Table of Contents

- Defining the Clear Access Banking Account

- Key Features That Distinguish Clear Access Accounts

- Technology Behind Clear Access Banking

- Open‑Banking and API Integration

- Regulatory Landscape and Consumer Protection

- Impact on Financial Inclusion

- Practical Benefits for Consumers

- Real‑World Example: Integration with Investment Services

- Challenges and Considerations

- Future Outlook

In today’s rapidly evolving financial landscape, the term “clear access banking account” has begun to surface in conversations among tech‑savvy consumers and industry insiders alike. At its core, a clear access banking account is a type of deposit account designed to provide transparent, frictionless entry to banking services while leveraging digital tools to enhance user experience. This article unpacks the definition, underlying technology, regulatory considerations, and practical advantages of such accounts, guiding readers through a comprehensive understanding of the concept.

Imagine a scenario where opening a new bank account is as simple as tapping a button on a smartphone, with no hidden fees, ambiguous terms, or unnecessary paperwork. That vision aligns closely with the promise of clear access banking. By prioritizing clarity and accessibility, these accounts aim to remove traditional barriers that have long complicated the banking relationship, especially for underserved populations. As we delve deeper, you’ll see how clear access banking accounts differ from conventional accounts and why they matter in a world increasingly driven by data and connectivity.

Before we jump into the specifics, it’s useful to consider how digital transformation has already reshaped the banking sector. From mobile‑first applications to open‑banking APIs, technology has opened doors that were once locked behind physical branches and complex approval processes. Clear access banking builds on this momentum, marrying regulatory compliance with user‑centric design to create a banking product that feels both modern and trustworthy.

Defining the Clear Access Banking Account

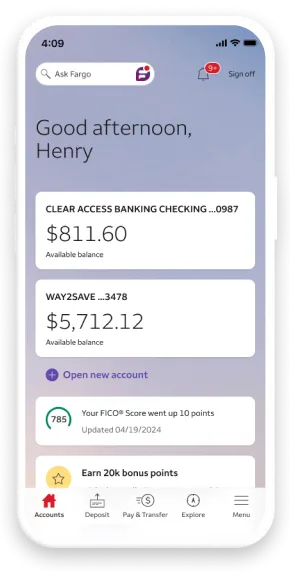

A clear access banking account can be defined as a deposit account—often a checking or savings product—offered by a financial institution that emphasizes three core principles: transparency, ease of entry, and digital accessibility. Unlike traditional accounts that may hide fees in fine print or require extensive in‑person verification, clear access accounts are structured to provide:

- Transparent fee structures: All costs are disclosed up front, with no surprise charges.

- Simple onboarding: Account opening can be completed online or via a mobile app, often within minutes.

- Digital‑first access: Full account management through secure web portals or apps, including real‑time transaction monitoring.

These attributes are not merely marketing buzzwords; they reflect a concrete shift toward consumer empowerment. By delivering clear, predictable terms, banks aim to build trust and reduce the friction that traditionally deters potential customers.

Key Features That Distinguish Clear Access Accounts

- Zero or Low Minimum Balance Requirements: Many clear access accounts remove the burden of maintaining a high minimum balance, making them attractive to students, freelancers, and low‑income users.

- Real‑Time Alerts and Notifications: Users receive instant push notifications for deposits, withdrawals, and potential overdrafts, fostering better financial awareness.

- Integrated Financial Tools: Budgeting widgets, spending categorization, and goal‑setting features are often embedded directly within the banking app.

- Open‑Banking Compatibility: APIs allow seamless data sharing with third‑party financial apps, enhancing the ecosystem of services available to account holders.

- Regulatory Safeguards: Despite their simplicity, clear access accounts remain fully FDIC‑insured (in the United States) and comply with AML/KYC regulations, ensuring consumer protection.

Technology Behind Clear Access Banking

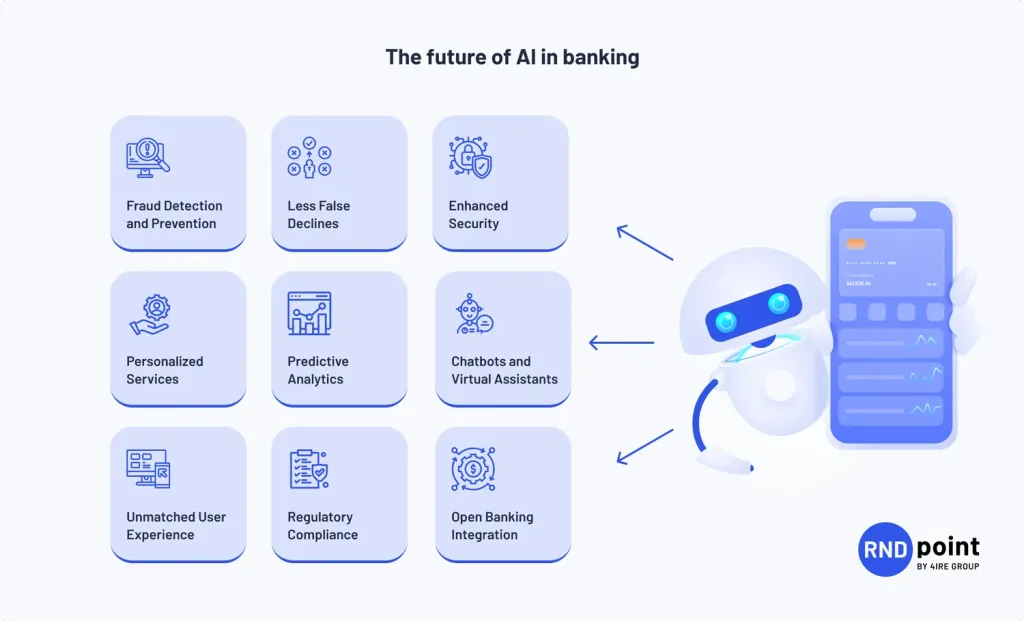

The seamless experience promised by clear access accounts rests on a stack of modern technologies. Cloud computing, AI‑driven identity verification, and robust cybersecurity measures form the backbone of these products. By migrating core banking functions to the cloud, institutions can scale services rapidly while maintaining high availability and low latency for end‑users.

Artificial intelligence plays a crucial role in the onboarding process. Machine‑learning models analyze documents, facial recognition data, and behavioral cues to verify identities in seconds—a stark contrast to the days‑long manual reviews that characterized legacy banking. This rapid verification not only speeds up account creation but also reduces operational costs for the bank.

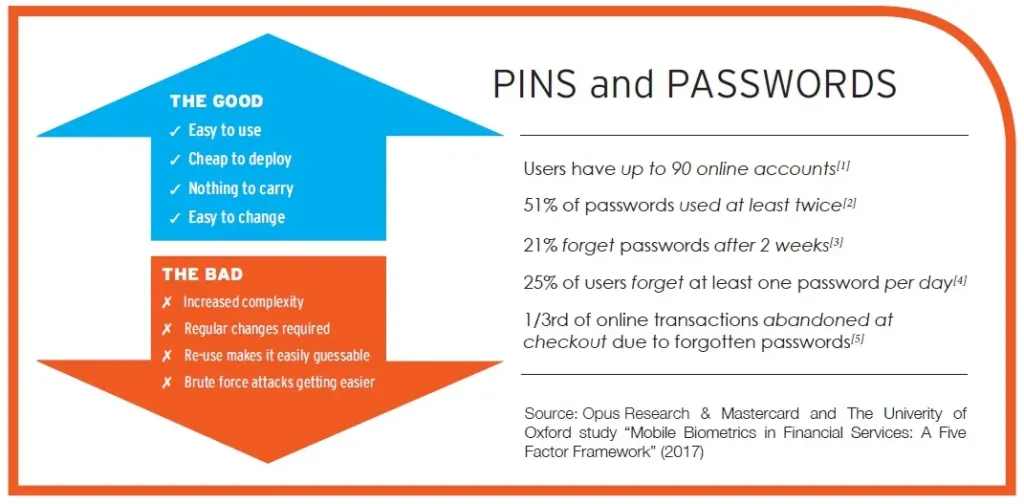

Security, however, remains paramount. End‑to‑end encryption, multi‑factor authentication (MFA), and continuous threat monitoring are standard practices. In addition, tokenization of sensitive data—replacing actual account numbers with random tokens—mitigates the risk of data breaches, ensuring that even if a breach occurs, the exposed information is useless to attackers.

Open‑Banking and API Integration

One of the most powerful enablers of clear access banking is the rise of open‑banking standards. By exposing secure APIs, banks allow third‑party developers to build applications that can read account balances, initiate payments, or offer personalized financial advice—all with the user’s explicit consent. This ecosystem approach creates a vibrant marketplace of services, turning a simple deposit account into a hub for financial wellbeing.

For example, a user might link their clear access account to a budgeting app that automatically categorizes expenses and suggests ways to save. Because the underlying data is shared through standardized APIs, the integration is smooth and reliable, providing a cohesive experience across platforms.

Regulatory Landscape and Consumer Protection

While the allure of streamlined, digital banking is strong, regulators worldwide are vigilant in ensuring that consumer rights are protected. Clear access banking accounts must adhere to a variety of regulations, including:

- Bank Secrecy Act (BSA) and Anti‑Money Laundering (AML) requirements: Institutions must implement robust monitoring to detect suspicious activity.

- Know Your Customer (KYC) standards: Even with rapid digital verification, banks must collect sufficient information to verify identity and assess risk.

- Consumer Financial Protection Bureau (CFPB) guidelines: Transparent disclosure of fees and terms is mandated, aligning perfectly with the clear access ethos.

- Data protection laws such as GDPR (EU) and CCPA (California): These govern how personal data is collected, stored, and shared, influencing the design of APIs and consent mechanisms.

Compliance is not an afterthought; it is integrated into the product design from the outset. Automated compliance tools scan transactions for red flags, while audit trails ensure that every action can be traced back to a responsible party, satisfying both regulators and customers.

Impact on Financial Inclusion

One of the most compelling arguments for clear access banking is its potential to advance financial inclusion. By eliminating high minimum balances and simplifying onboarding, these accounts become accessible to individuals who have historically been marginalized by traditional banking models. The result is a broader base of “banked” consumers who can participate in the digital economy, access credit, and build financial histories.

Studies have shown that individuals with a clear, low‑cost account are more likely to save regularly and less likely to rely on costly payday loans. This shift not only improves personal financial health but also contributes to macro‑economic stability by expanding the pool of consumers who can engage in formal financial activities.

Practical Benefits for Consumers

From a user perspective, the advantages of a clear access banking account are tangible and varied. Below are some of the most notable benefits:

- Cost Predictability: With all fees disclosed upfront, users can budget without fearing hidden charges.

- Speed and Convenience: Opening an account can be completed in under ten minutes from a smartphone.

- Enhanced Financial Literacy: Integrated tools help users understand spending patterns and set savings goals.

- Seamless Integration: API connectivity enables linking to investment platforms, such as Merrill Edge, or savings boosters like the Bank of Montreal Savings Builder account. For a deeper look at how a savings builder can supercharge your savings, read Discover How the Bank of Montreal Savings Builder Account Can Supercharge Your Savings.

- Security Confidence: Advanced encryption and tokenization reduce exposure to fraud.

These features collectively empower users to manage money more effectively, reduce financial stress, and pursue long‑term goals with confidence.

Real‑World Example: Integration with Investment Services

Consider a customer who wants to consolidate banking and investing. By linking a clear access checking account with a brokerage platform like Merrill Edge, they can move funds instantly to seize market opportunities. The synergy is highlighted in the guide Unlock the Full Potential of Merrill Edge and Bank of America – Your Ultimate Guide, which demonstrates how seamless transfers enhance both liquidity and investment flexibility.

Challenges and Considerations

Despite the many advantages, clear access banking is not without challenges. Institutions must balance openness with risk management, ensuring that rapid onboarding does not open doors to fraud. Continuous investment in AI‑driven monitoring and human oversight is essential to mitigate these risks.

Another consideration is the digital divide. While many consumers enjoy high-speed internet and smartphones, a segment of the population still lacks reliable connectivity. Banks must therefore maintain alternative channels—such as phone support or community kiosks—to ensure that the promise of clear access does not inadvertently exclude those without digital access.

Future Outlook

The trajectory for clear access banking suggests continued growth, especially as regulatory bodies recognize the benefits of transparency and inclusion. Emerging technologies like decentralized finance (DeFi) and blockchain may further influence how these accounts operate, potentially offering even greater real‑time settlement and reduced intermediation.

Nevertheless, the core tenets—clarity, accessibility, and security—are likely to remain central. As consumer expectations evolve, banks that invest in robust, user‑friendly platforms will be well positioned to capture market share and foster lasting relationships.

In summary, a clear access banking account represents a modern evolution of traditional deposit accounts, built on the pillars of transparency, digital convenience, and regulatory compliance. By leveraging cutting‑edge technology and fostering open‑banking ecosystems, these accounts not only simplify everyday banking but also promote broader financial inclusion. Whether you are a tech‑savvy millennial, a small‑business owner, or someone looking to re‑enter the formal banking system, exploring a clear access offering could be a strategic step toward greater financial control and peace of mind.

As the financial industry continues to innovate, staying informed about such developments is essential. Readers interested in related topics may also find value in exploring the relationship between Merrill Bank of America and its investment arm, detailed in What Is Merrill Bank of America? Unveiling the Full Relationship. Understanding these connections can further enhance your approach to integrated financial management.