Table of Contents

- Understanding e & o insurance for real estate agents

- Why e & o insurance for real estate agents is mandatory in many states

- Core risks that e & o insurance for real estate agents addresses

- How e & o insurance for real estate agents works in practice

- Choosing the right e & o insurance for real estate agents

- Assess your exposure and set appropriate limits

- Compare deductibles and premium structures

- Review policy exclusions carefully

- Consider the insurer’s reputation and claims handling

- Leverage broker expertise

- Cost factors influencing e & o insurance premiums for real estate agents

- Ways to reduce e & o insurance costs without sacrificing protection

- Legal and regulatory considerations for e & o insurance for real estate agents

- Impact of licensing status on coverage

- Special scenarios where e & o insurance for real estate agents becomes critical

- Donations of real estate to charity

- Marketing and lead generation

- Cross‑border transactions

- Steps to file a claim under e & o insurance for real estate agents

- Role of the insurer’s legal team

- Future trends shaping e & o insurance for real estate agents

In the fast‑paced world of residential and commercial property transactions, real estate agents juggle negotiations, client expectations, and regulatory requirements every day. While the excitement of closing a deal can be rewarding, the same process also carries a hidden risk: the possibility of legal claims arising from alleged mistakes, omissions, or negligence.

When a client believes an agent failed to disclose a material fact, misrepresented a property’s condition, or missed a critical deadline, the fallout can quickly move beyond a simple disagreement. Lawsuits, disciplinary actions, and reputational damage are all very real outcomes that can jeopardize an agent’s career and livelihood. This is precisely why e & o insurance for real estate agents has become a cornerstone of professional risk management.

The purpose of this article is to walk you through the fundamentals of errors and omissions (E&O) coverage, explore the specific needs of real estate practitioners, and provide practical guidance on selecting a policy that aligns with both regulatory demands and business goals. By the end of the read, you’ll have a clear roadmap for protecting your practice against the financial and operational consequences of professional errors.

Understanding e & o insurance for real estate agents

E&O insurance, sometimes called professional liability insurance, is designed to shield professionals from claims alleging inadequate or faulty services. For real estate agents, the policy typically covers legal defense costs, settlements, and judgments that arise when a client accuses the agent of errors, omissions, or negligence in the course of their duties.

Key elements of a standard e & o insurance for real estate agents policy include:

- Coverage limits: The maximum amount the insurer will pay for a single claim and for the policy’s aggregate period.

- Deductibles: The amount the insured must pay out‑of‑pocket before the insurer steps in.

- Exclusions: Specific situations or acts not covered, such as intentional wrongdoing or fraudulent behavior.

- Retroactive dates: The date from which prior acts are covered, essential for agents who change carriers.

Because real estate transactions involve large sums of money, complex disclosures, and numerous statutory deadlines, the potential exposure can be substantial. A single lawsuit can quickly exceed the financial capacity of an individual agent, making robust coverage not just advisable but often mandatory under state licensing regulations.

Why e & o insurance for real estate agents is mandatory in many states

Most state real estate commissions require agents and brokers to maintain a minimum level of E&O coverage as a condition of licensure. The rationale is straightforward: the public interest is best served when professionals have a safety net that ensures claimants can receive compensation without bankrupting the practitioner. Moreover, many brokerage firms embed E&O requirements into their contracts, demanding that every affiliated agent hold an active policy.

Failure to maintain the required coverage can lead to penalties ranging from fines to suspension of the real estate license. In addition, without a policy, an agent may be personally liable for any legal costs, which can be devastating even for a modest claim.

Core risks that e & o insurance for real estate agents addresses

Real estate agents encounter a variety of scenarios that can trigger a claim. Below are the most common risk categories covered by an e & o insurance for real estate agents policy:

- Failure to disclose material facts: Omitting known defects, zoning restrictions, or lien information.

- Misrepresentation of property value: Providing inaccurate comparative market analyses or price appraisals.

- Negligent contract preparation: Errors in drafting purchase agreements, lease terms, or escrow instructions.

- Missed deadlines: Overlooking contractual dates such as financing contingencies or inspection periods.

- Improper handling of client funds: Allegations related to escrow or trust account mismanagement.

Each of these scenarios can result in costly litigation, and an E&O policy acts as the financial buffer that allows the agent to focus on defense rather than worrying about personal assets.

How e & o insurance for real estate agents works in practice

When a claim is filed, the insured agent notifies the insurer, who then conducts an initial assessment to determine coverage applicability. If the claim falls within policy terms, the insurer typically assumes responsibility for legal defense, appointing experienced attorneys who specialize in real estate law. Throughout the process, the policyholder may be required to cooperate, provide documentation, and possibly attend settlement discussions.

In many cases, insurers aim to settle early to avoid protracted courtroom battles. However, if the case proceeds to trial, the policy’s limit becomes critical, as it caps the total payout. Agents should therefore choose coverage limits that reflect the scale of their transactions and the potential severity of claims.

Choosing the right e & o insurance for real estate agents

Selecting an appropriate policy involves more than simply picking the cheapest option. Agents need to evaluate several factors to ensure the coverage aligns with their operational realities.

Assess your exposure and set appropriate limits

Begin by estimating the maximum potential loss from a single claim. Consider the average transaction size you handle, the jurisdiction’s legal environment, and the likelihood of multiple claims within a policy period. Many agents opt for limits ranging from $500,000 to $2 million, but high‑volume brokers may require even higher protection.

Compare deductibles and premium structures

A higher deductible can lower the annual premium, but it also means the agent bears more upfront cost when a claim arises. Weigh the trade‑off based on cash flow and risk tolerance. Some carriers offer flexible premium payment plans, which can be advantageous for independent contractors.

Review policy exclusions carefully

Exclusions can vary widely between insurers. Common exclusions include claims arising from fraudulent acts, intentional misrepresentation, or activities performed outside the scope of a licensed real estate professional. Ensure you understand what is not covered, and consider supplemental policies if necessary.

Consider the insurer’s reputation and claims handling

Not all insurers are created equal when it comes to defending claims. Look for carriers with a proven track record of prompt, fair, and transparent claims processing. Reviews from fellow agents, brokerages, and professional associations can provide valuable insight.

Leverage broker expertise

Partnering with a knowledgeable insurance broker who specializes in real estate can simplify the selection process. Brokers can match you with carriers that understand the nuances of e & o insurance for real estate agents, negotiate better terms, and keep you informed about regulatory updates.

For a deeper dive into broker‑specific considerations, see our Real Estate Broker E&O Insurance: A Comprehensive Guide, which outlines how brokerage firms structure coverage for their teams.

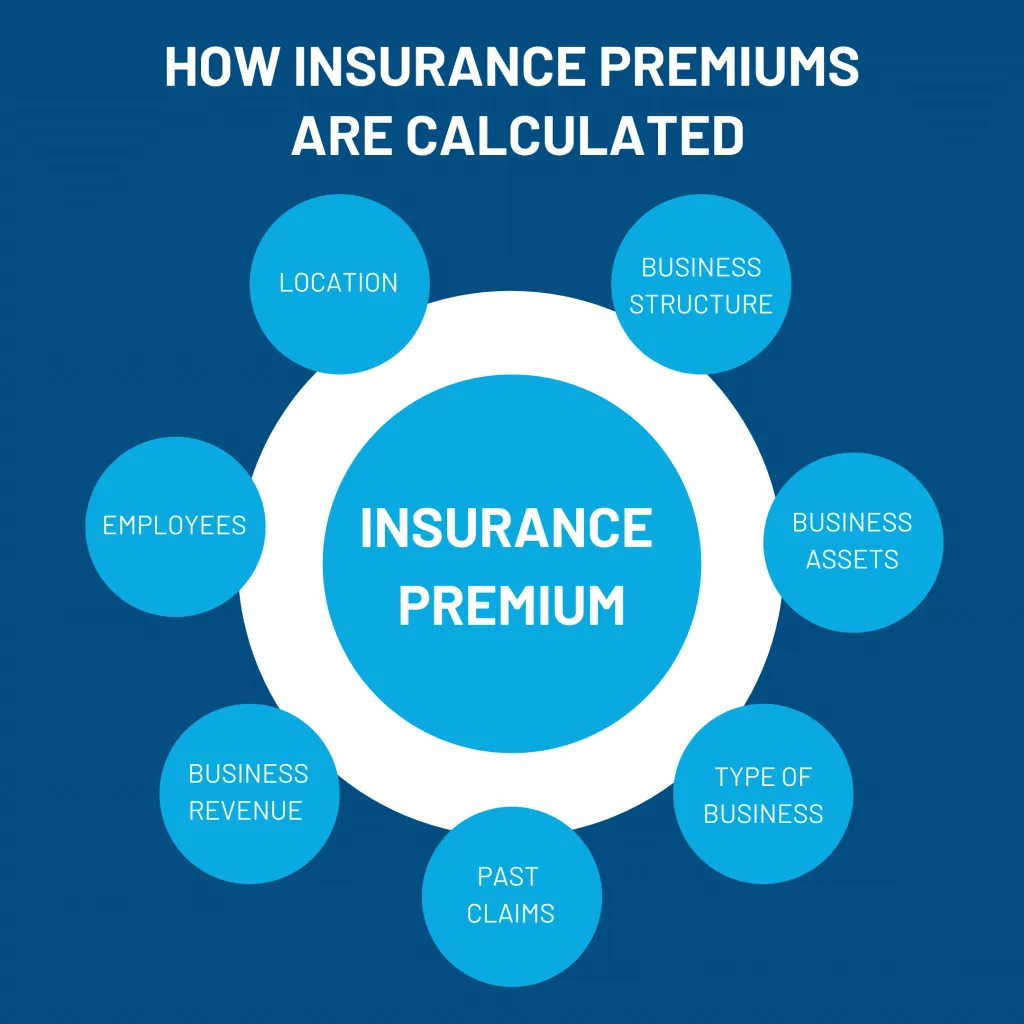

Cost factors influencing e & o insurance premiums for real estate agents

Premiums for e & o insurance for real estate agents are not one‑size‑fits‑all. Insurers assess risk based on a combination of quantitative and qualitative data, including:

- Experience level: Seasoned agents with a clean claims history often enjoy lower rates.

- Transaction volume: Higher sales numbers can increase exposure, leading to higher premiums.

- Geographic location: States with more litigious environments or stricter disclosure laws may see higher costs.

- Claims history: Past lawsuits, even if settled, signal higher risk to insurers.

- Policy features: Higher limits, lower deductibles, and broader coverage extensions raise the premium.

Understanding these drivers helps agents anticipate cost fluctuations and plan budgets accordingly.

Ways to reduce e & o insurance costs without sacrificing protection

Implementing best practices can lead to lower premiums over time:

- Maintain a clean claims record by adhering strictly to disclosure requirements.

- Participate in continuing education courses that focus on risk mitigation and legal updates.

- Adopt technology tools, such as transaction management software, to reduce human error.

- Bundle E&O coverage with other professional policies, like general liability, to qualify for multi‑policy discounts.

Technology, in particular, has reshaped how agents manage risk. For instance, using a robust property management software can streamline document handling and ensure deadlines are never missed.

Legal and regulatory considerations for e & o insurance for real estate agents

Each state’s real estate commission dictates minimum coverage thresholds, but there is also a broader federal backdrop. The Fair Housing Act, for example, imposes strict compliance standards, and violations can trigger E&O claims. Agents must stay current with both state and federal statutes to avoid inadvertent breaches.

Additionally, some brokerage contracts require agents to name the brokerage as an additional insured on the policy. This provision protects the broker’s interests and ensures that any claim against the agent also extends coverage to the firm.

Impact of licensing status on coverage

Agents who hold multiple licenses—such as a dual real estate and mortgage broker license—should verify that their E&O policy covers all activities. Some insurers issue separate endorsements for each license type, while others provide a single, comprehensive policy.

Special scenarios where e & o insurance for real estate agents becomes critical

Beyond day‑to‑day transactions, there are niche situations that heighten the need for robust coverage.

Donations of real estate to charity

When an agent assists a client in donating property to a nonprofit, the transaction involves additional layers of due diligence, valuation, and tax implications. Errors in this process can lead to claims from both the donor and the charity. Our Donation of Real Estate to Charity: A Complete Guide outlines the complexities that agents should be aware of, underscoring why tailored E&O protection is prudent.

Marketing and lead generation

Modern agents rely heavily on digital advertising to generate leads. Misleading ad copy or inaccurate property descriptions can trigger consumer protection claims. A well‑crafted E&O policy often extends to cover advertising errors, but agents should confirm this scope with their insurer.

Cross‑border transactions

Agents dealing with international buyers or sellers encounter differing legal frameworks, currency exchange issues, and additional disclosure obligations. The heightened risk profile warrants higher limits and possibly specialized endorsements.

Steps to file a claim under e & o insurance for real estate agents

When a claim arises, acting promptly can preserve coverage and improve the chances of a favorable outcome. Follow these steps:

- Notify your insurer immediately: Provide a concise summary of the allegation and any supporting documents.

- Preserve evidence: Secure contracts, emails, disclosures, and any communication related to the transaction.

- Cooperate with the adjuster: Respond to requests for information and be transparent about the facts.

- Engage legal counsel: Most insurers will assign attorneys, but you may also retain independent counsel if preferred.

- Stay within policy limits: Avoid settlements that exceed your coverage without insurer approval.

Timely reporting also helps avoid denial of coverage due to policy conditions such as notice requirements or failure to mitigate damages.

Role of the insurer’s legal team

Professional liability insurers typically have a network of experienced real‑estate attorneys who understand industry‑specific nuances. Their expertise can be a decisive advantage, especially when navigating complex jurisdictional issues or negotiating settlements.

Future trends shaping e & o insurance for real estate agents

The insurance landscape is evolving alongside the real estate industry. Emerging trends include:

- Data‑driven underwriting: Insurers are leveraging analytics to better assess an agent’s risk profile based on transaction history and digital footprints.

- Cyber‑E&O hybrid policies: As agents adopt more cloud‑based tools, some carriers bundle cyber liability with traditional E&O coverage.

- Usage‑based pricing: Premiums may adjust dynamically based on real‑time activity metrics, rewarding agents who demonstrate low‑risk behavior.

- Regulatory harmonization: A push toward more uniform national standards could simplify compliance for agents operating across state lines.

Staying informed about these developments helps agents anticipate changes in policy terms and pricing, ensuring continuous protection.

In summary, e & o insurance for real estate agents is not merely a regulatory checkbox—it is an essential safeguard that enables agents to operate confidently in a high‑stakes environment. By understanding the scope of coverage, assessing risk, and selecting a policy that aligns with their business model, agents can mitigate financial exposure, uphold professional reputation, and focus on delivering value to clients.

Whether you are a solo practitioner, part of a boutique brokerage, or managing a large team, investing in the right E&O policy is a strategic decision that pays dividends in peace of mind and operational resilience.