that have a proven track record with recurring billing models. A reputable processor will have transparent policies, clear communication channels, and documented case studies.

Evaluating Fee Structures

Fees for high‑risk merchants typically include a higher interchange‑plus rate, monthly minimums, and reserve requirements. The owner compares a flat‑rate model versus a tiered structure, ensuring that projected monthly volume aligns with the chosen plan.

Looking for Specialized Support

Dedicated account managers who understand the nuances of high‑risk verticals can make a significant difference. They help navigate compliance, set up fraud filters, and provide chargeback dispute assistance.

Essential Features for High‑Risk Processing

Chargeback Management Tools

Automated dispute filing and real‑time alerts enable merchants to respond quickly. The supplement store adopts a platform that integrates directly with its order management system, reducing response time from days to minutes.

Fraud Prevention Solutions

- Address Verification Service (AVS) checks

- Card Verification Value (CVV) verification

- Machine‑learning risk scoring that flags suspicious patterns

Flexible Settlement Terms

High‑risk processors may hold funds for 7‑14 days. Negotiating shorter settlement cycles can improve cash flow, especially for subscription businesses that rely on predictable revenue streams.

Best Practices to Reduce Risk

Implement Robust KYC & AML Procedures

Know Your Customer (KYC) and Anti‑Money Laundering (AML) checks verify the identity of purchasers, lowering the chance of fraudulent orders. The store integrates a verification step that confirms billing addresses against cardholder data.

Maintain Transparent Refund Policies

Clear, prominently displayed return policies help set customer expectations and can be used as evidence during chargeback disputes. The owner adds a FAQ section that outlines the 30‑day refund window and required documentation.

Monitor Transaction Patterns

Regularly reviewing sales spikes, geographic anomalies, and repeat chargebacks allows early detection of problem areas. The store uses a dashboard that highlights transactions exceeding a set risk score.

Cost Structure and Pricing Models

Flat‑Rate vs. Tiered Pricing

Flat‑rate pricing offers simplicity—e.g., 3.5% + $0.30 per transaction—but may become costly as volume grows. Tiered pricing adjusts rates based on transaction volume, rewarding higher sales with lower percentages.

Monthly Fees and Minimums

Many high‑risk processors impose a $25‑$50 monthly fee and a minimum processing volume. If the store’s monthly sales dip below the minimum, the fee ensures the processor covers its risk exposure.

Rolling Reserves

A reserve is a percentage of each transaction held for a set period (often 90 days). This protects the processor against future chargebacks. The store negotiates a 5% rolling reserve, which is released once the transaction history proves stable.

Legal and Compliance Considerations

PCI DSS Compliance

All merchants handling cardholder data must meet PCI DSS requirements. The supplement store adopts a tokenization solution that replaces sensitive data with non‑reversible tokens, minimizing the scope of PCI audits.

State Licensing and Industry Regulations

Some states require specific licenses for selling dietary supplements. The owner consults legal counsel to ensure compliance with both federal and state regulations, avoiding costly fines.

Industry‑Specific Rules

Payment networks may impose additional rules for recurring billing, such as obtaining explicit consent for each billing cycle. The store updates its checkout flow to capture recurring consent, storing the proof for future reference.

Future Trends for High‑Risk Processing

Tokenization and Encryption Advances

Emerging tokenization standards promise even greater security, allowing merchants to store transaction data without exposing card numbers. This reduces PCI scope and lowers the risk of data breaches.

AI‑Driven Fraud Detection

Artificial intelligence models analyze millions of data points in real time, spotting anomalies that traditional rules‑based systems miss. Early adopters report a 20‑30% reduction in false positives, improving approval rates.

Alternative Payment Methods

Digital wallets, ACH, and even cryptocurrency are gaining traction among high‑risk merchants looking to diversify payment options. Offering these alternatives can attract customers who prefer non‑card methods, potentially lowering overall chargeback risk.

Putting It All Together: A Practical Checklist

- Identify your industry’s risk factors and document them.

- Research processors with proven experience in your vertical.

- Compare fee structures, focusing on interchange‑plus rates, reserves, and monthly minimums.

- Implement robust KYC/AML checks and transparent refund policies.

- Choose a solution that offers chargeback automation and AI‑driven fraud detection.

- Maintain PCI DSS compliance through tokenization and regular security audits.

- Monitor transaction trends and adjust risk parameters as needed.

- Stay informed about emerging technologies such as tokenization and digital wallets.

By following this roadmap, the supplement store transitions from a precarious position—facing potential account shutdown—to a stable, compliant, and profitable operation. The journey illustrates that, while credit card processing for high‑risk merchants presents unique obstacles, the right combination of technology, expertise, and disciplined practices can turn those challenges into sustainable growth.

Entrepreneurs looking to solidify their financial foundations often start by establishing a reliable banking relationship. For those who need to open a business bank account online, the process can be streamlined with modern fintech platforms, providing the necessary backbone for high‑risk payment processing.

Understanding related financial services, such as how a lockbox at a bank works, can further enhance cash management and reduce reconciliation errors—critical for businesses handling large volumes of recurring payments.

Finally, while the focus here is on high‑risk merchant processing, many businesses also benefit from strategic credit card use in other areas, such as optimizing travel expenses with a business travel credit card. Integrating these tools creates a holistic financial ecosystem that supports growth across all facets of the enterprise.