Table of Contents

- Why Open a Business Bank Account Online?

- Convenience and Speed

- Regulatory Compliance Made Simpler

- Access to Digital Financial Tools

- Eligibility Requirements and Documentation

- Business Structure and EIN

- Personal Identification

- Proof of Business Address and Operational Details

- Step‑by‑Step Process to Open the Account

- Choose the Right Bank

- Complete the Online Application

- Verify Identity

- Fund the Account

- Common Pitfalls and How to Avoid Them

- Incomplete Documentation

- Choosing the Wrong Account Type

- Neglecting Security Practices

- Maximizing the Benefits of Your Online Business Account

- Integrate Accounting Software

- Utilize Cash Management Tools

- Leverage Business Credit Options

Opening up a business bank account online has become a cornerstone of modern entrepreneurship. In today’s fast‑paced digital economy, the ability to establish a legitimate financial gateway without stepping foot in a physical branch can save hours, reduce costs, and streamline cash flow management from day one. This article walks you through every critical facet of the process, from understanding why an online account matters to mastering the final verification steps.

The journey begins with a clear purpose: separating personal and business finances, complying with tax regulations, and unlocking tools that can accelerate growth. While the concept sounds straightforward, the reality involves navigating regulatory requirements, selecting the right banking partner, and preparing a precise set of documents. By the end of this guide, you’ll have a practical roadmap that turns the abstract idea of “online business banking” into a tangible, operational account.

For entrepreneurs seeking a deeper dive, the definitive guide to fast‑track your online business bank account offers additional strategies for rapid onboarding, while the fast‑track guide to set up a business bank account online highlights common mistakes to avoid. Let’s start by exploring the core motivations behind moving your banking operations to the cloud.

Why Open a Business Bank Account Online?

Convenience and Speed

Traditional banking often requires multiple visits, paperwork, and waiting periods that can stretch for weeks. Online platforms compress this timeline dramatically. Most reputable banks now offer a fully digital onboarding flow that can be completed in under an hour, provided you have the necessary documentation ready. The convenience extends beyond the initial setup; everyday tasks such as checking balances, initiating transfers, or ordering checks are all performed through secure web portals or mobile apps.

Regulatory Compliance Made Simpler

Separating personal and business finances is not just good practice—it is a legal requirement for many tax jurisdictions. An online business account automatically tags transactions with your business’s EIN (Employer Identification Number), simplifying bookkeeping and audit trails. Moreover, digital banks are required to adhere to the same anti‑money‑laundering (AML) and Know‑Your‑Customer (KYC) standards as brick‑and‑mortar institutions, ensuring that compliance is baked into the onboarding workflow.

Access to Digital Financial Tools

Modern online banks integrate seamlessly with accounting software like QuickBooks, Xero, and FreshBooks. These integrations automate transaction categorization, generate real‑time financial statements, and even predict cash‑flow gaps. In addition, many platforms provide built-in invoicing, payroll processing, and expense management modules, turning a simple deposit account into an all‑in‑one financial hub for your enterprise.

Eligibility Requirements and Documentation

Business Structure and EIN

Before you can click “Submit,” you must determine the legal structure of your business—sole proprietorship, LLC, corporation, or partnership. Each structure has distinct documentation requirements. For most entities, the primary identifier is the Employer Identification Number (EIN), which you can obtain for free from the IRS. Banks will request the EIN to link the account to your legal entity and to verify tax obligations.

Personal Identification

Even though the account is for a business, banks still need to confirm the identity of the individuals who will have signing authority. Acceptable forms of ID include a passport, driver’s license, or state‑issued ID card. Some institutions also require a recent utility bill or bank statement to confirm the applicant’s residential address.

Proof of Business Address and Operational Details

A virtual office or coworking space can serve as a legitimate business address for most banks, provided you can furnish a lease agreement or a utility bill in the company’s name. Additionally, banks often ask for a brief description of your primary business activities, projected monthly transaction volume, and anticipated average balance. This information helps the bank assess risk and tailor services to your needs.

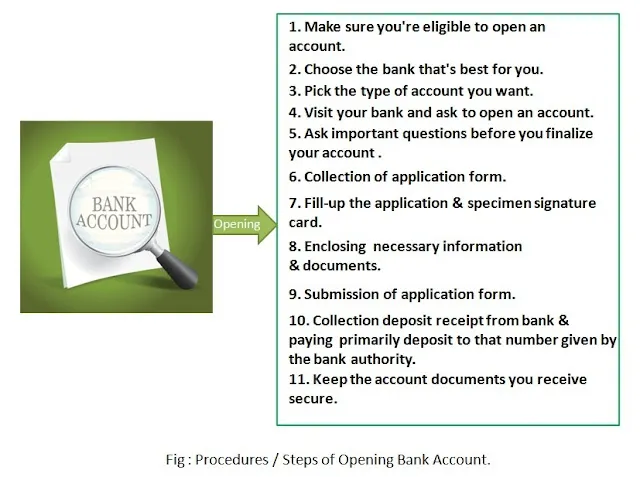

Step‑by‑Step Process to Open the Account

Choose the Right Bank

Not all online banks are created equal. Evaluate factors such as monthly fees, transaction limits, integration capabilities, and customer support. Some banks specialize in serving startups and tech companies, offering perks like free wire transfers or higher cash‑deposit limits. Review the fast‑track guide to opening a business bank account online to compare providers side by side.

Complete the Online Application

The application typically begins with basic business details: legal name, DBA (Doing Business As) if applicable, EIN, and industry classification (NAICS code). You’ll also be asked to upload scanned copies of your incorporation documents, operating agreement, or partnership agreement. A clean, organized PDF file set speeds up the review process.

Verify Identity

After submitting the application, the bank will initiate a KYC check. This may involve a short video call, a selfie‑with‑ID verification, or a third‑party verification service. The goal is to confirm that the person opening the account is indeed authorized to do so. Successful verification unlocks full access to the account dashboard.

Fund the Account

Most banks require an initial deposit to activate the account. This can be done via ACH transfer from an existing personal account, a wire, or even a debit card transaction. Some platforms allow you to fund the account using a linked PayPal or Stripe account, providing flexibility for businesses that operate primarily online.

Common Pitfalls and How to Avoid Them

Incomplete Documentation

Missing or mismatched documents are the leading cause of application delays. Double‑check that the name on your EIN matches the legal name on your incorporation papers. Ensure all scanned files are legible and in PDF format. A quick pre‑submission audit can prevent back‑and‑forth requests that extend the onboarding timeline.

Choosing the Wrong Account Type

Many banks offer multiple account tiers—basic checking, premium checking, and treasury services. Selecting a basic account for a high‑volume e‑commerce business may lead to excessive transaction fees. Conversely, a premium account with high minimum balances might drain resources from a bootstrapped startup. Align the account features with your projected cash flow and transaction needs.

Neglecting Security Practices

Digital banking introduces new security considerations. Enable multi‑factor authentication (MFA) on every device, regularly update passwords, and monitor account activity through alerts. Some banks provide virtual cards for online purchases, reducing exposure of the primary account number. Treat your online business account with the same vigilance you would a physical vault.

Maximizing the Benefits of Your Online Business Account

Integrate Accounting Software

Link your new account to accounting platforms to automate transaction imports. This reduces manual data entry and minimizes errors. Real‑time syncing also enables you to generate profit‑and‑loss statements, balance sheets, and cash‑flow forecasts with a single click.

Utilize Cash Management Tools

Many online banks offer sweep accounts, which automatically move excess funds into interest‑bearing accounts overnight. Others provide automated payment scheduling, allowing you to set up recurring vendor payments or payroll runs. These tools improve liquidity and ensure you never miss a critical deadline.

Leverage Business Credit Options

Once your account demonstrates consistent activity, banks may extend a line of credit or offer a business credit card. These credit products are often tied to your transaction history, meaning a well‑managed online account can unlock favorable terms faster than a traditional credit review process. Use the credit responsibly to finance inventory, marketing campaigns, or equipment purchases.

In summary, opening up a business bank account online is no longer a futuristic concept; it’s a practical, efficient solution for today’s entrepreneurs. By understanding eligibility, gathering accurate documentation, and following a systematic application process, you can secure a digital banking relationship that supports growth, compliance, and financial insight. Remember to choose a bank that aligns with your operational needs, avoid common missteps, and fully exploit the digital tools at your disposal. With the right approach, your online business account will become a strategic asset, powering everything from day‑to‑day cash flow to long‑term expansion plans.